Financial and Compliance Audit of the O‘ahu Metropolitan Planning Organization

Posted on Apr 15, 2024 in Summary

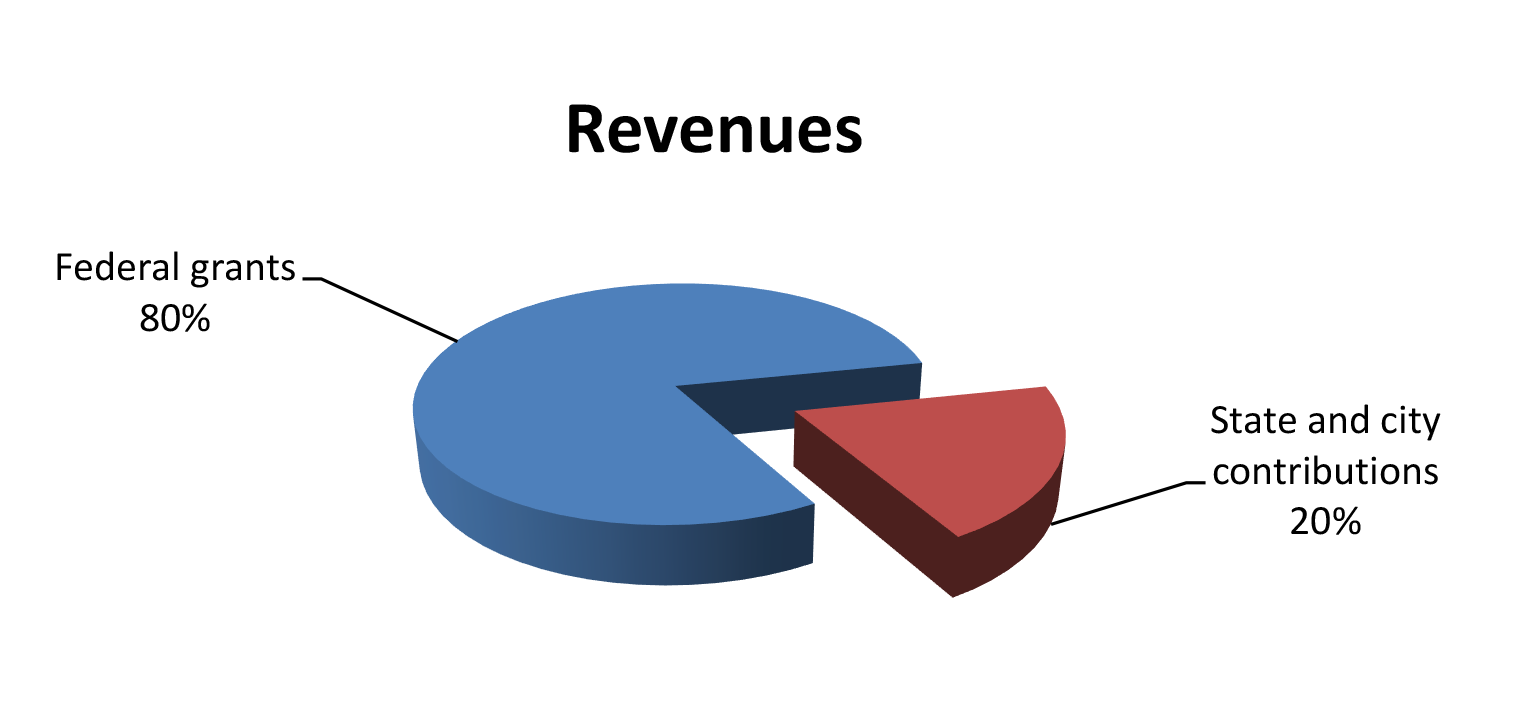

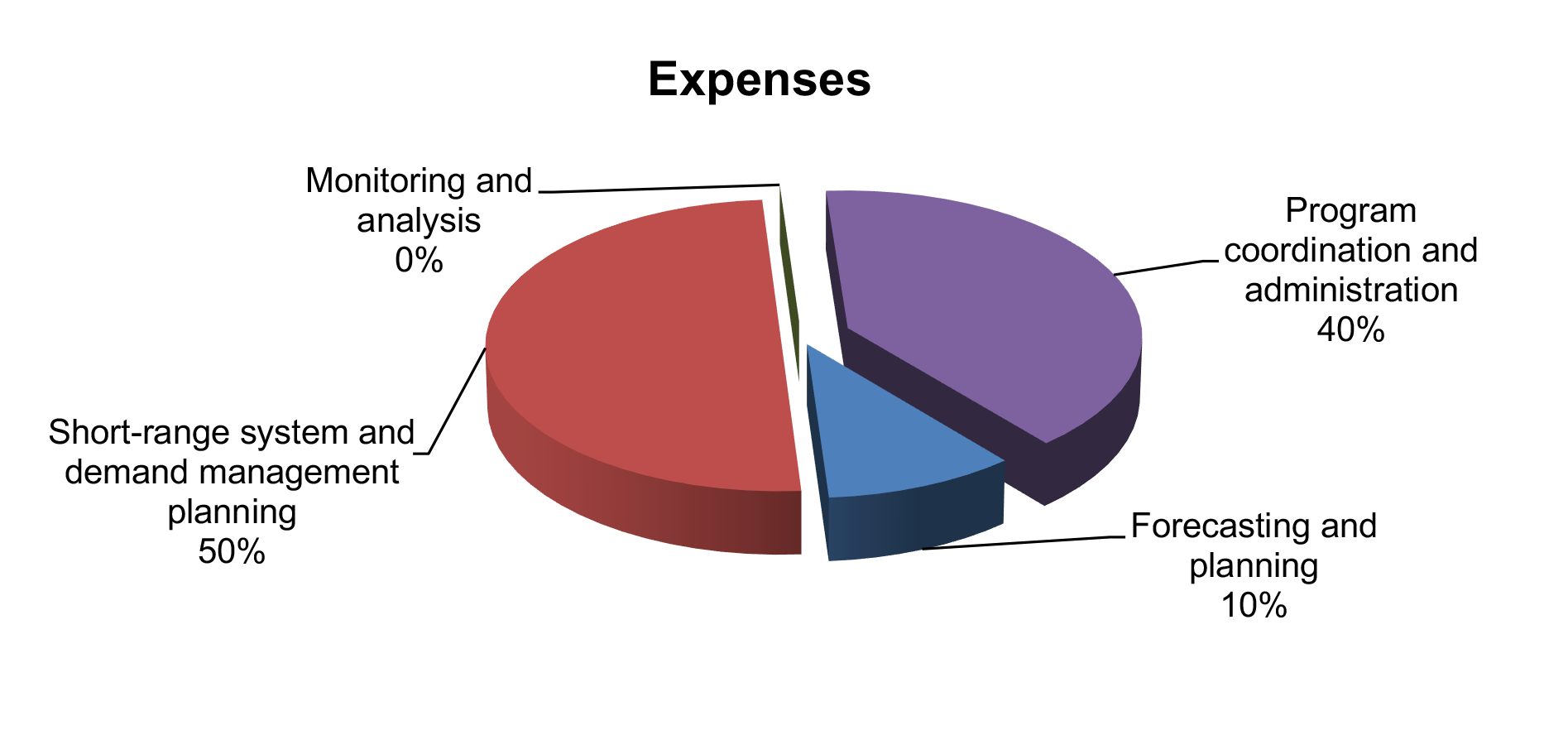

PHOTO: O‘AHU METROPOLITAN PLANNING ORGANIZATION AUDITOR’S SUMMARY Financial Statements, Fiscal Year Ended June 30, 2023 THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the O‘ahu Metropolitan Planning Organization, as of and for the fiscal year ended June 30, 2023, and to comply with the requirements of Title 2, U.S. Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by N&K CPAs, Inc. Financial Highlights FOR THE FISCAL YEAR ended June 30, 2023, OahuMPO reported total revenues of approximately $3.74 million and total expenses of approximately $3.73 million, resulting in minimal change in net position. Revenues consisted of $3 million from federal grants and $744,000 in contributions from the State of Hawai‘i and City and County of Honolulu. Total expenses consisted of (1) $358,000 for transportation forecasting and long-range planning; (2) $1.87 million for short-range transportation system and demand management planning; (3) $6,000 for transportation monitoring and analysis; and (4) $1.49 million for program coordination and administration. As of June 30, 2023, total assets exceeded total liabilities by $498,000. Total assets of $1.8 million, included cash of $822,000, receivables and other assets of $895,000, and net capital assets of $87,000. Total liabilities were $1.3 million.

Auditors’ Opinion OahuMPO RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles. OahuMPO also received an unmodified opinion on its compliance with major federal programs in accordance with the Uniform Guidance. Findings THERE WERE NO REPORTED DEFICIENCIES in internal control over financial reporting that were considered to be material weaknesses and no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. However, the auditors identified two significant deficiencies that are required to be reported under Government Auditing Standards. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. The significant deficiencies are described on pages 45-46 of the report. There were no findings that were considered material weaknesses in internal control over compliance in accordance with the Uniform Guidance. |

| About the Organization

Federal highway and transit statutes require urbanized areas greater than 50,000 in population to designate a metropolitan planning organization as a condition for spending federal highway or transit funds. O‘ahu Metropolitan Planning Organization (OahuMPO) is the designated metropolitan planning organization for the island of O‘ahu. OahuMPO was established by agreement between the Governor of the State of Hawai‘i and the Chairperson of the City Council of the City and County of Honolulu and serves as the decision-making body responsible for carrying out continuing, comprehensive, and cooperative transportation planning and programming for the island of O‘ahu. |