Financial Audit of the Employees’ Retirement System of the State of Hawai’i

Posted on Mar 15, 2024 in Summary

Photo: iStock.com AUDITOR’S SUMMARY

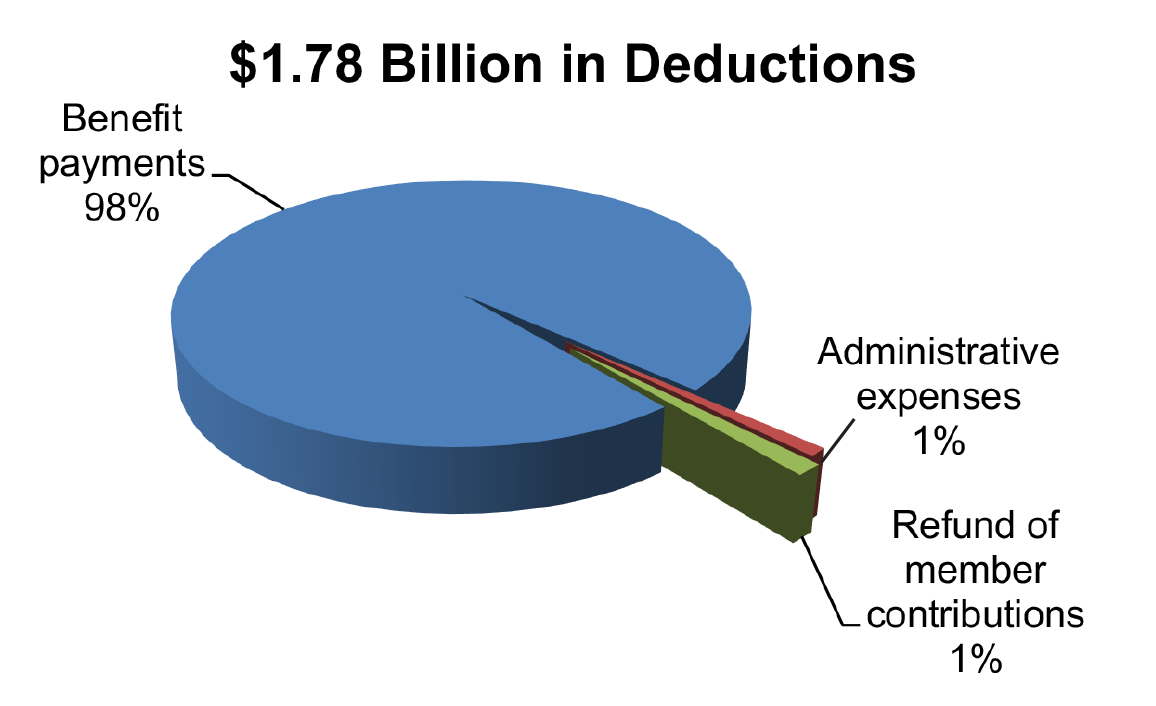

Financial Statements, Fiscal Year Ended June 30, 2022 THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the Employees’ Retirement System of the State of Hawai‘i, as of and for the fiscal year ended June 30, 2022. The audit was conducted by Eide Bailly LLP. Financial Highlights FOR THE FISCAL YEAR ended June 30, 2022, ERS reported total net additions of approximately $1.7 billion. Additions consisted of $1.53 billion from contributions and $165 million in net investment income.

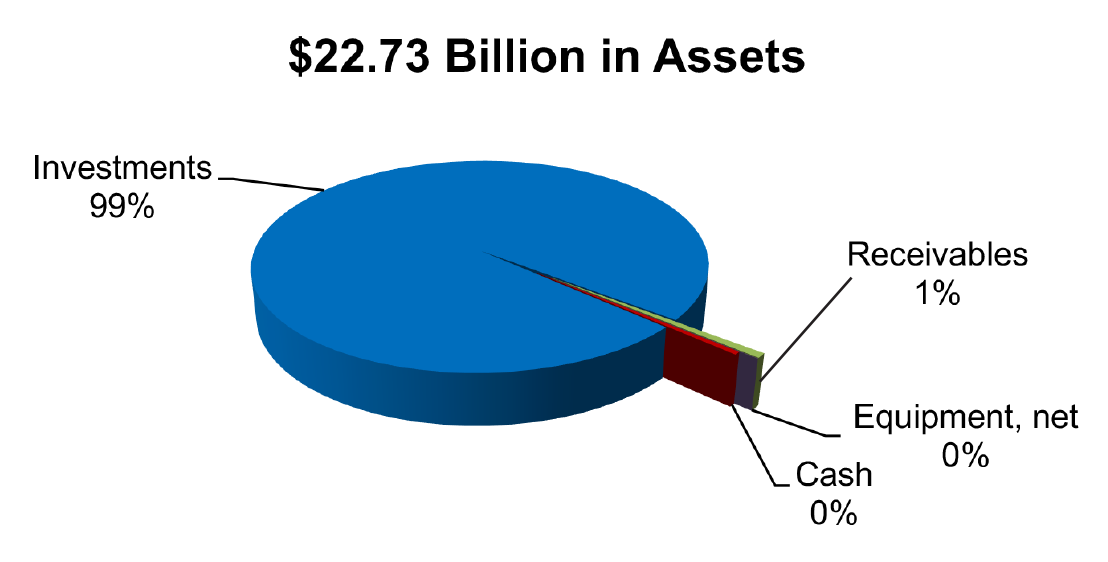

As of June 30, 2022, assets totaled $22.73 billion and liabilities totaled $872 million, leaving a net position balance of $21.86 billion. Total assets included (1) investments of $22.47 billion; (2) receivables of $156 million; (3) cash of $99 million; and (4) net equipment of $5 million. Auditors’ Opinion Findings A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected, on a timely basis. The material weakness identified by the auditors related to the classification of certain investments. A reclassifying journal entry was recorded by management to correct the classification and accounting for these investments. There was no impact on net position, but the journal entry had material impacts on financial statement line items in the statement of fiduciary net position. Management acknowledged the finding and has implemented procedures to monitor, review and approve investment classifications for reporting in conformity with similar investments held by other statewide employee retirement systems. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. The significant deficiency identified by the auditors related to the lack of a documented journal entry review and approval process. Management acknowledged the finding and has implemented procedures to strengthen the journal entry, review, and approval process. There were no instances of noncompliance or other matters required to be reported under Government Auditing Standards. The Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards is reported separately and is available upon request. |

| About the System

The Employees’ Retirement System of the State of Hawai‘i (ERS) is a cost-sharing, multiple-employer retirement system for government workers. Through its pension benefits program, ERS provides a defined-benefit pension plan for all state and county employees, including teachers, professors, police officers, firefighters, correction officers, judges and elected officials. ERS is governed by a Board of Trustees, which consists of eight members. |