21-04, Proposed Special and Revolving Fund Analyses

Posted on Mar 3, 2021 in Summary

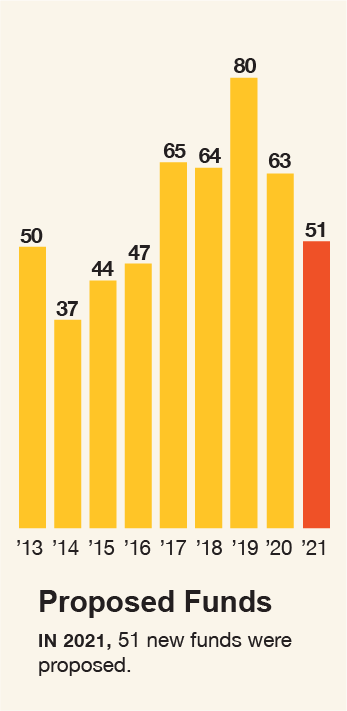

AUDITOR’S SUMMARY Fifty-one funds proposed in 2021 did not meet criteria We reviewed 75 House and Senate bills proposing 51 special and revolving funds during the 2021 legislative session of which none met criteria. ONLY ABOUT HALF OF THE MONEY the State spends each year comes from its main financial account, the general fund. The other half of expenditures are financed by special, revolving, federal, and trust funds. Between 2008 and 2012, the number of these non-general funds and the amount of money contained in them substantially increased. Much of that upward trend had been caused by an increase in special funds, which are funds set aside by law for a specified object or purpose. In 2013, the Legislature amended Section 23-11, Hawai‘i Revised Statutes (HRS), after the Auditor recommended changes to stem a trend in the proliferation of special and revolving funds over the past 30 years. Such funds erode the Legislature’s ability to control the State budget through the general fund appropriation process. General funds, which made up about two-thirds of State operating budget outlays in the late 1980s, had dwindled to about half of outlays. By 2011, special funds amounted to $2.48 billion, or 24.3 percent, of the State’s $10.2 billion operating budget. Also ballooning were revolving funds, which are used to pay for goods and services and are replenished through charges to users of the goods and services or transfers from other accounts or funds. By 2011, revolving funds made up $384.2 million, or 3.8 percent, of the State’s operating budget. Further hampering the Legislature’s control over the budget process was a 2008 court case. In Hawai‘i Insurers Council v. Linda Lingle, Governor of the State of Hawai‘i, the Hawai‘i Supreme Court determined that under only certain conditions could the Legislature “raid” special funds to balance the State budget. In 2013, in order to gain more control over the budget process, the Legislature built new safeguards into the criteria for establishing special funds. We reviewed 75 House and Senate bills proposing 51 special and revolving funds during the 2021 legislative session. None satisfied the criteria set forth in Section 23-11, HRS, for proposed special and revolving funds. References to House Draft and Senate Draft versions reflect bill status at the time of our review.

|

| The Criteria

SECTION 23-11, HRS, 1. The need for the fund, as demonstrated by:

2. Whether there is a clear nexus between the benefits sought and charges made upon the program users or beneficiaries or a clear link between the program and the sources of revenue, as opposed to serving primarily as a means to provide the program or users with an automatic means of support that is removed from the normal budget and appropriation process. |