21-07, Review of General Excise and Use Tax Exemptions and Exclusions Pursuant to Section 23-73, Hawai‘i Revised Statutes

Posted on Apr 1, 2021 in Summary

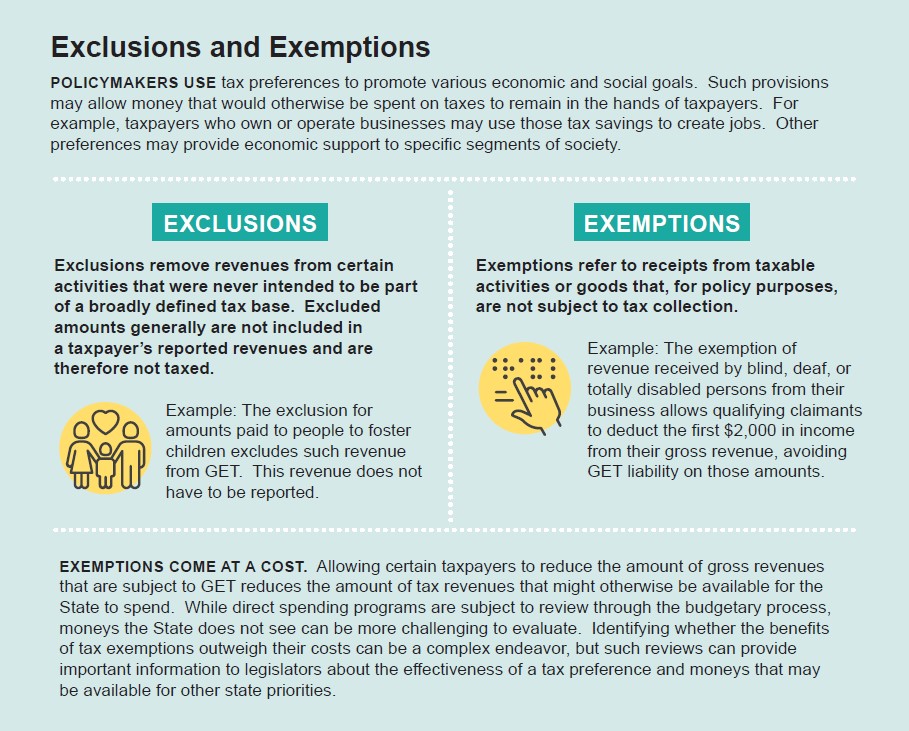

Illustration: istock.com AUDITOR’S SUMMARY This report assesses certain tax exemptions and exclusions from Hawai‘i’s General Excise Tax (GET). Section 23-71 et seq., Hawai‘i Revised Statutes (HRS), requires the Auditor to annually review different tax exemptions, exclusions, and credits on a 10-year recurring cycle. As described by the Department of Taxation (DoTax), Hawai‘i’s GET and Use Tax, combined, apply to nearly all business activities in the state. In fiscal year 2020, which ended June 30, 2020, GET and Use Tax revenues accounted for $3.36 billion, or 49 percent of the total tax revenue of $6.89 billion. Those amounts predate the current COVID-19 pandemic, which has significantly impacted public health and the State’s economy, while simultaneously resulting in sharp reductions in GET and Use Tax revenue. This report reviews a total of nine tax provisions – seven GET exemptions and two GET exclusions. While DoTax collects data on seven of these tax provisions, our ability to report information about three of them was restricted by DoTax’s policy prohibiting disclosure of information, even in aggregated form, when there are a limited number of taxpayers. The current policy is to exclude disclosure when there are five or fewer claims for an exemption, or when an individual return represents a large percentage of the tabulation. We note we were required to analyze an exemption for amounts received by TRICARE-managed care support contractors. However, that exemption was repealed on December 31, 2018. We, therefore, did not review that exemption. We also note that the GET exemption relating to cooperative housing corporations is related to an exemption for reimbursements to associations of owners of condominium property regimes or nonprofit homeowners or community associations, which we are not scheduled to analyze until 2024. However, because DoTax does not segregate data relating to these two exemptions, we report the exemptions’ aggregated numbers in this report. Overall, we found there was insufficient data to determine whether six of the seven exemptions reviewed are meeting their stated or inferred purposes. As we note in the report, making conclusions as to whether purposes have been met is extremely difficult where amounts claimed are not tracked or where no benchmarks or metrics are provided. We also found that one exemption for amounts received by a patient-centered community care contractor used to pay third-party health care providers pursuant to a contract with the United States is likely being erroneously or improperly claimed by some taxpayers. |

In fiscal year 2020, which ended June 30, 2020,GET and Use Tax revenues accountedfor $3.36 billion, or 49 percent of thetotal tax revenue of $6.89 billion. |

|