Do you need help in another language? We will get you a free interpreter. Call 808-587-0800 to tell us which language you speak.

您需要其它語言嗎?如有需要, 請致電 808-587-0800, 我們會提供免費翻譯服務

En mi niit alilis lon pwal eu kapas? Sipwe angei emon chon chiaku ngonuk ese kamo. Kokori 808-587-0800 omw kopwe ureni kich meni kapas ka ani.

Avez-vous besoin d'aide dans une autre langue? Nous pouvons vous fournir gratuitement des services d'un interprète. Appelez le 808-587-0800 pour nous indiquer quelle langue vous parlez.

Brauchen Sie Hilfe in einer andereren Sprache? Wir koennen Ihnen gern einen kostenlosen Dolmetscher besorgen. Bitte rufen Sie uns an unter 808-587-0800 und sagen Sie uns Bescheid, welche Sprache Sie sprechen.

Makemake `oe i kokua i pili kekahi `olelo o na `aina `e? Makemake la maua i ki`i `oe mea unuhi manuahi. E kelepona 808-587-0800 `oe ia la kaua a e ha`ina `oe ia la maua mea `olelo o na `aina `e.

Masapulyo kadi ti tulong iti sabali a pagsasao? Ikkandakayo iti libre nga paraipatarus. Awaganyo ti 808-587-0800 tapno ibagayo kadakami no ania ti pagsasao nga ar-aramatenyo.

다른언어로 도움이 필요하십니까? 저희가 무료로 통역을 제공합니다. 808-587-0800 로 전화해서 사용하는 언어를 알려주십시요

您需要其它语言吗?如有需要,请致电 808-587-0800, 我们会提供免费翻译服务

Kwoj aikuij ke jiban kin juon bar kajin? Kim naj lewaj juon am dri ukok eo ejjelok wonen. Kirtok 808-587-0800 im kwalok non kim kajin ta eo kwo melele im kenono kake.

E te mana'o mia se fesosoani i se isi gagana? Matou te fesosoani e ave atu fua se faaliliu upu mo oe. Vili mai i le numera lea 808-587-0800 pea e mana'o mia se fesosoani mo se faaliliu upu.

¿Necesita ayuda en otro idioma? Nosotros le ayudaremos a conseguir un intérprete gratuito. Llame al 808-587-0800 y diganos que idioma habla.

Kailangan ba ninyo ng tulong sa ibang lengguwahe? Ikukuha namin kayo ng libreng tagasalin. Tumawag sa 808-587-0800 para sabihin kung anong lengguwahe ang nais ninyong gamitin.

'Oku ke fiema'u tokoni 'iha lea makehe? Te mau malava 'o 'oatu ha fakatonulea ta'etotongi. Telefoni ki he 808-587-0800 'o fakaha mai pe koe ha 'ae lea fakafonua 'oku ke ngaue'aki.

Bạn có cần giúp đỡ bằng ngôn ngữ khác không ? Chúng tôi se yêu cầu một người thông dịch viên miễn phí cho bạn. Gọi 808-587-0800 nói cho chúng tôi biết bạn dùng ngôn ngữ nào?

Gakinahanglan ka ba ug tabang sa imong pinulongan? Amo kang mahatagan ug libre nga maghuhubad. Tawag sa 808-587-0800 aron magpahibalo kung unsa ang imong sinulti-han

Report summaries not listed here can be found within their full report. Search our full report list here.

Date

Content

Title

Tags

Category

05/09/2025

Photo: iStock.com

AUDITOR’S SUMMARY

Section 342G-107, Hawaii Revised Statutes (HRS), requires the Auditor to conduct a management and financial audit of the Department of Health’s (DOH) Deposit Beverage Container Program (Program) in even-numbered fiscal years, after the initial audit for the fiscal year ended June 30, 2005. We contracted KMH LLP, a certified public accounting firm, to conduct this financial and program audit for the fiscal year ended June 30, 2024. This is the Auditor’s tenth review of the Program

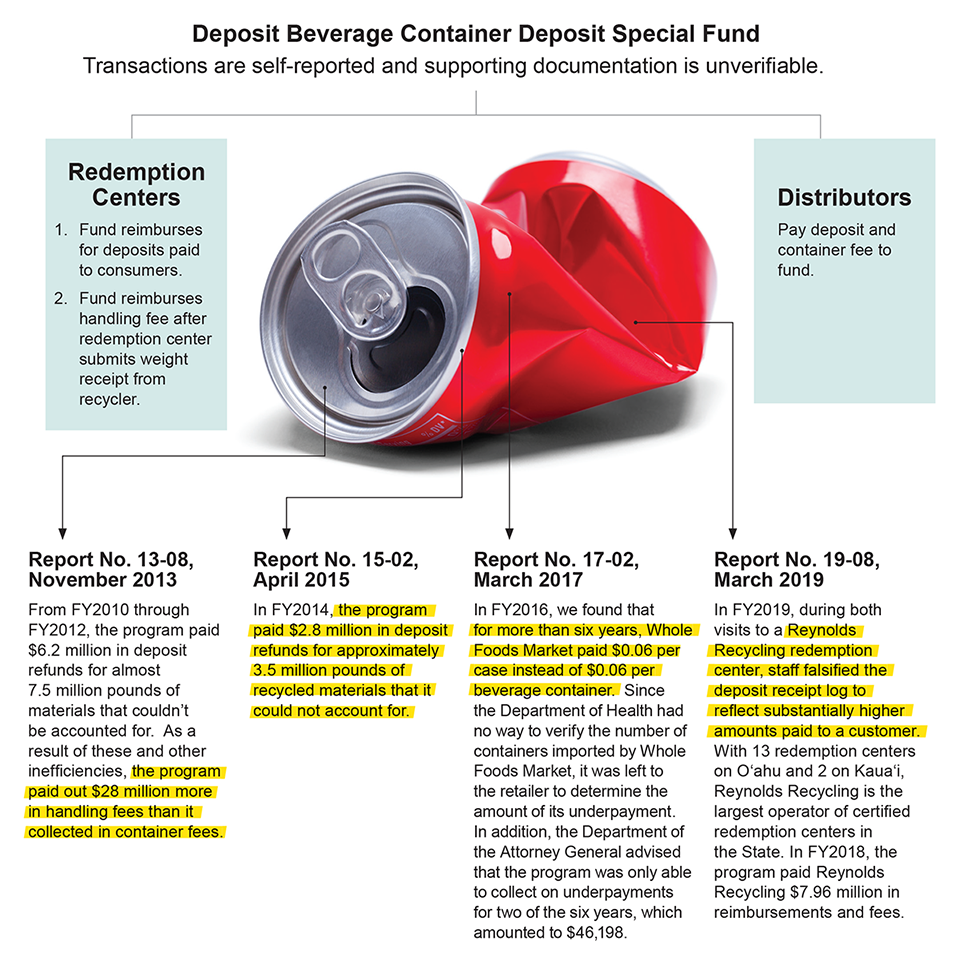

THE LEGISLATURE ESTABLISHED the Deposit Beverage Container Program (Program) in 2002 to increase recycling of specific types of beverage containers, reduce litter, and provide a connection between beverage container manufacturing decisions and Program management. The Deposit Beverage Container Deposit Special Fund (Special Fund) was created to hold fees, deposits, and accrued interest – moneys that are used to pay deposit beverage container refunds and handling fees and Program-related expenses.

Review of Prior Findings

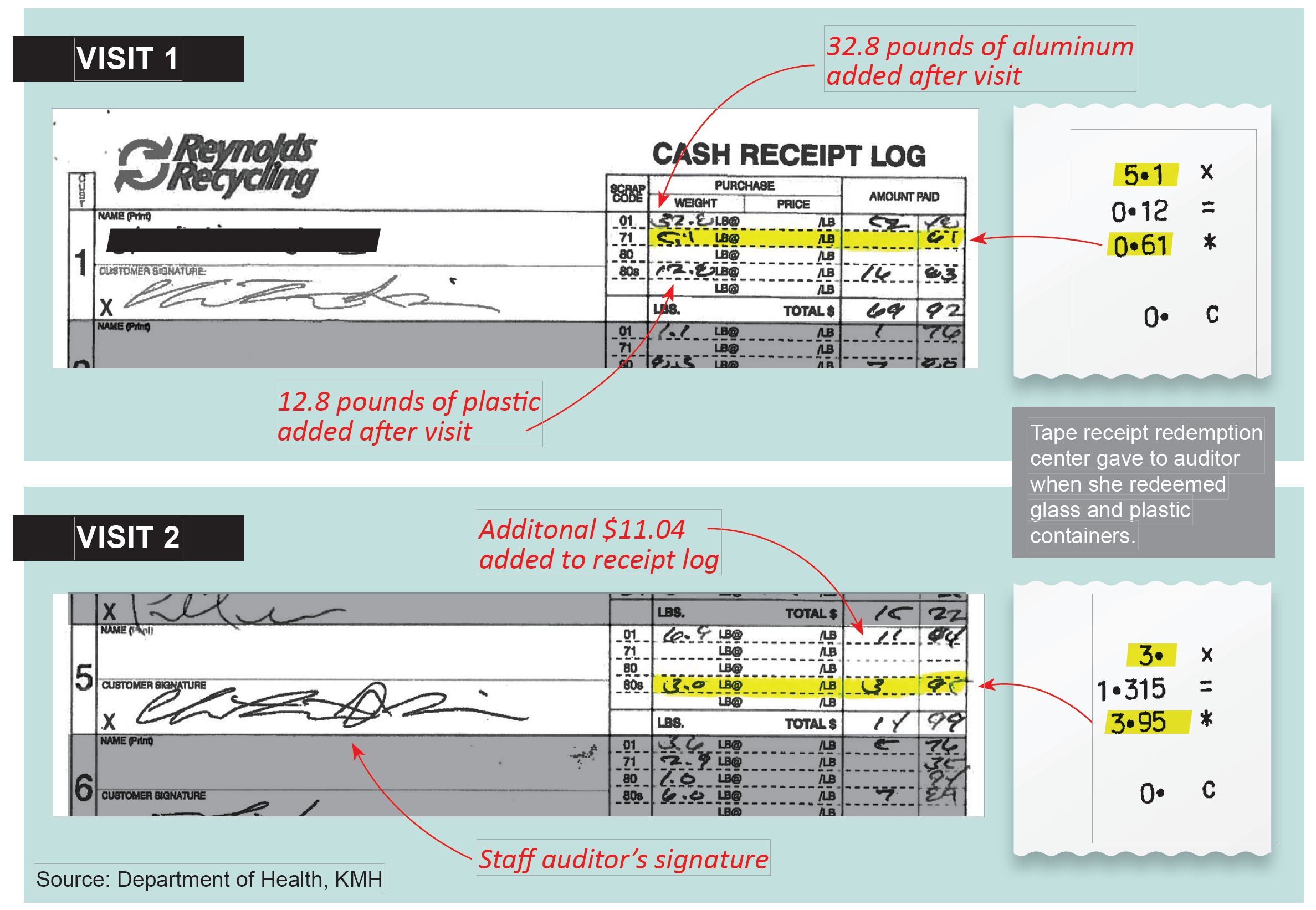

Our initial review, issued in 2005, found DOH’s reliance on self-reported numbers from distributors and certified redemption centers exposed the Program to possible fraud and abuse. Six subsequent audits issued between 2008 and 2018 found those initial findings remained relevant; the department had taken no meaningful action to address the chronic issues. Specifically, we have pointed out that distributors and redemption centers have financial incentive to under- or over-report the amounts that the distributors must pay into the Special Fund and amounts that the redemption centers may claim for reimbursement from the Special Fund. For example, in 2015 we reported that a distributor, Whole Foods Market, Inc., had substantially underpaid the department for years by depositing $0.06 per case of beverages rather than $0.06 for each individual container. In 2018, auditors identified two instances of actual fraud at a redemption center by comparing receipts received for redeeming containers against the cash receipt log submitted to DOH to support the center’s claim for reimbursement; the amounts the redemption center claimed – and DOH reimbursed – were significantly higher than the auditors had received for redeeming containers. DOH took no action against the redemption center and reimbursed the inflated amounts.

In 2021, instead of repeating the same, unaddressed findings, we adopted a new approach to examine why DOH had not taken meaningful action to address chronic issues by implementing controls or making other changes. We found the Program viewed our biennial audits as a replacement for internal controls and expected the Auditor to review records and identify errors in the amounts received from distributors or claimed by redemption centers. The following year, the Legislature passed Act 12, Session Laws of Hawai‘i 2022, codified as Section 342G-121.5, HRS, to compel DOH to develop and implement procedures to verify the accuracy and completeness of the data reported by beverage distributors and redemption centers, as we repeatedly recommended.

Given the relatively short period between the passage of Act 12 and our 2023 review, as well as DOH’s representation that it was in the process of implementing changes, we switched our approach again in 2023. We asked DOH to submit the required financial information and provide an update on steps the Program had taken to address the 2021 audit findings. This report again assessed the implementation of those recommendations, as well as DOH’s compliance with Section 342G-121.5, HRS.

What We Found in 2024

In 2024, we examined relevant documents and records, interviewed Program personnel, and evaluated whether DOH’s actions addressed our 2021 recommendations. We found DOH still has made no progress on implementing prior recommendations, including those codified by the Legislature in Section 342G-121.5, HRS. Specifically, we found DOH has not implemented any of our eight recommendations, including one the department did not agree with and did not intend to implement. Since the requirement to implement those recommendations was codified in HRS, DOH is not in compliance with its legal mandate.

Financial Highlights

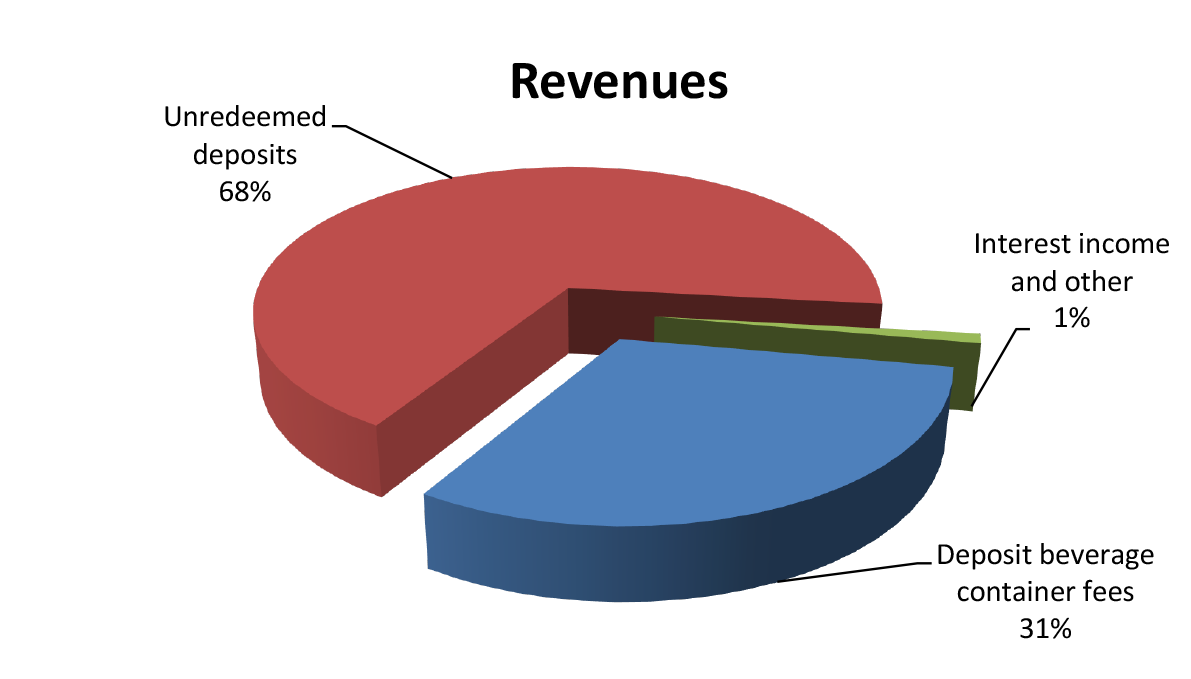

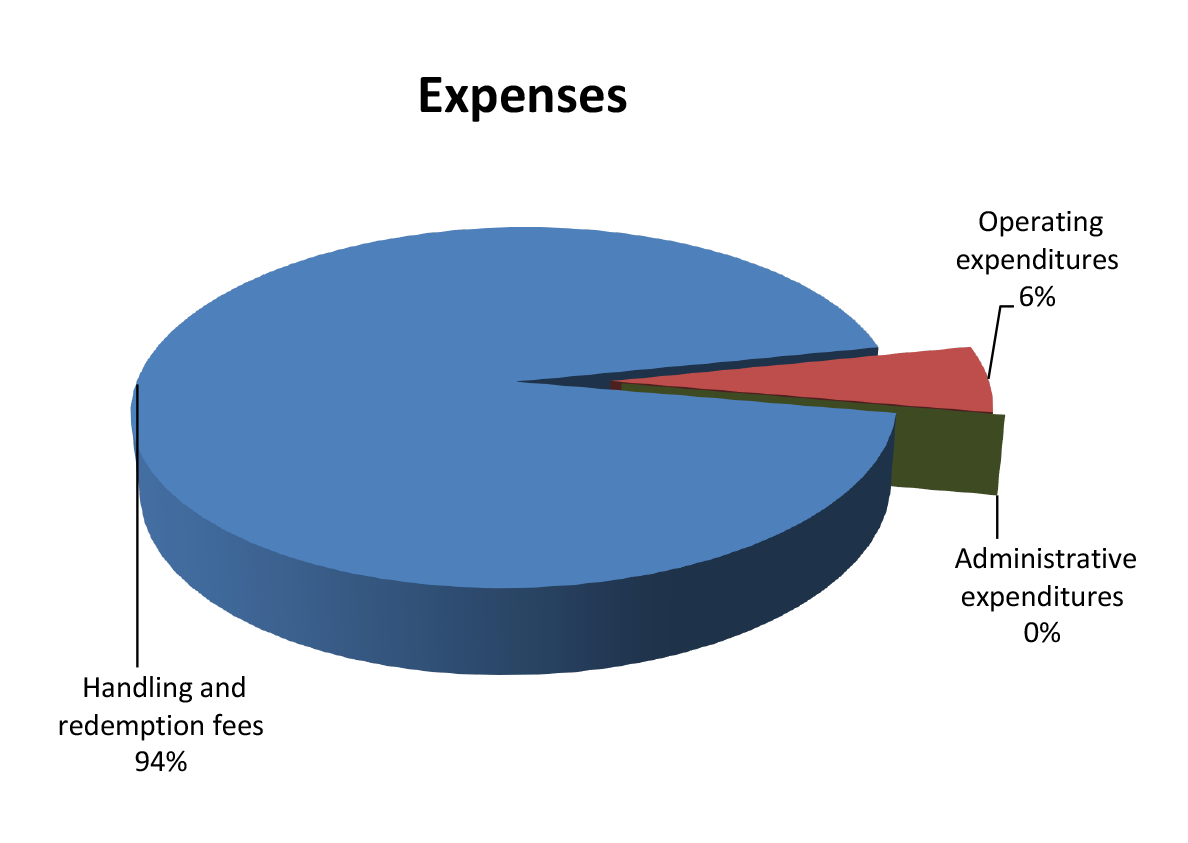

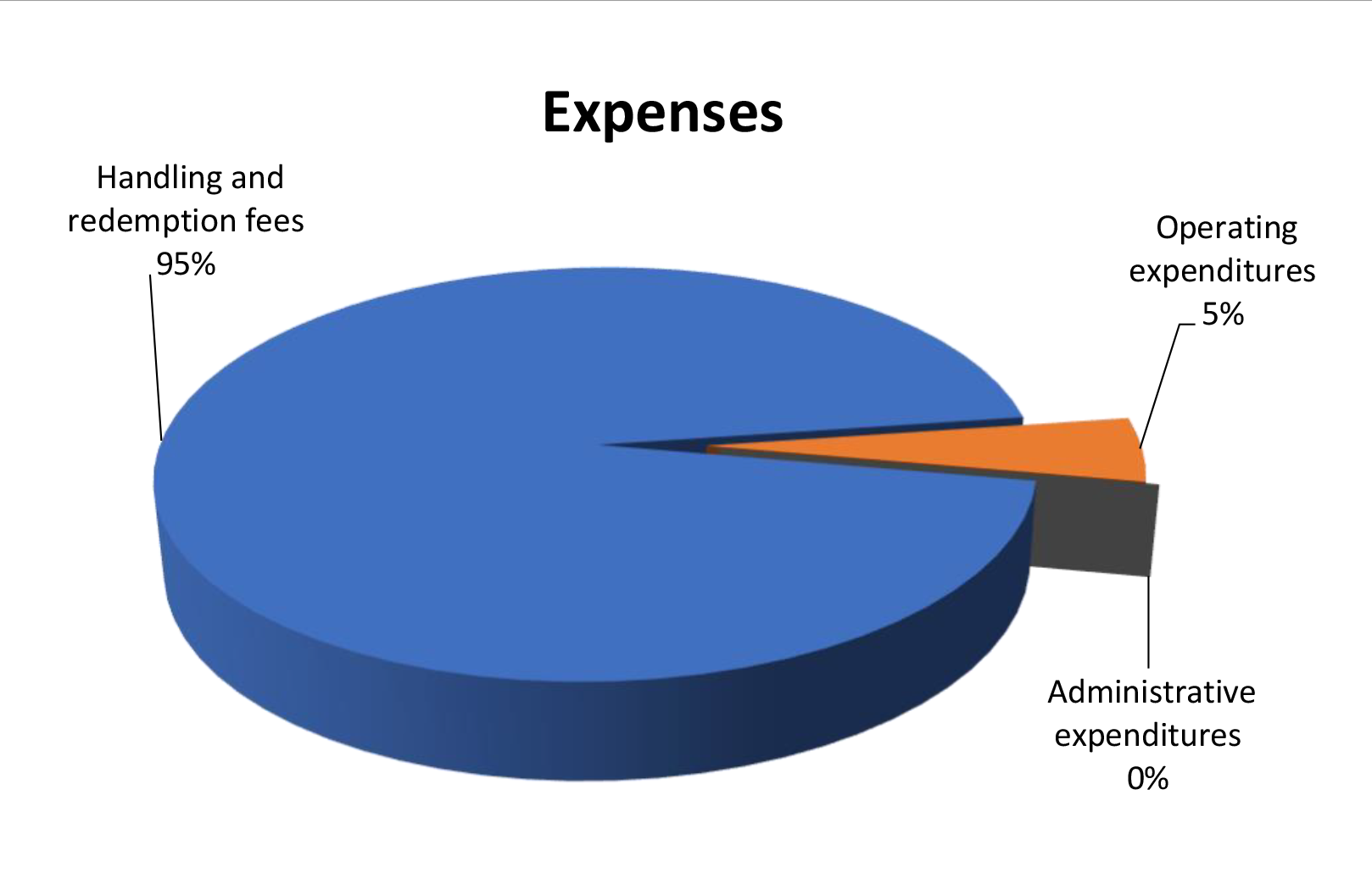

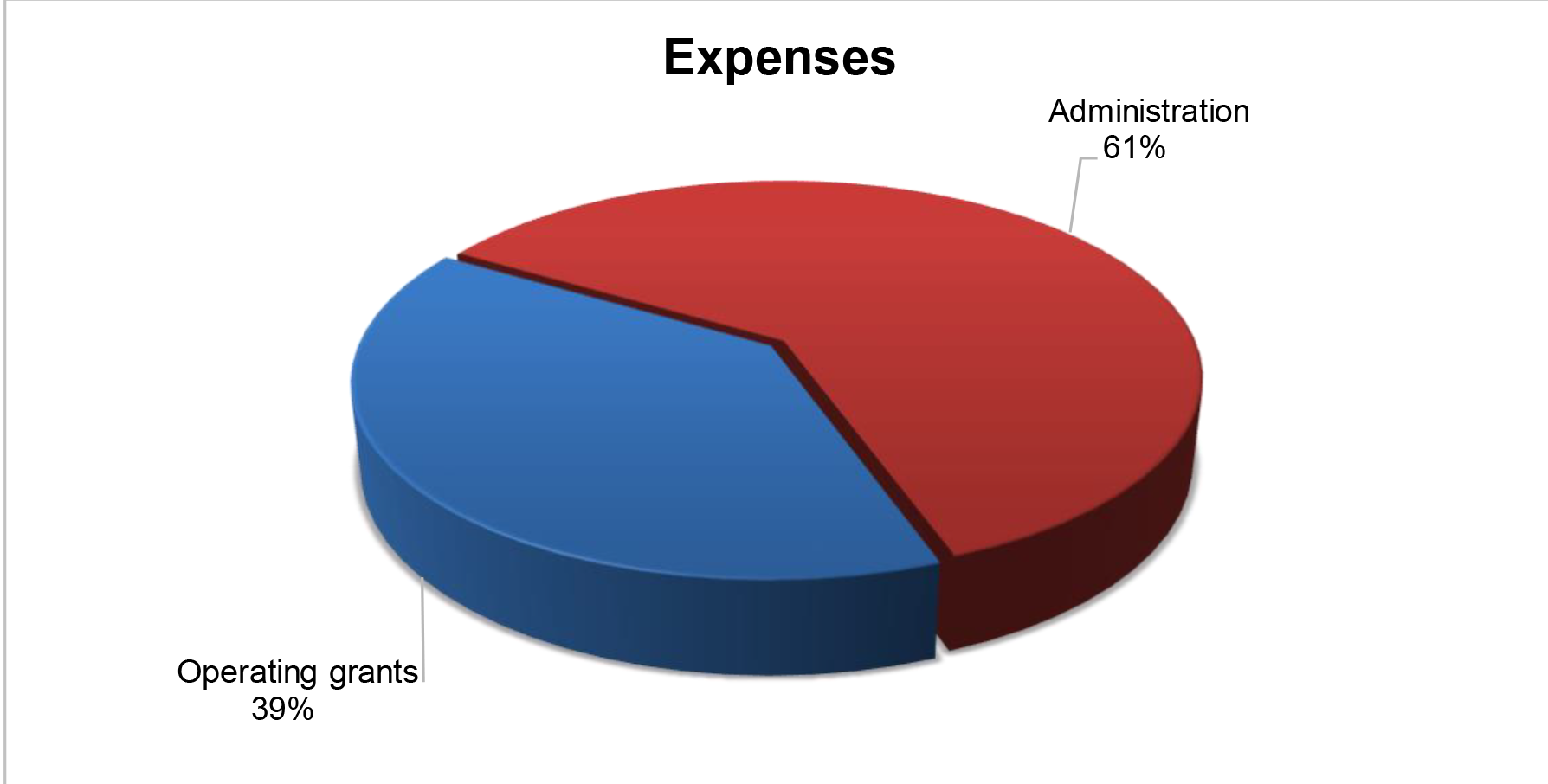

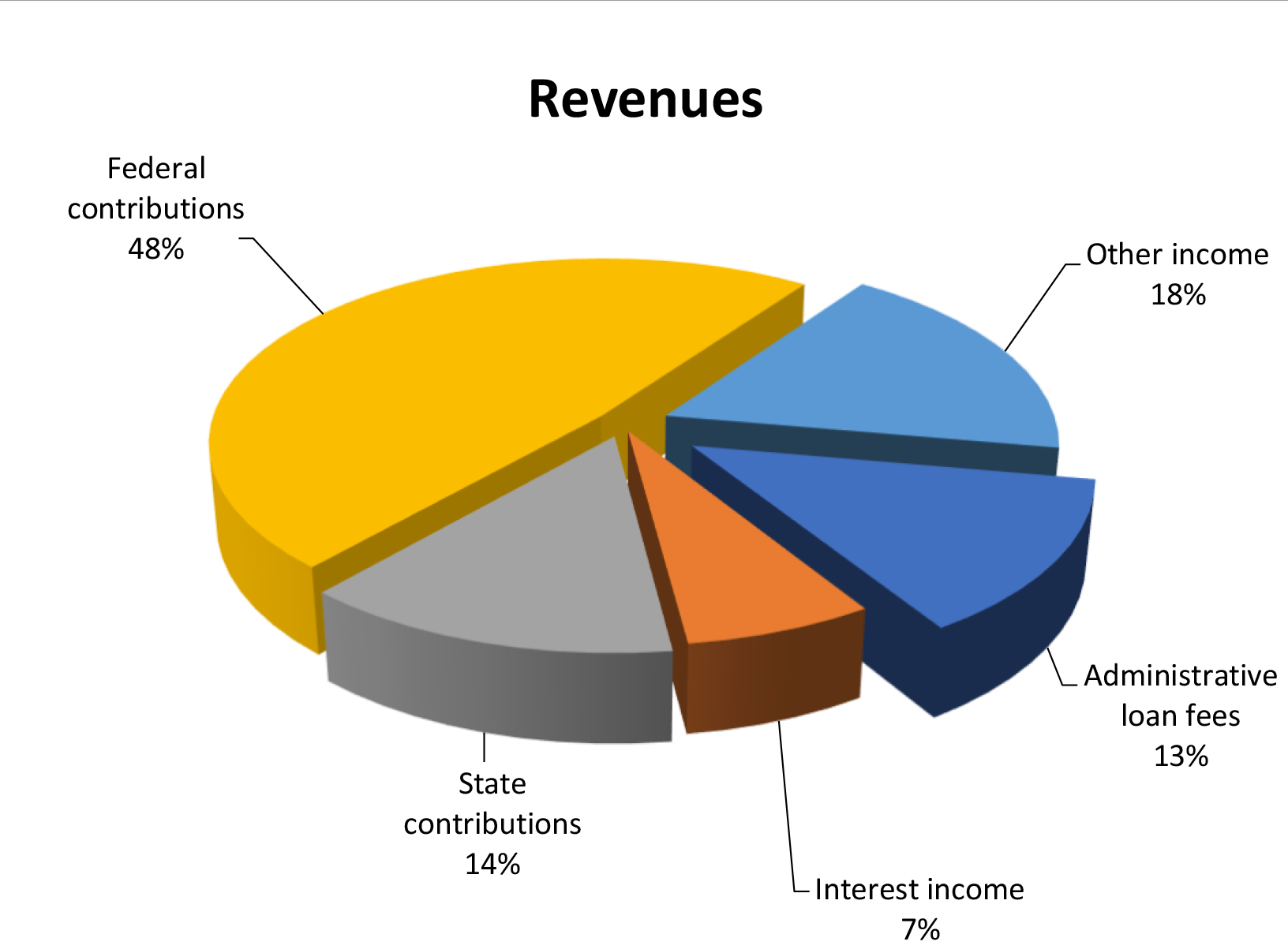

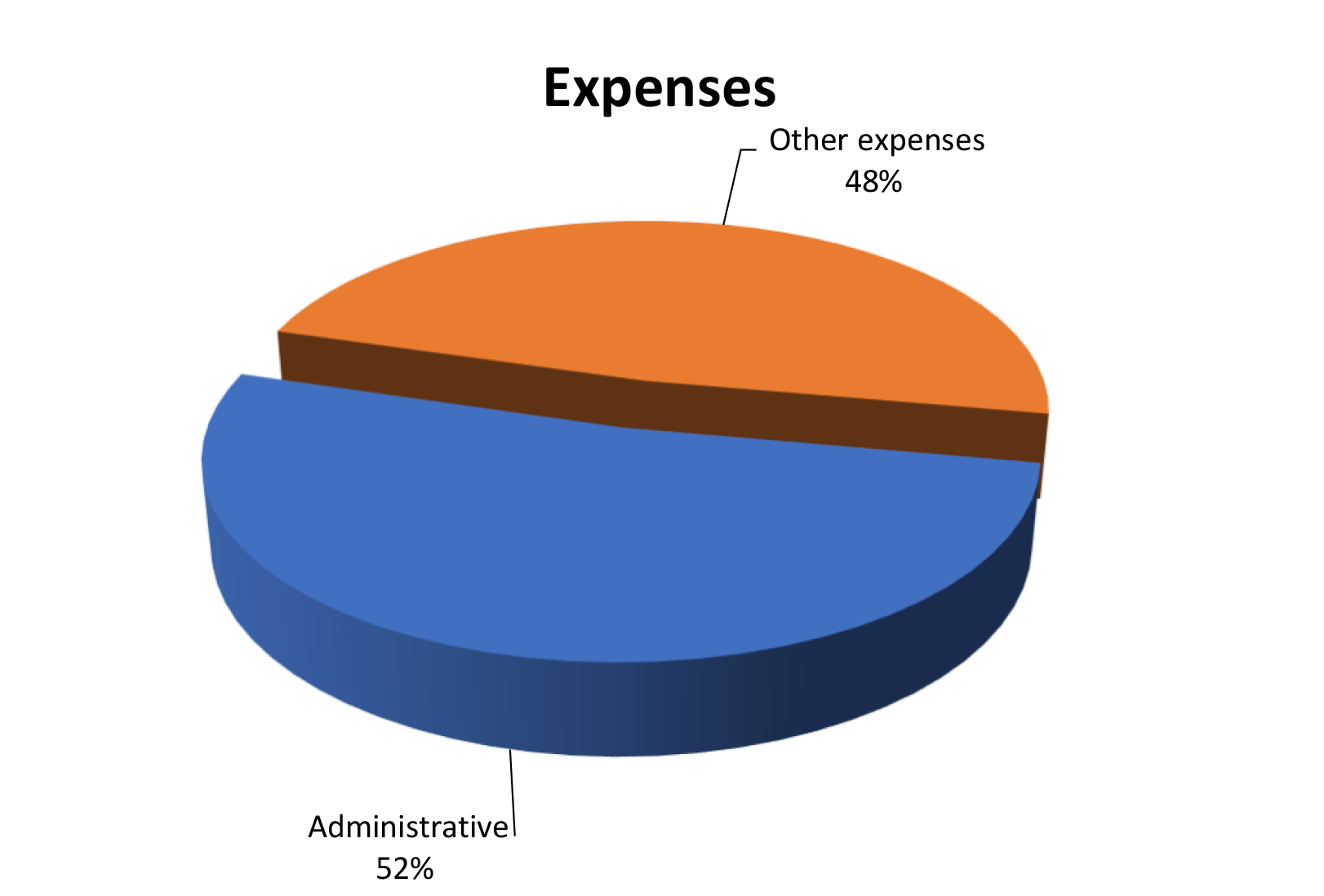

FOR THE FISCAL YEAR ended June 30, 2024, the special fund reported total revenues of $33.57 million and total expenditures of $23.03 million, resulting in a change of fund balance of $10.54 million. Total revenues consisted of (1) deposit beverage container fees of $10.37 million, (2) unredeemed deposits of $20.81 million, and (3) investment income of $2.38 million, and (4) nonimposed employee fringe benefits of $7,390. Total expenditures consisted of (1) handling and redemption fees of $21.01 million, (2) operating expenditures of $2 million, and (3) administrative expenditures of $28,587.

As of June 30, 2024, total assets were $85.79 million and total liabilities were $7.93 million. Total assets were comprised of (1) cash and cash equivalents of $76.33 million, (2) accounts receivable of $9.24 million, and (3) interest receivable of $226,842. Total liabilities were comprised of (1) vouchers and contracts payable of $4.37 million; (2) accrued wages and employee benefits of $124,548; and (3) beverage container deposits of $3.43 million.

Auditors’ Opinion The special fund received an unmodified opinion that its financial statements presented fairly, in all material respects, the financial position of the fund as of June 30, 2024, in accordance with generally accepted accounting principles.

Findings

One material weakness was reported – some vouchers payable were not recorded, resulting in an overstated fund balance. Management accepted a proposed adjustment of approximately $733,000 to increase vouchers payable and expenditures.

One significant deficiency was also reported, relating to over-reliance on third party certifications. As we found in prior audits, the Program continued to rely on self-reporting from beverage distributors and redemption centers. This overreliance may result in underpayments on deposits and related container payments DOH receives to administer the Program, overpayments of deposit refunds and handling fees to redemption centers, and an overstated redemption rate. An overstated redemption rate could result in a misstatement in DOH’s financial statements, as well as higher fees for consumers.

IN 2020, as it entered its third decade, the Hawai‘i Tourism Authority (HTA or the Authority) concluded that a continuous drive to increase visitor numbers had taken a toll on Hawai‘i’s natural environment and people. What was needed was a “re-balancing” of priorities, and for that reason, “destination management” would be the Authority’s main focus and at the heart of the new strategic plan.

In its 2020 – 2025 Strategic Plan (its current plan), HTA defined destination management as: “attracting and educating responsible visitors; advocating for solutions to overcrowded attractions, overtaxed infrastructure, and other tourism-related problems; and working with other responsible agencies to improve natural and cultural assets valued by both Hawai‘i residents and visitors.” The plan also explained that destination concerns, such as attention to community benefits, Native Hawaiian culture, and workforce training, had always been a part of the Authority’s strategic plans; however, this time, HTA would be putting a greater emphasis on and devoting additional resources to that effort.

As part of its “greater emphasis” on destination management, and with a goal of rebuilding, redefining, and resetting the direction of tourism over a three-year period, HTA developed three-year Destination Management Action Plans (DMAPs) for six islands, all of which terminated in 2024. Actions and sub-actions vary in the individual DMAPs, such as protecting and preserving culturally significant places and tourist “hotspots”; increasing communication, engagement and outreach efforts with the community, visitor industry, and other sectors; increasing enforcement and active management of sites and trails; advocating/creating more funding sources to improve infrastructure; and developing regenerative tourism initiatives.

What We Found

In Report No. 25-07, Audit of the Hawai‘i Tourism Authority, we assessed HTA’s achievement of its 2016 and 2020 – 2025 strategic plans’ destination management goals. We also evaluated the effectiveness of the agency’s DMAPs. We found that HTA’s new emphasis on destination management is not materially different from its prior efforts. Although not referred to as “destination management,” a large part of HTA’s previous strategic plan had outlined – and highlighted – the same goals as its current strategic plan. We concluded that HTA’s destination management effort is largely a reshuffling of past and continuing programs, done without changes in policies and procedures or proposed organizational adjustments. In addition, HTA’s self-described refocusing doesn’t seem to have involved any increased financial commitment; overall spending on destination management efforts remained generally level.

What didn’t change from previous audit findings was HTA’s inability or disinterest in reporting on its own performance against its strategic plan goals. HTA’s last three annual reports to the Legislature lacked analysis or reporting of the Authority’s own Key Performance Indicators and its progress toward achieving its destination management goals. In our review, we found that performance against two of these Key Performance Indicators, when adjusted for inflation, has not improved since 2019, calling into question whether the Authority’s destination management efforts were effective.

We also found that HTA’s DMAP effort was largely ineffective. Most of the plans’ actions and sub-actions did not address hotspots, were underway or already completed, or were impractical. HTA funded many actions and sub-actions that seem unrelated to destination management, which HTA defines, generally, to mean attracting and educating responsible visitors and advocating for solutions to overcrowded attractions, overtaxed infrastructure, and other tourism-related problems. Moreover, we found that HTA’s tracking of the progress towards advancement of the hotspot-related sub-actions involved little more than filling out a to-do list. And, in the last year of the DMAPs, the Authority stopped tracking all DMAP actions and sub-actions altogether.

Why Did These Problems Occur?

HTA rushed its DMAP effort without a clear idea of what they were intended to achieve and how their actions would be prioritized. The Authority had no process or criteria for choosing who was on each steering committee. Similarly, HTA did not systematically choose how the DMAP actions and sub-actions would be implemented. There was also no criteria or process for choosing which projects would be funded to advance the DMAP goals. And, the Authority delegated much of the creation, management, and assessment of the DMAPs to third-party contractors, the community, and the island steering committees. Instead of leading this important aspect of tourism planning, HTA deferred to others. In the end, all proposed projects were accepted.

More generally, HTA management is not held accountable by its board to meaningfully achieve the goals and objectives of HTA’s strategic plan. HTA lacks meaningful milestones and measures to track its progress against its strategic initiatives. HTA’s Key Performance Indicators, which it uses to track performance, are the same broad metrics that HTA used to measure its success before it adopted the current strategic plan with its “emphasis” on destination management. Those indicators are not meaningful in measuring, for instance, the impacts of tourism on infrastructure and natural resources. And, none of the Key Performance Indicators seem designed to gauge progress in addressing resident concerns about visitor impacts, generally, and about hot spots, specifically.

Why Do These Problems Matter?

Without adequate HTA leadership and oversight, the DMAP actions and sub-actions were efforts that were dubious or impractical, little more than elaborate tourism to-do lists and rosters of various, unconnected actions. For instance, “hotspots,” determined by the various island steering committees, are locations where visitors and residents compete for access, and where mitigating congestion and overcrowding could increase resident support for tourism. HTA did not adequately identify or vet hot spots or the community concerns about them. As a result, relatively few of the resultant actions and sub-actions addressed hot spots and their perceived issues.

However, HTA’s most persistent issue may be its most concerning. The Authority’s continued inability or reluctance to demonstrate its overall effectiveness for meeting its tourism goals undermines its credibility with the public and policymakers, as well as its ability to effectively make evidence-driven decisions and allocate resources to its destination management efforts.

Teens under 18 have been required to complete State-certified driver education to qualify for driver’s licenses since January 2001. However, as noted in House Concurrent Resolution No. 125 (2022 Regular Session), many students have been unable to enroll in driver education – particularly students from neighbor islands. According to the resolution, limited opportunities have led some neighbor island students to travel to O‘ahu to take driver education, while other prospective drivers delay getting their licenses until after they turn 18. The resolution asked the Auditor to examine the backlog of driver education opportunities and programs, including insufficient instructors and courses, to determine why many teens are unable to enroll in driver education, considering the Department of Education (DOE) offers driver education at public high schools throughout the state. Driver education courses are also available through commercial driving schools, but at a much higher cost: DOE charges $10 for classroom instruction and behind-the-wheel training, while commercial schools can charge as much as $550 to teach the same curriculum.

The resolution points out that two agencies are involved in high school driver education – DOE provides classroom instruction and behind-the-wheel training to students, and the Department of Transportation (DOT) certifies the curriculum used in those courses and the instructors (DOE teachers and instructors teaching at commercial driving schools) qualified to teach it. Because the two departments have distinctly different roles and responsibilities in the State’s driver education program, we audited them separately, although our analyses address certain issues relevant to both departments.

Department Of Education

DOE’s driver education program is incomplete, a loosely organized and inconsistent collection of school-level practices, that is incapable of being meaningfully evaluated.

DOE has offered driver education to Hawai‘i teenagers for more than a half-century. When it established a statewide driver education program in 1966, the Legislature deemed the need for such instruction to be a “matter of urgency,” a legislative “imperative,” citing the “needless loss of human life on the highways” and noting that there is clear-cut evidence that driver education and training can reduce such loss.

The Legislature authorized DOE to establish and administer a driver education program “at each public high school in the State” through Act 42, Session Laws of Hawai‘i (SLH) 1966. Such courses must be open to all state residents under age 19, including public and private school students, home-schooled teenagers, and age-eligible residents who have already graduated or are no longer in school. But the concisely worded act included none of the details necessary for the department to oversee the program. Instead, the Legislature instructed the department to provide those details, filling in the broad program outlined in the act through administrative rules.

What we found We found, nearly 60 years later, DOE has yet to act as the Legislature directed – and expected. It has neither promulgated administrative rules that would complete the program, nor developed comprehensive internal regulations or procedures to guide its internal operations. Notably, DOE did not promulgate rules after the enactment of Act 175, SLH 1999, which changed its voluntary high school driver education program into a mandatory course for prospective drivers, thereby increasing demand. As a result, DOE’s high school driver education program is incomplete, lacking adequate direction and detail. The failure to adopt rules compromises program transparency, accountability, consistency, and fairness. For example, during our audit, 35 of DOE’s 68 public high schools offered driver education courses, and we found there were 35 different ways that the instruction is made available to interested students.

We additionally found DOE has no way to measure demand for its courses, which prevents the department from meeting its mandate to employ “necessary instructors” who have met all certification requirements. To calculate the number of necessary instructors, DOE would first need to set targets for how many students it intends to teach and how many classes are needed to accommodate them, as well as take into consideration areas where the classes are needed. That policy needs to be developed through rulemaking.

Why do these problems matter? Without a complete program, there is no centralized administration and leadership. DOE has yet to establish how it intends and expects driver education to be offered at its high schools. For instance, there are no policies and procedures describing how schools ensure enrollment in the driver education program is equitable to all eligible residents, including those who do not attend the school offering the course.

The absence of consistent guidance has left schools to figure out for themselves whether to offer driver education. Surveys and interviews with principals, school-level coordinators, and driver education instructors, as well as reviews of school websites, revealed an array of different strategies for enrolling students. The distributed nature of the program has rendered DOE unable to estimate the demand for driver education, or to identify and quantify a backlog of students wanting to enroll in a driver education class.

We recommend, among other things, that DOE promulgate administrative rules that articulate the department’s policy with respect to driver education in its high schools, including how it intends to provide instruction to age-eligible students, the priorities and prerequisites for enrollment, how individuals apply to enroll in a course, and consistent application procedures, including how to maintain waitlists.

Department Of Transportation

A lack of meaningful management oversight and interest in DOT’s driver education program resulted in an unequal certification process for instructors and impeded efforts to expand access to students statewide.

Act 175, SLH 1999, gave DOT new responsibilities related to high school driver education, tasking the department with ensuring instruction was appropriate and standardized, and certifying driver education instructors who have fulfilled all legal requirements. DOT promulgated administrative rules that outline how student, instructor, and master trainer curricula are to be selected and certified, which went into effect in 2006. Among other things, the rules require the DOT Director to appoint task forces to select and recommend student and instructor curricula for certification, while the DOT Director has sole discretion for certifying curricula used to teach master trainers who train new instructors.

DOT is also responsible for certifying driver education instructors who have met all requirements in accordance with the department’s rules, which include completion of a DOT-certified course for new instructors. DOT also processes instructors’ annual and 5-year renewal applications.

What we found Not only has the DOT Director neglected to form the required task forces, during the audit period, the director had not certified any driver education course curricula – not the student curriculum; not the instructor curriculum; and not the master trainer curriculum. The curricula are fundamental to and necessary for the department to perform its primary responsibility of certifying instructors and ensuring students receive appropriate driver education instruction. Without any certified course curricula, DOT cannot fully comply with other legal requirements, such as issuing certificates to driver education instructors who have “successfully completed a training class certified or subsequently certified by the department.”

The lack of certified curricula created a void that a lower-level Highway Safety Specialist stepped in to fill. A lack of internal controls – along with inaction and inattention from management – enabled the specialist to perform tasks assigned explicitly to the director, exercising authority well-beyond that conferred to the department. For instance, the specialist created requirements for master trainers that effectively eliminated DOE’s internal training program, then designated three other individuals to be master trainers despite the absence of a DOT Director-certified curriculum. We were told one of the three trainers was romantically involved with the specialist; property records show the two purchased a home together in 2023.

From 2022 until the Highway Safety Specialist abruptly resigned in August 2024, those three trainers, along with the specialist, controlled who could, and could not, teach driver education in Hawai‘i. This limited DOE’s ability to have new instructors trained, and inflated DOE’s costs to do so. The specialist also intruded on how DOE could offer instruction, such as prohibiting the use of substitute teachers and imposing a 14-student cap on virtual classes. House Concurrent Resolution No. 125 specifically called out DOT’s flexibility – or lack thereof – regarding virtual classes that could expand access to driver education courses, especially for neighbor island residents.

We found insufficient supervision allowed for unequal treatment of instructors seeking renewed certificates; instructors were suspended for late renewals, or for making minor mistakes on student certificates, and were required to take a paid course from one of the specialist’s designated trainers for reinstatement. In addition to suspending instructors, the specialist directed county examiners of drivers to turn away students who presented certificates issued by suspended instructors – even certificates that had been issued while an instructor’s certification was current. When a DOE coordinator attempted to assist students whose certificates of completion had been voided, the specialist responded by first suspending, then terminating the coordinator. After a delayed and flawed proceeding, the coordinator’s termination was reversed by the DOT Director without explanation.

Why do these problems matter? The Highway Safety Specialist’s unauthorized and unsupervised activities created havoc at both DOT and DOE. Her unequal treatment of instructors seeking renewed certificates led to reduced income for some driver education instructors, and financial gains for the three individuals she chose to be master trainers. As we reported, the Highway Safety Specialist required instructors she disciplined to pay her designated master trainers up to $200 for refresher courses to continue their driver education jobs. The Highway Safety Specialist’s actions against instructors also impacted students who had completed a driver education under a certified instructor who was subsequently suspended, delaying their ability to obtain a driver’s license.

The Highway Safety Specialist also impeded DOE’s ability to increase driver education opportunities by eliminating its internal master training program, which forced DOE to pay the DOT master trainers for new instructor training. This raised DOE’s costs for training new instructors, which is paid out of the driver education fund, a special fund that uses $2 collected from each insured vehicle in Hawai‘i to support DOE’s driver education and traffic safety programs.

While DOT claimed to have tried to rein in its employee, we recommend defining clearly, in writing, the roles, responsibilities, and limits of authority, as well as the Motor Vehicle Safety Office Administrator’s supervisory responsibilities over anyone administering the program.

The Highway Safety Specialist’s misuse of her position undermined the integrity of the program; however, just as damaging and maybe more concerning is the DOT administration’s lack of presence and awareness, which allowed her to operate unchecked for so long.

Single Audit of Federal Financial Assistance Programs of the State of Hawai‘i

Financial Statements, Fiscal Year Ended June 30, 2024

THE PRIMARY PURPOSE of the State Single Audit for the fiscal year ended June 30, 2024, was to comply with Title 2, U.S. Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The State Single Audit was conducted by Accuity LLP.

Auditors’ Report on Internal Controls over Financial Reporting

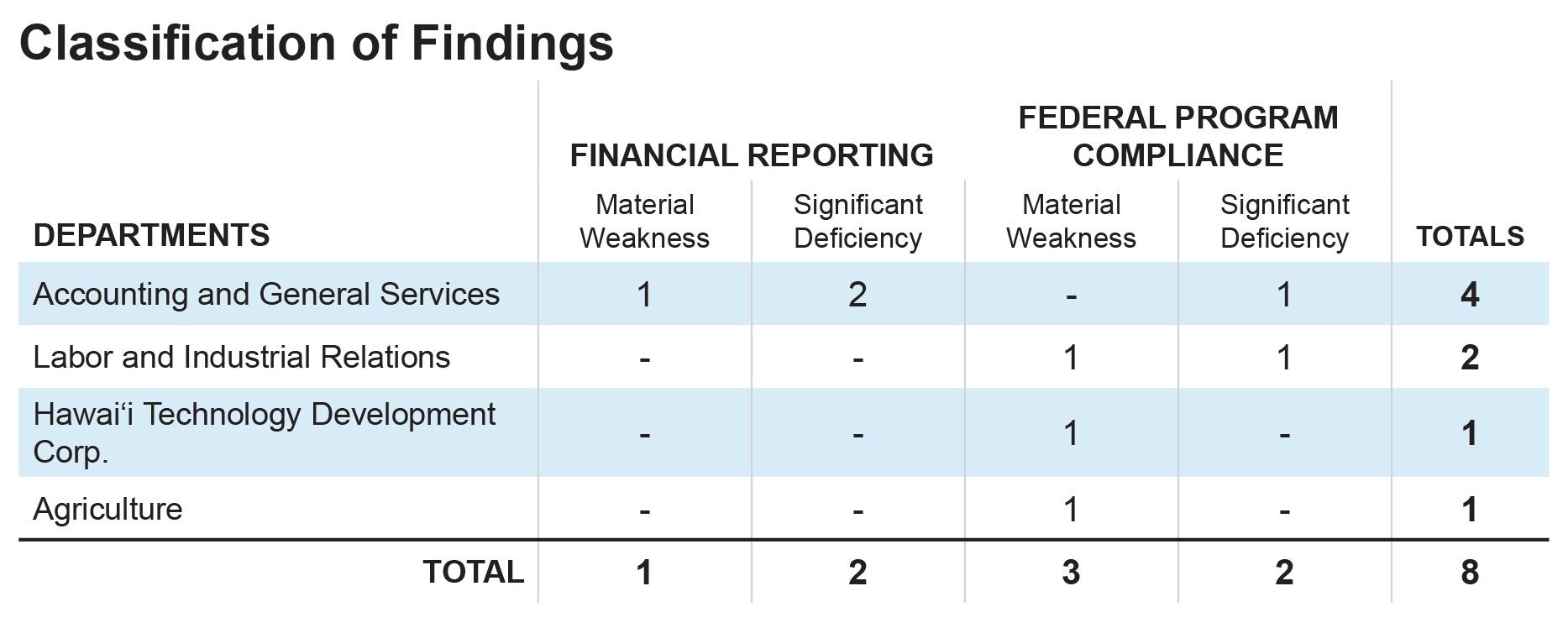

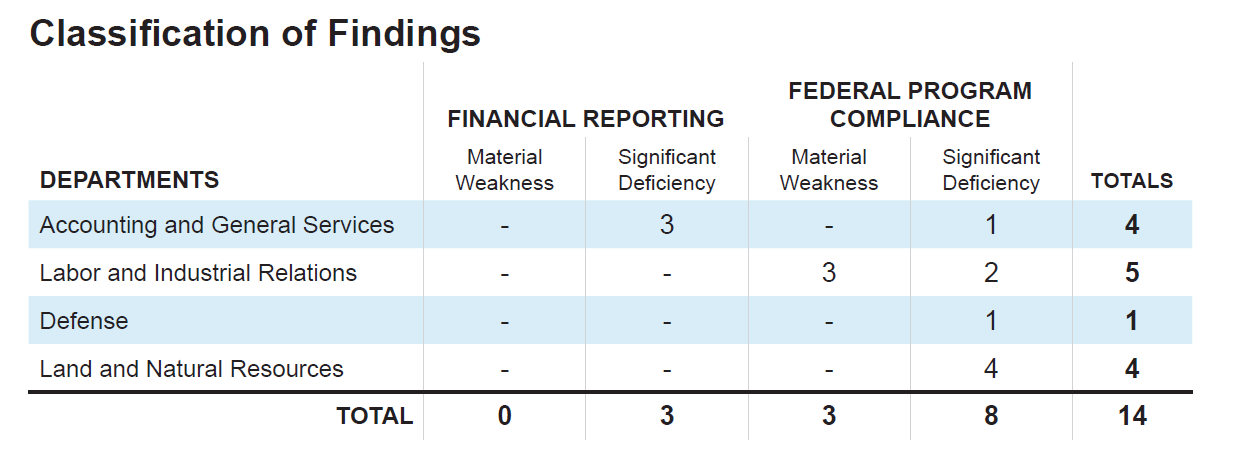

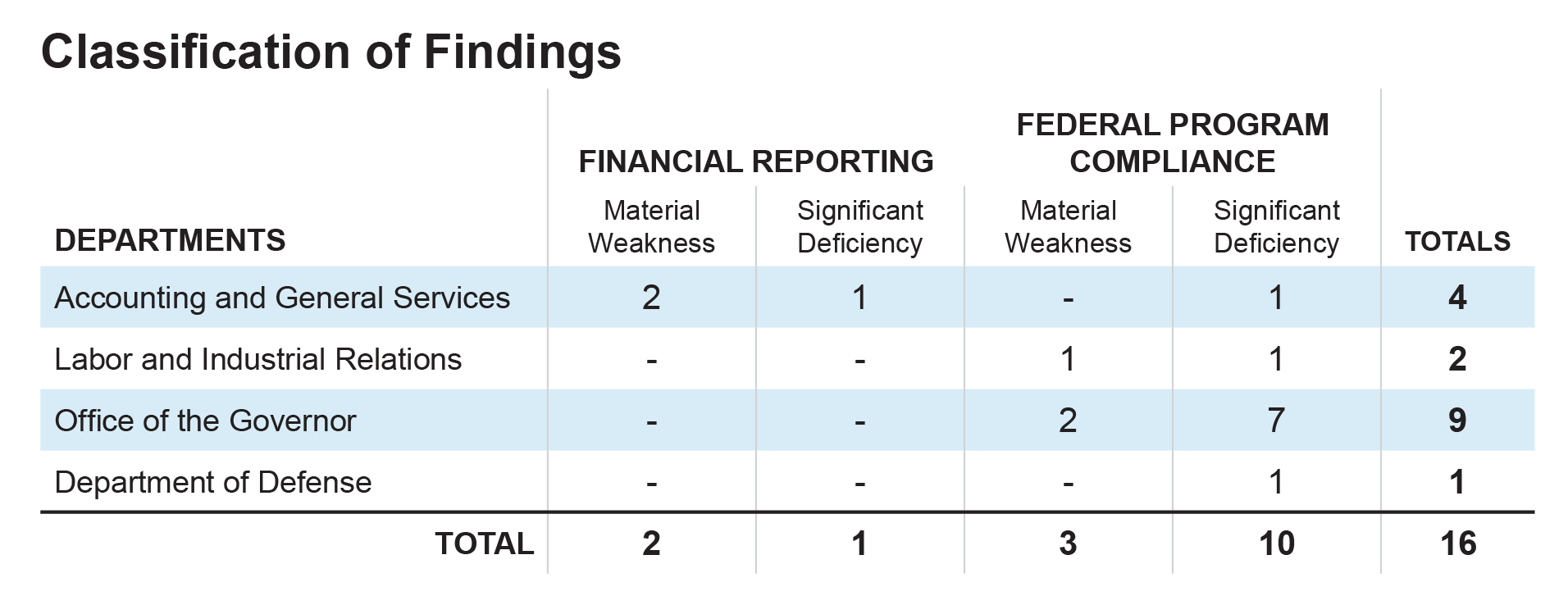

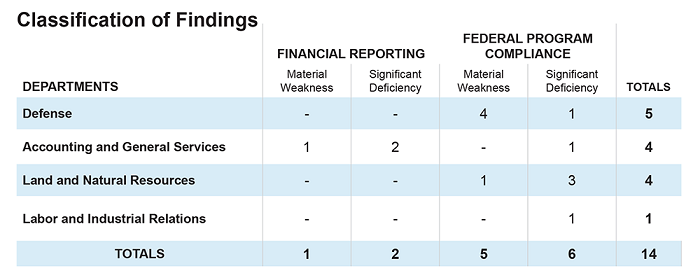

THE AUDITORS IDENTIFIED one material weakness and two significant deficiencies in internal controls over financial reporting that are required to be reported in accordance with Government Auditing Standards. A material weakness is a deficiency, or a combination of deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected, on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. The material weakness is described on pages 19-20 and the significant deficiencies are described on pages 21-23 of the report.

Auditors’ Report on Compliance with Major Federal Programs

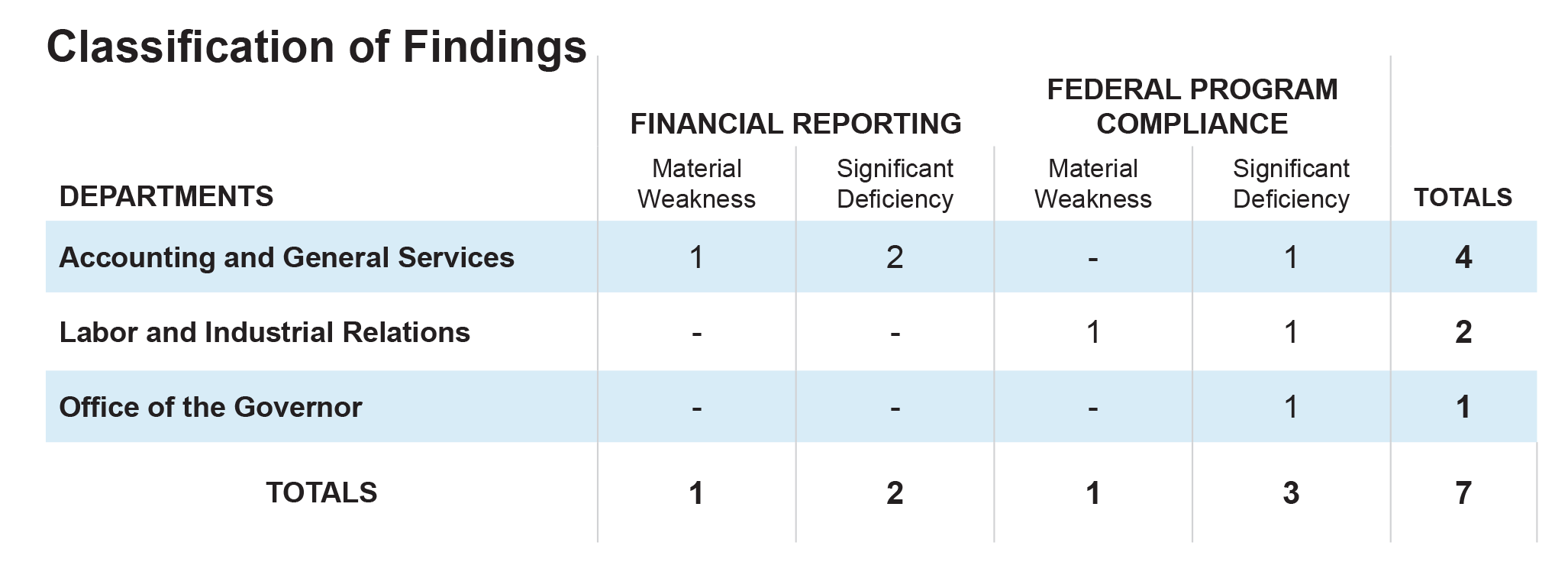

THE AUDITORS EXPRESSED A QUALIFIED OPINION on certain major programs and identified three material weaknesses and two significant deficiencies over compliance with major federal programs that are required to be reported in accordance with the Uniform Guidance. These findings are described in a Schedule of Findings and Questioned Costs that can be found on pages 24-28 of the report. A table with the number and type of findings by department can be found below.

A material weakness in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented or detected and corrected on a timely basis.

A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance.

About the Report

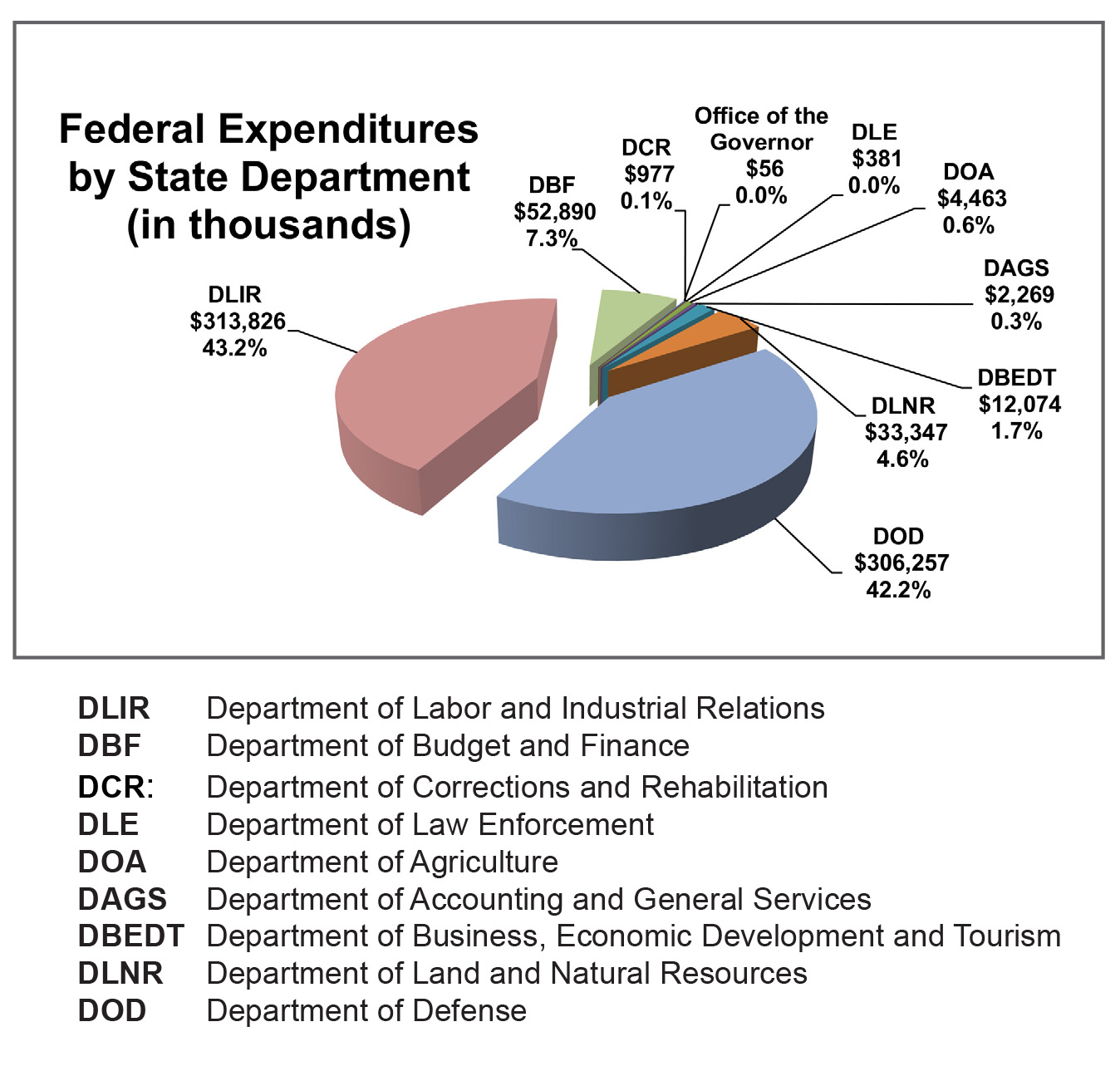

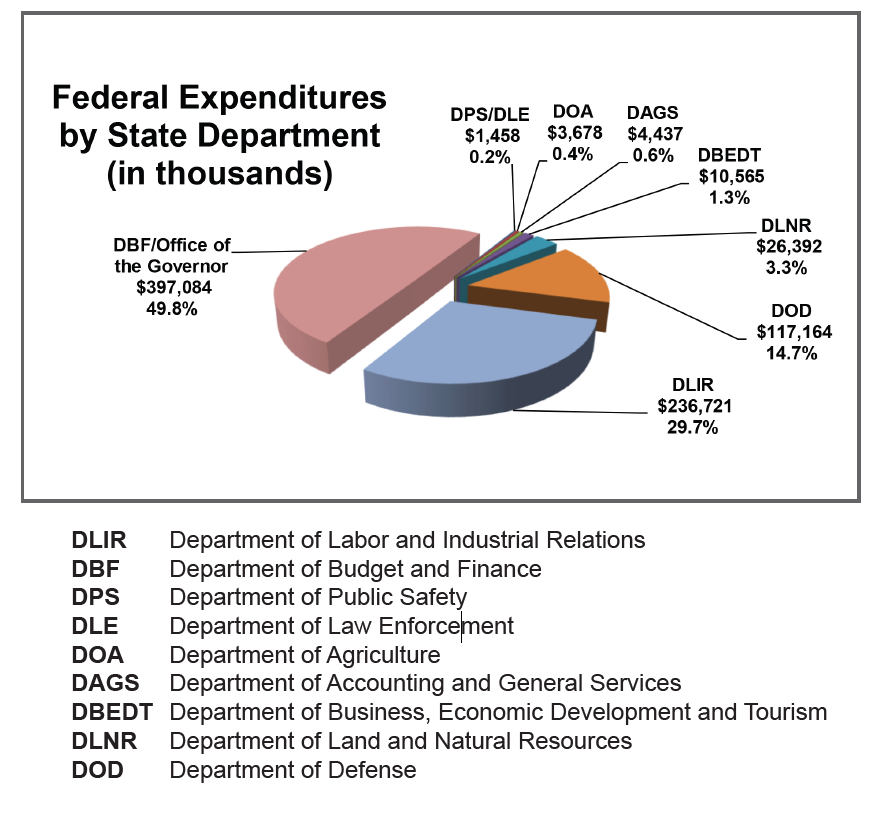

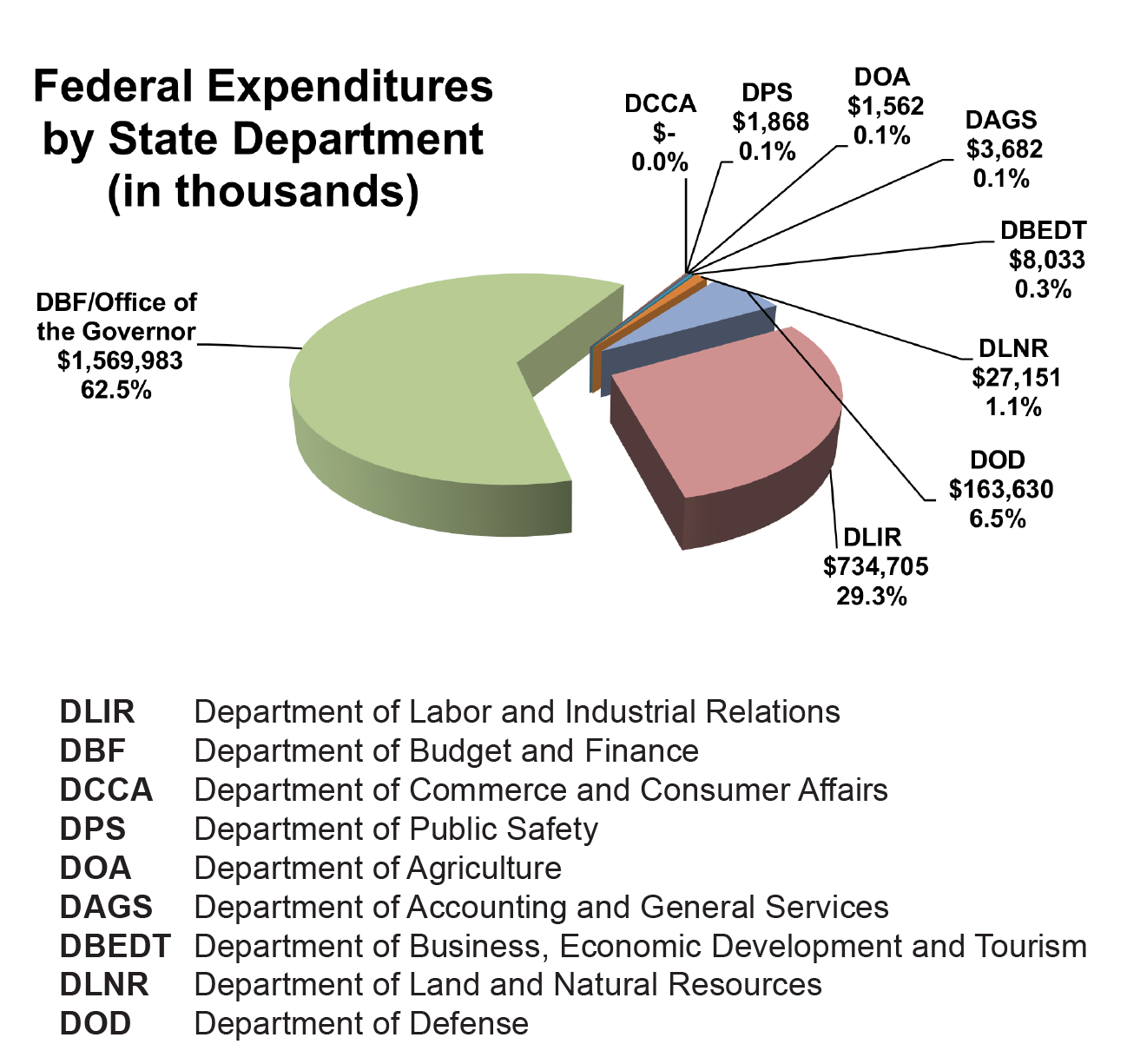

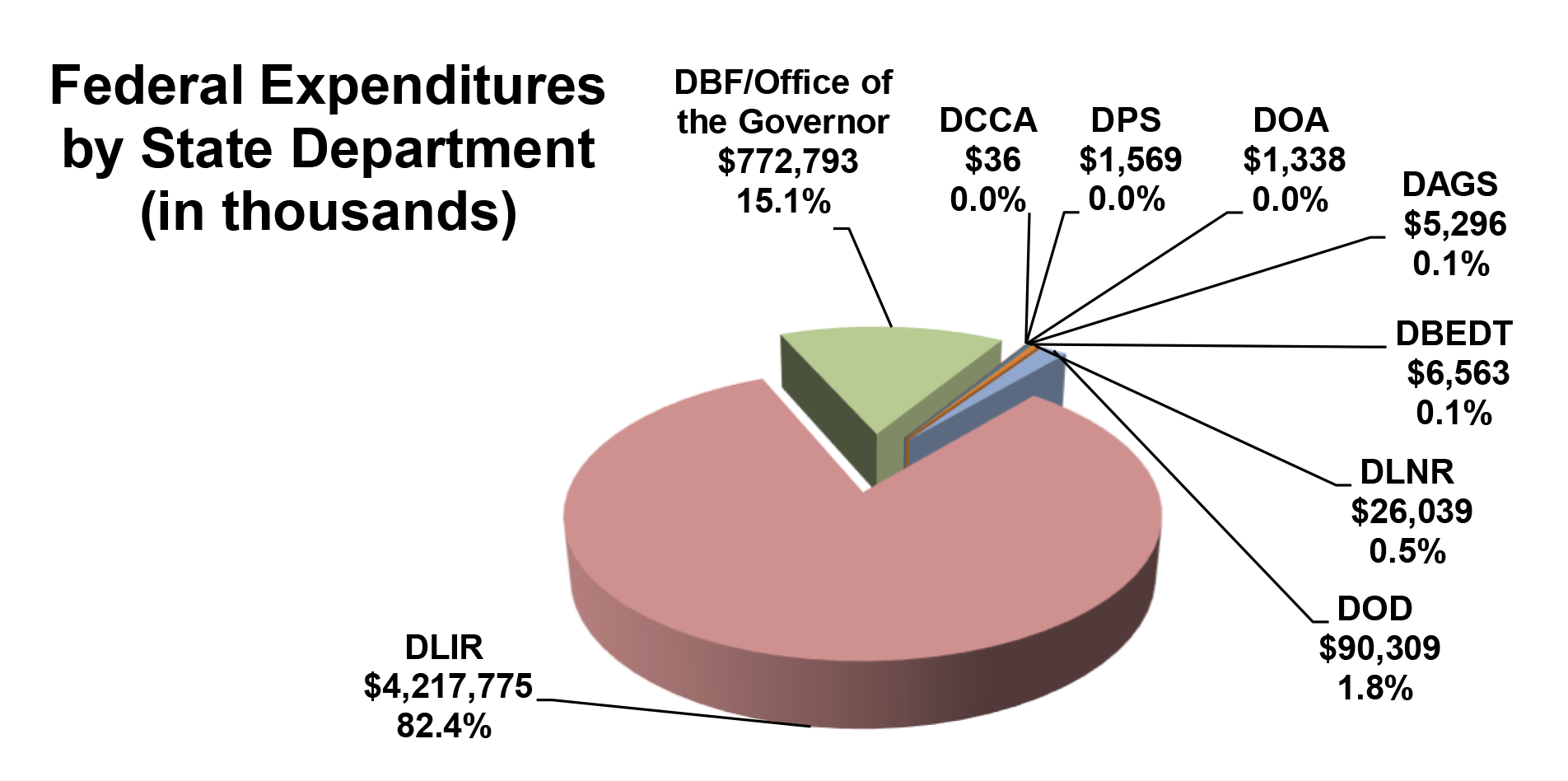

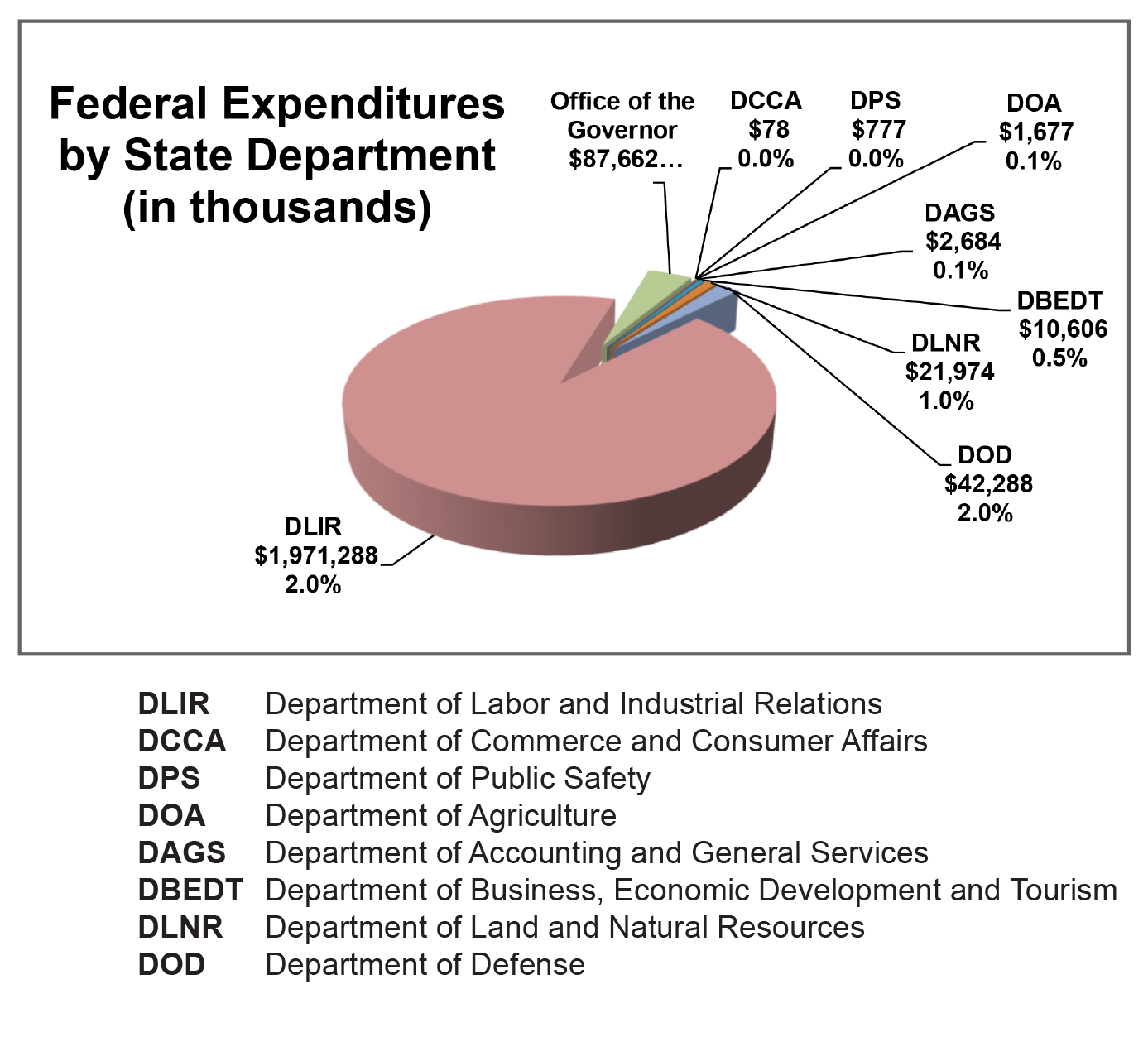

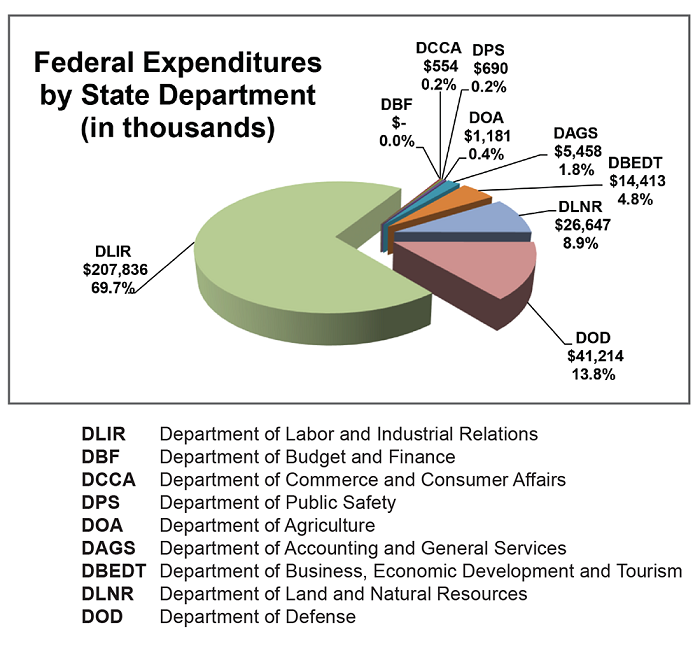

Single audits provide assurance to the federal government that state agencies and programs receiving federal funds are expending those funds properly. This report includes the total federal expenditures and findings related to departments that are included in the State of Hawai‘i Single Audit of Federal Financial Assistance Programs for the fiscal year ended June 30, 2024. For the departments included in the report that received federal monies, federal expenditures totaled approximately $726.5 million. Other departments’ federal expenditures and findings are reported in their individual single audit reports. For the audits procured by the Office of the Auditor, those reports are available through the Office of the Auditor’s website.

Financial Statements, Fiscal Year Ended June 30, 2024

THE PRIMARY PURPOSE of the Hawai‘i Public Housing Authority Single Audit for the fiscal year ended June 30, 2024, was to comply with the Code of Federal Regulations, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, Title 2, Part 200 (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by Plante & Moran, PLLC.

About the Report

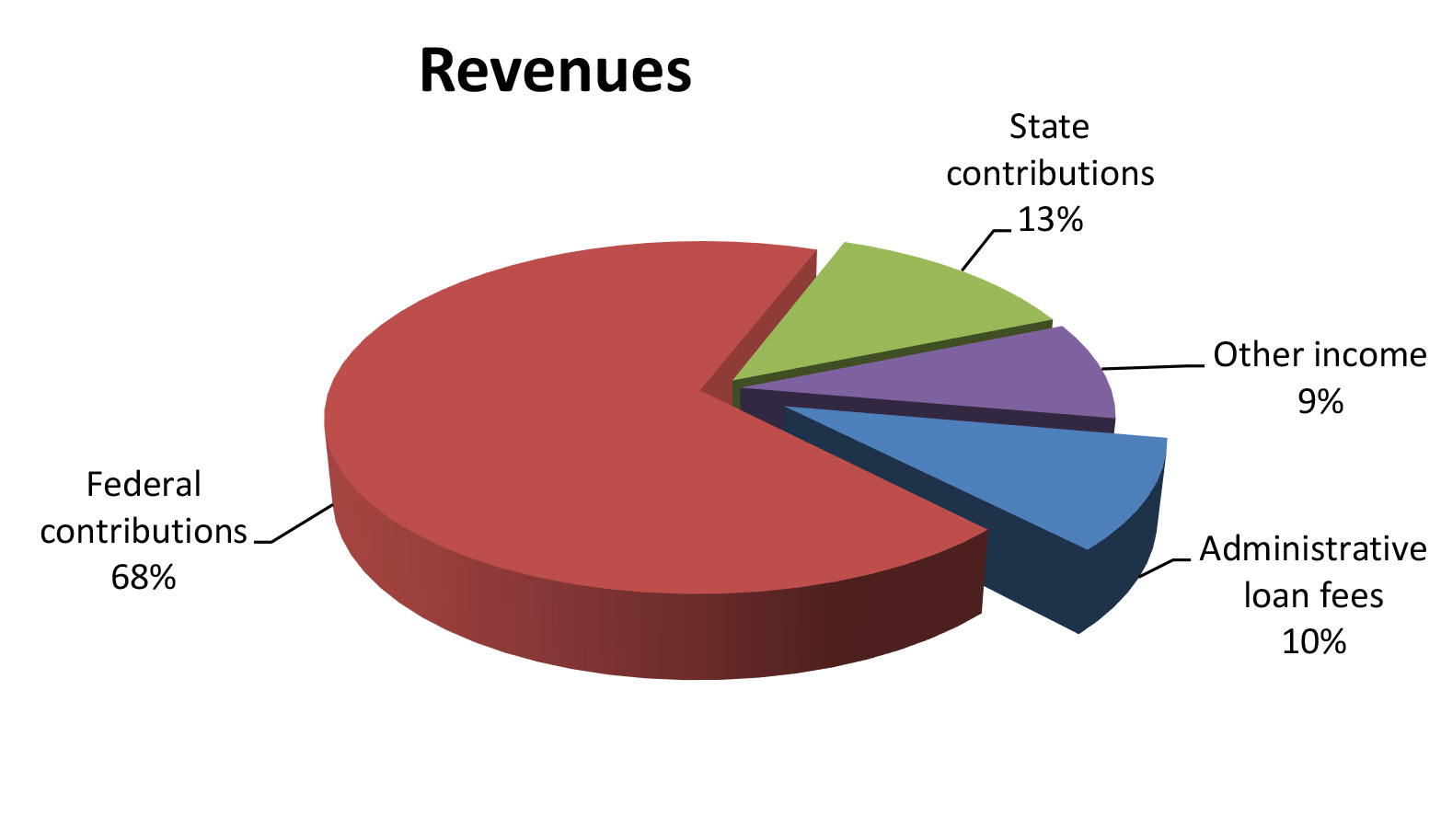

SINGLE AUDITS provide assurance to the federal government that state agencies and programs receiving federal funds are expending those funds properly. This report includes the total federal expenditures and findings related to the HPHA’s Federal Financial Assistance Programs for the fiscal year ended June 30, 2024. Federal expenditures totaled approximately $157.5 million.

Auditors’ Opinion HPHA RECEIVED AN UNMODIFIED OPINION on its compliance with major federal programs in accordance with the Uniform Guidance.

Findings THERE WERE NO MATERIAL WEAKNESSES in internal control over financial reporting that were required to be reported under Government Auditing Standards. There were no findings that were considered material weaknesses in internal control over compliance in accordance with the Uniform Guidance.

About the Division

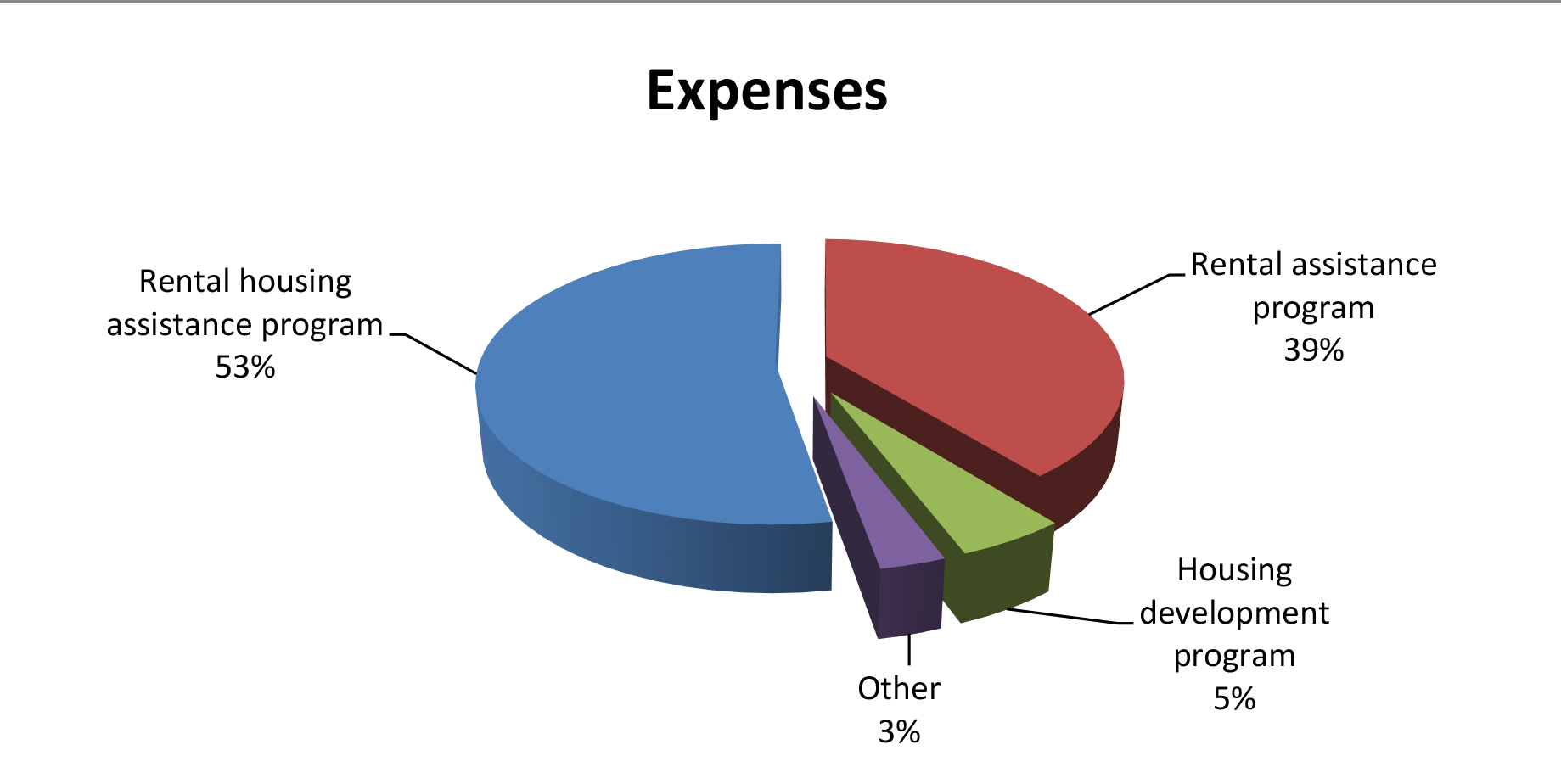

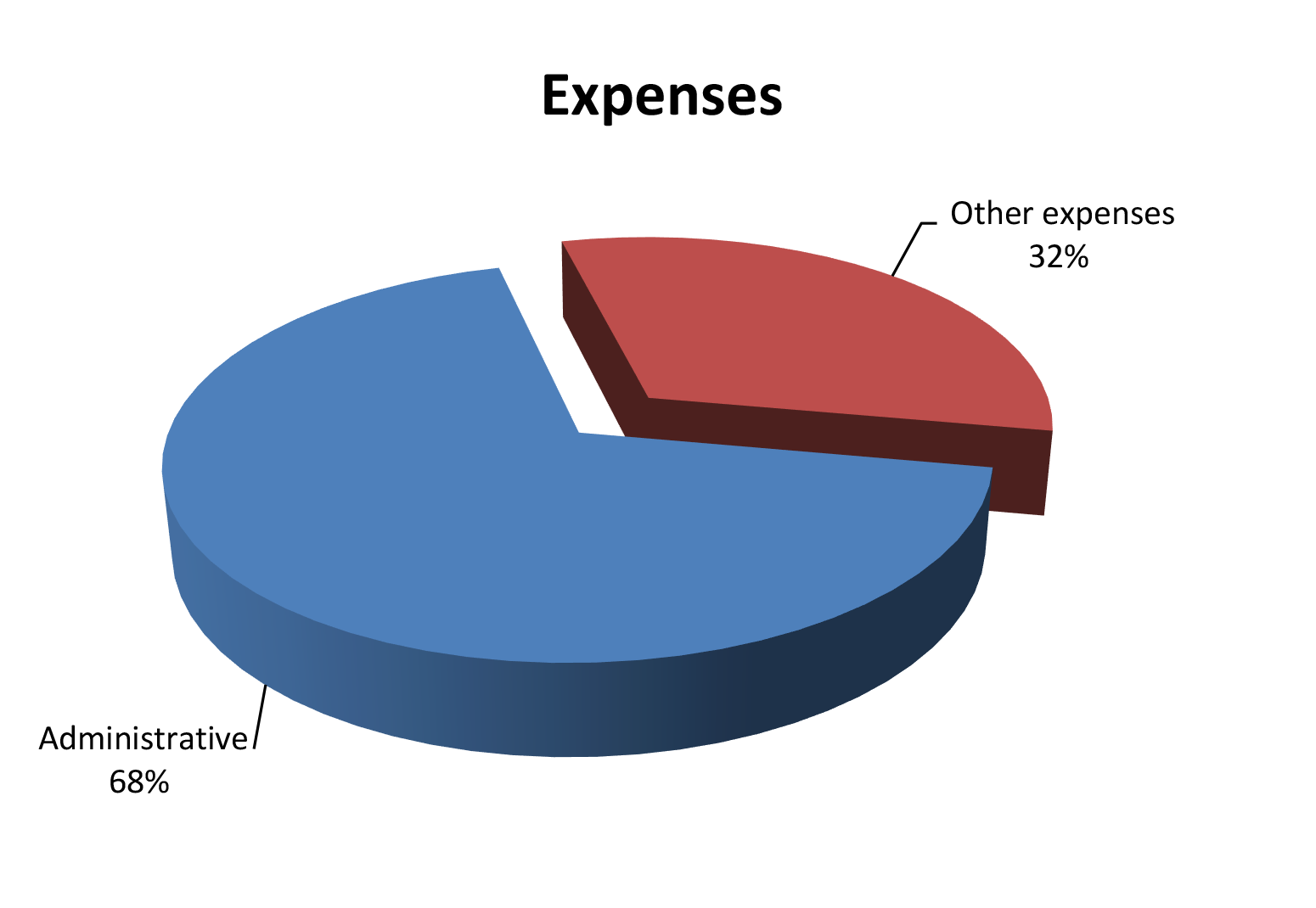

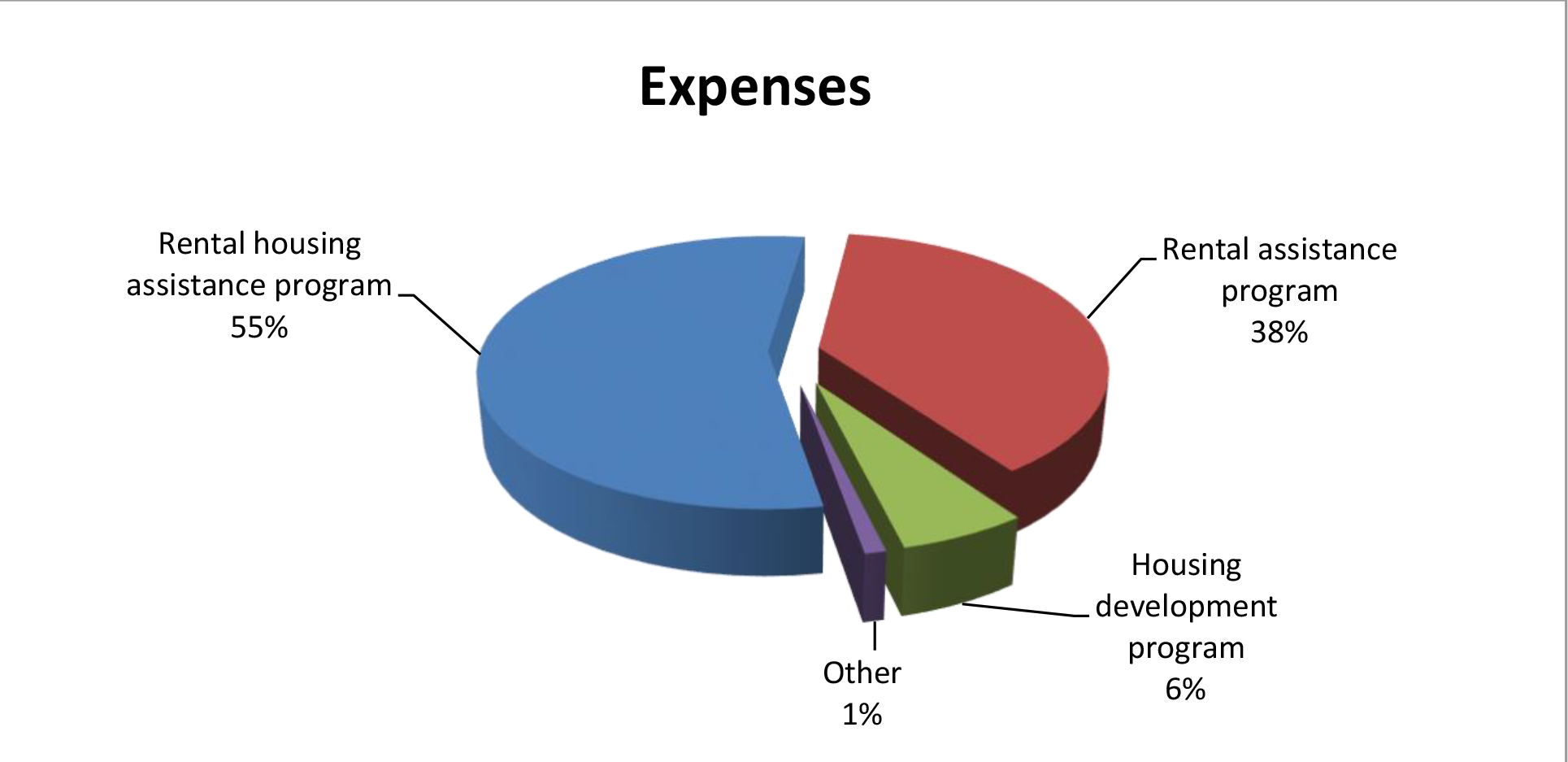

The mission of the Hawai‘i Public Housing Authority (HPHA) is to provide safe, decent, and sanitary dwellings for low and moderate-income residents of Hawai‘i and to operate its housing programs in accordance with federal and State laws and regulations. Some of HPHA’s housing assistance programs are funded by the U.S. Department of Housing and Urban Development.

HPHA is administratively attached to the Hawai‘i Department of Human Services (DHS). HPHA operates under the direction of its Executive Director and Board of Directors, which consists of eleven board members, nine of whom are appointed by the Governor. The Director of DHS and the Governor’s designee are ex-officio members.

Financial Statements, Fiscal Year Ended June 30, 2024

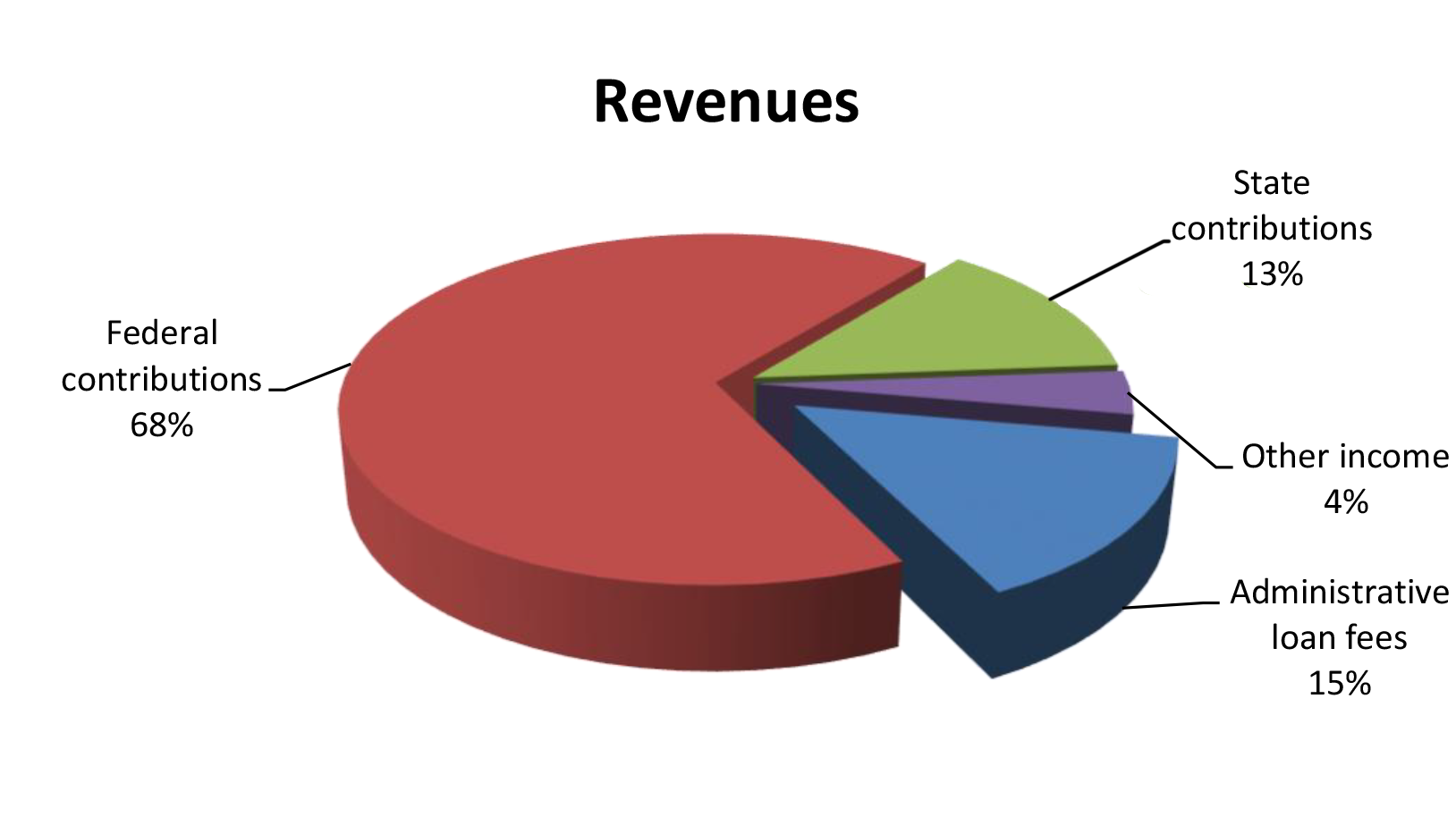

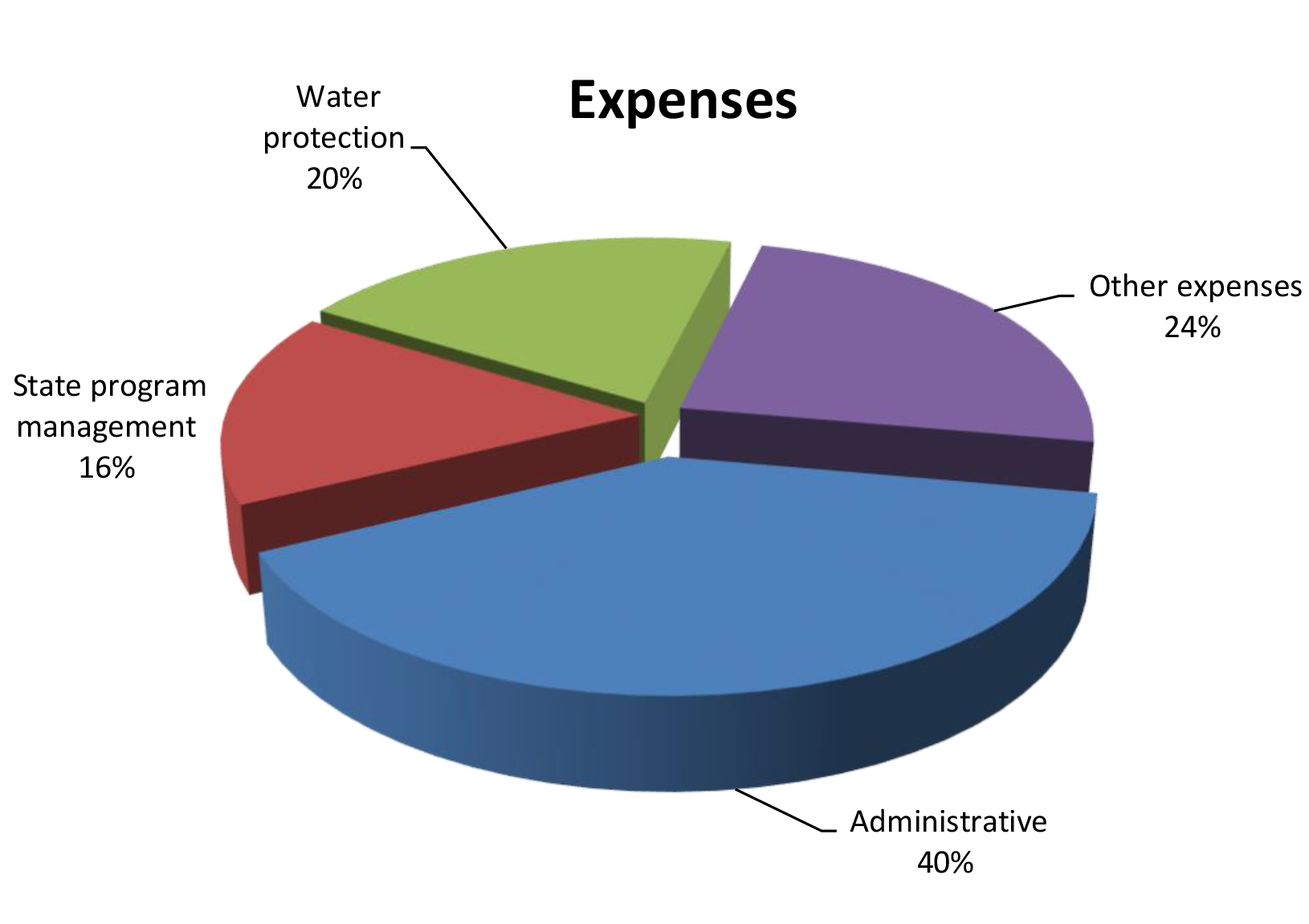

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the Department of Health, as of and for the fiscal year ended June 30, 2024, and to comply with Title 2, U.S. Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by KMH LLP.

Financial Highlights

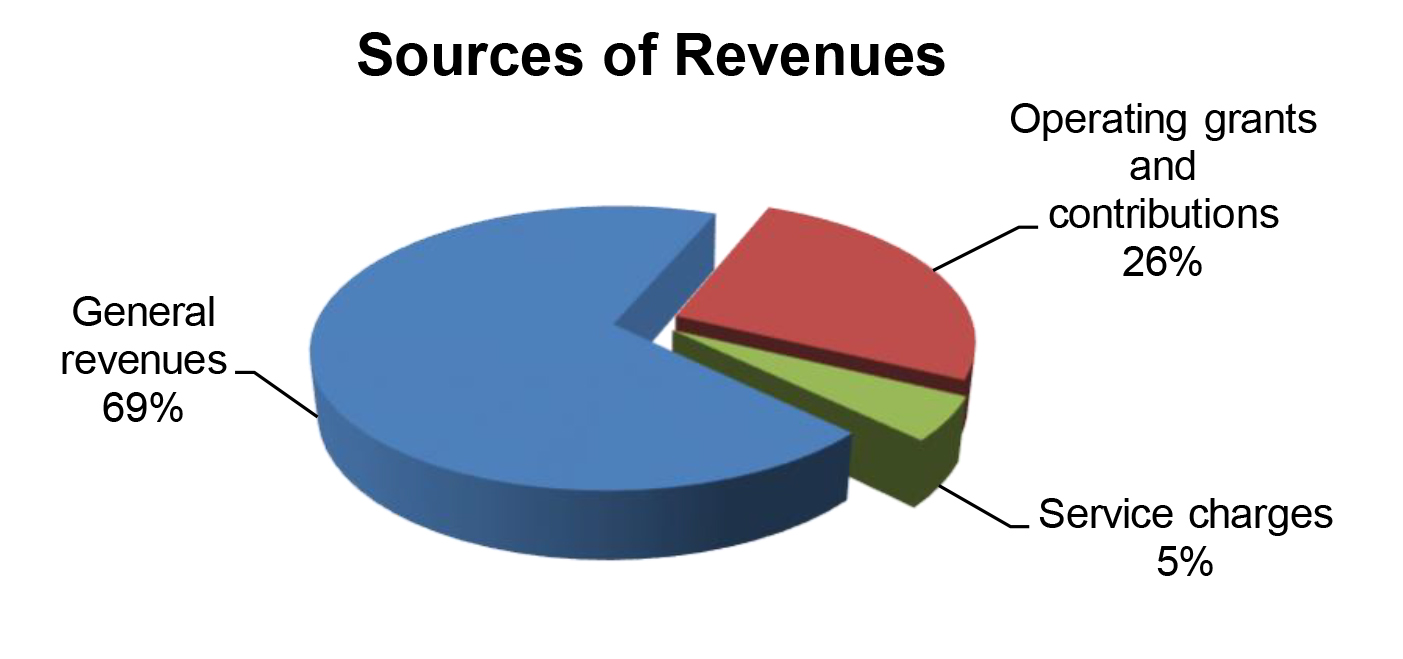

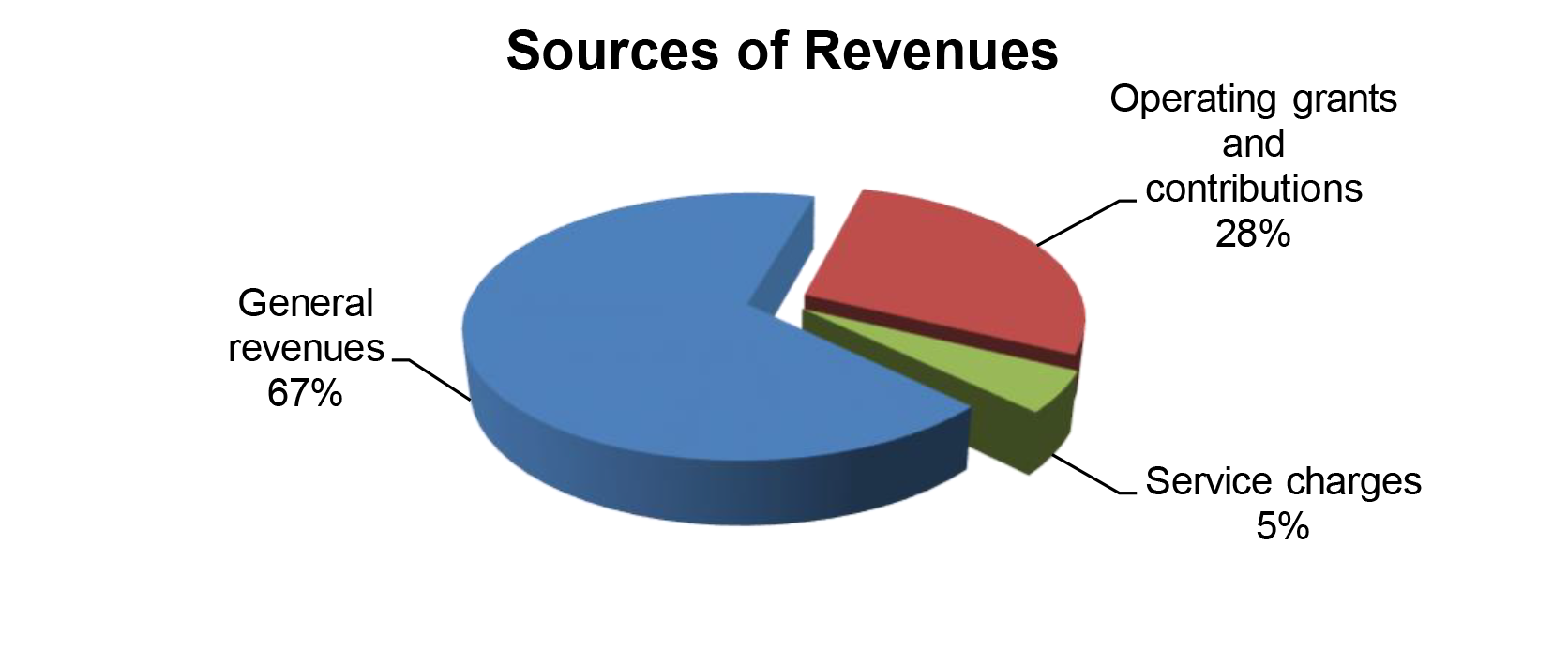

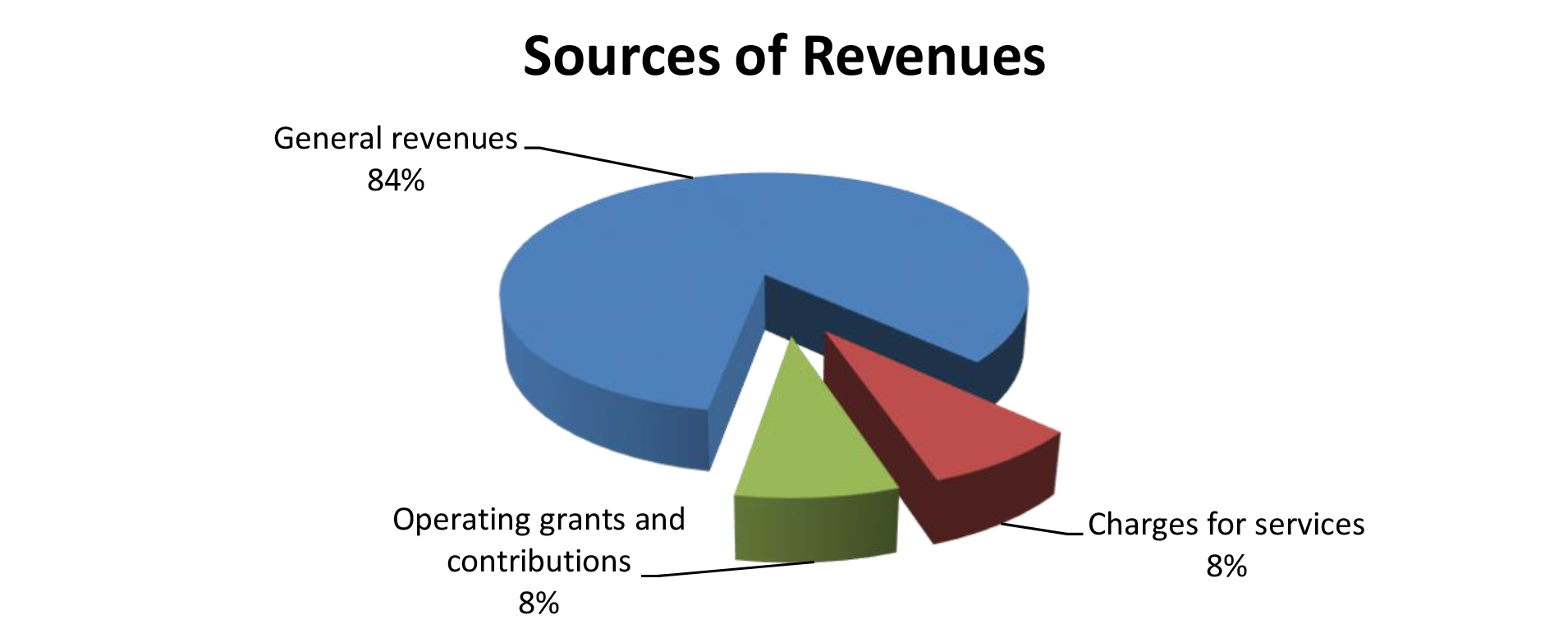

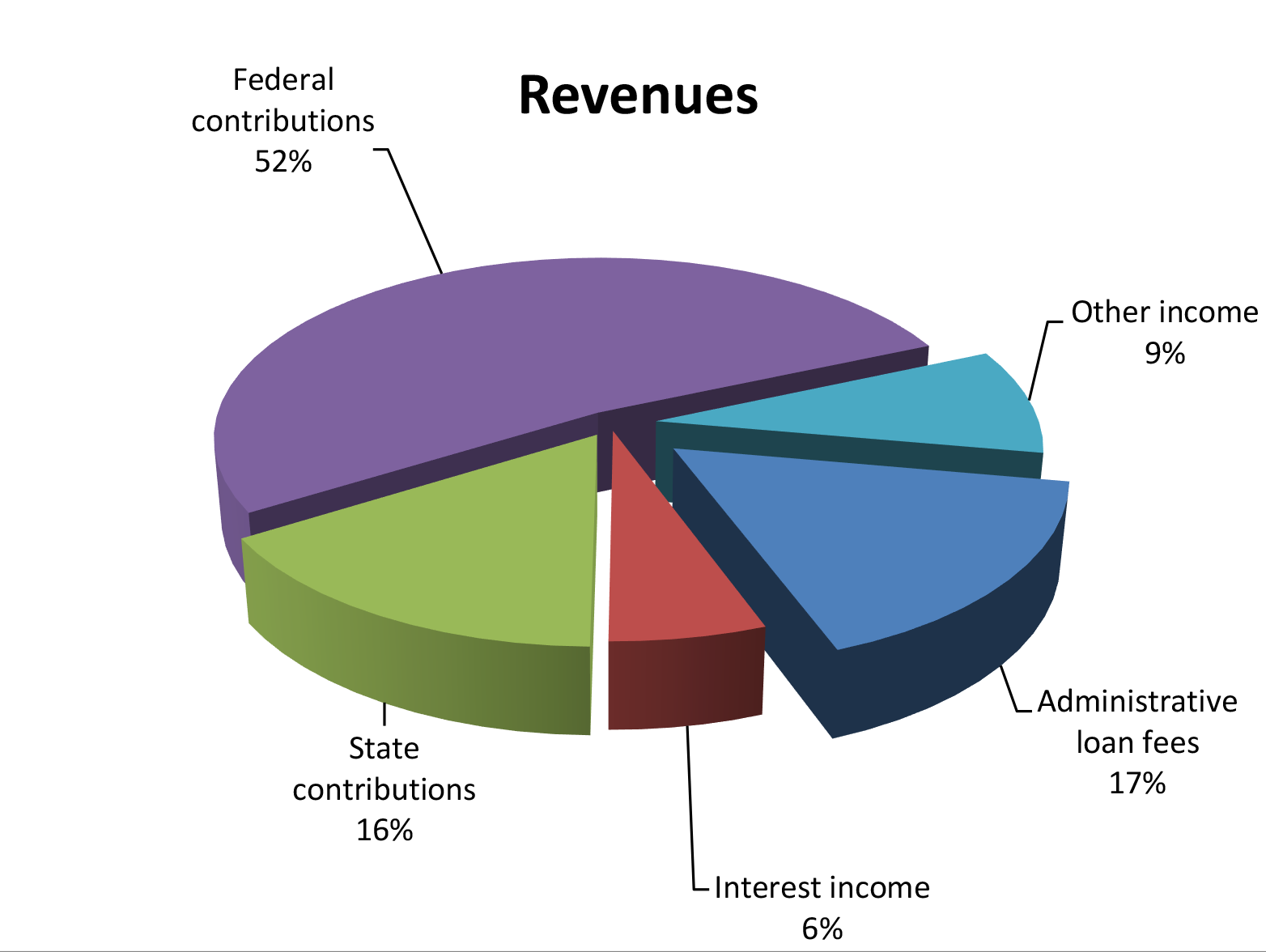

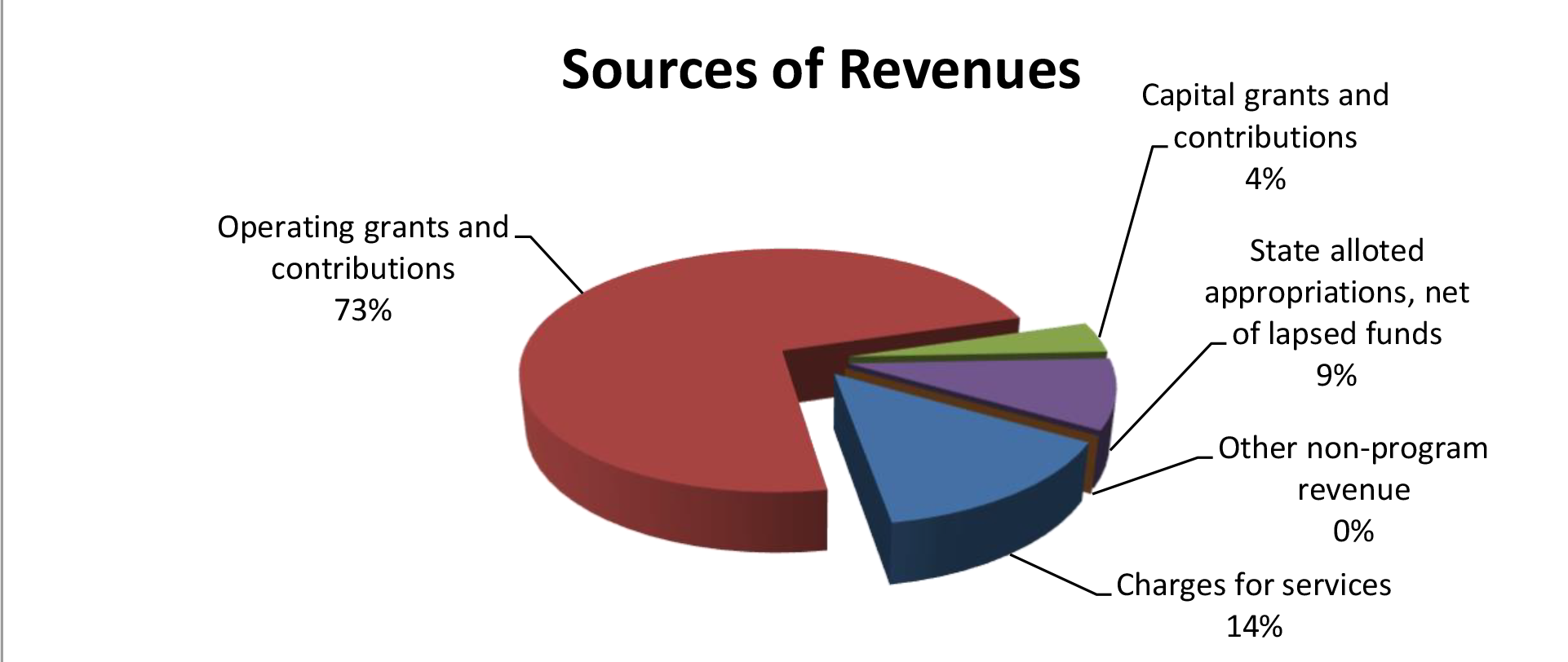

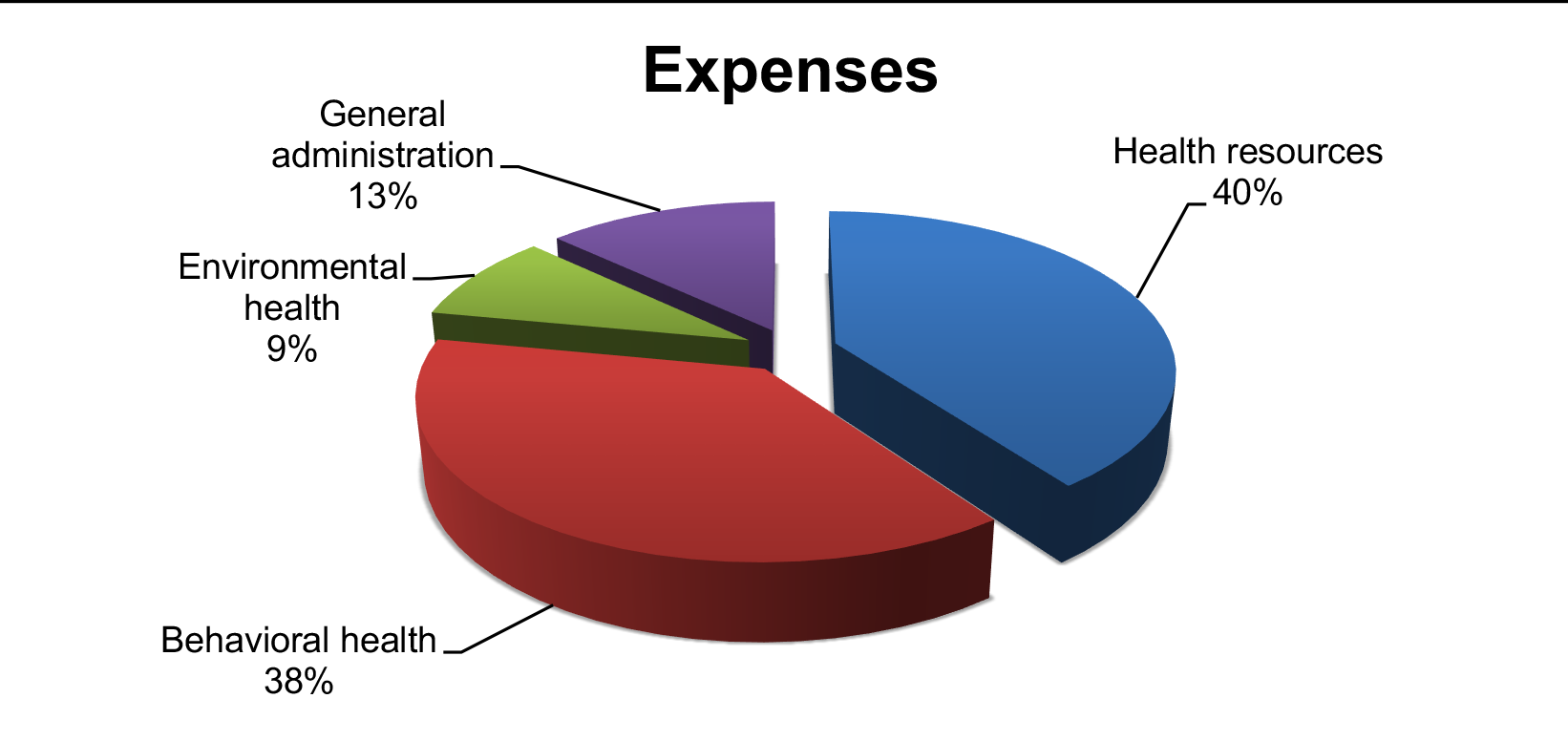

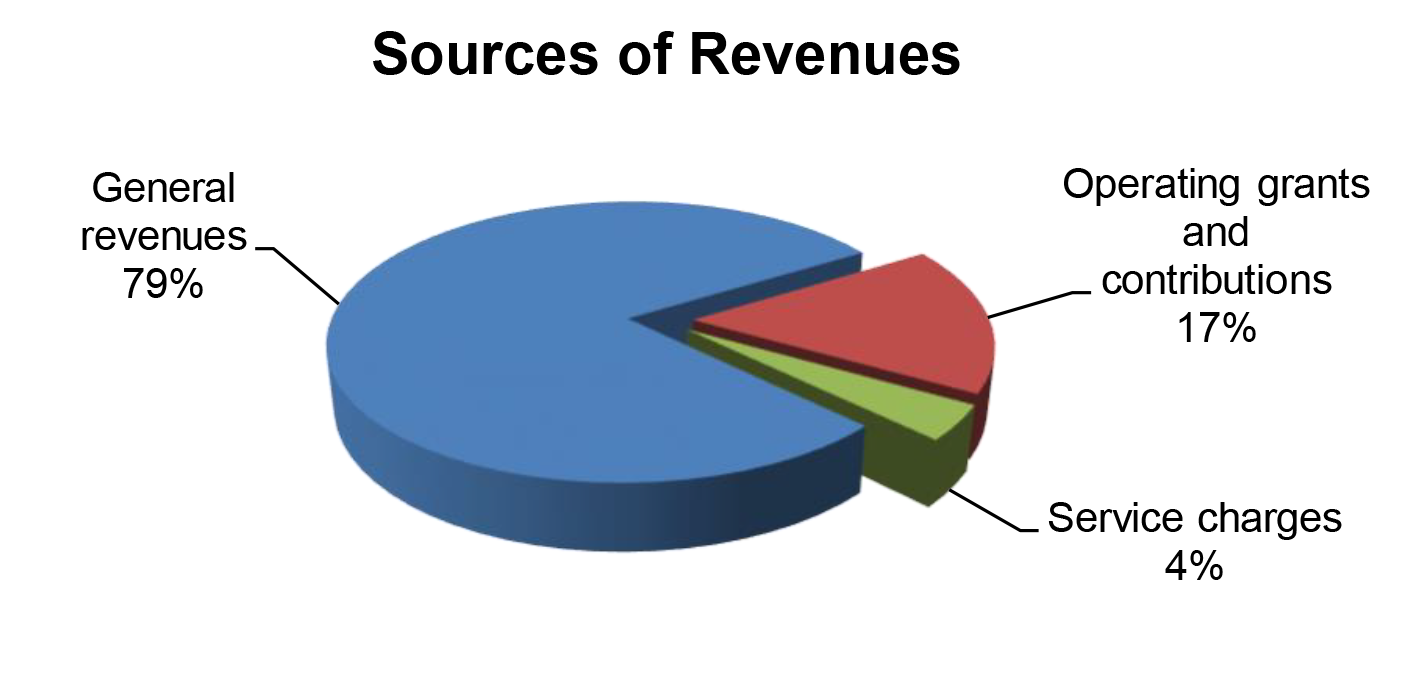

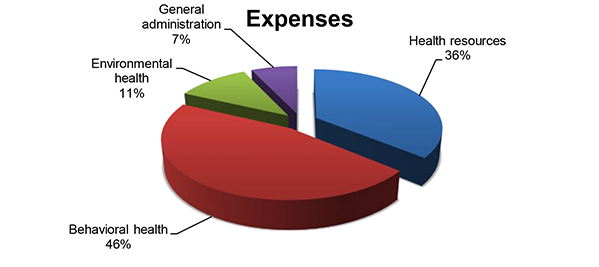

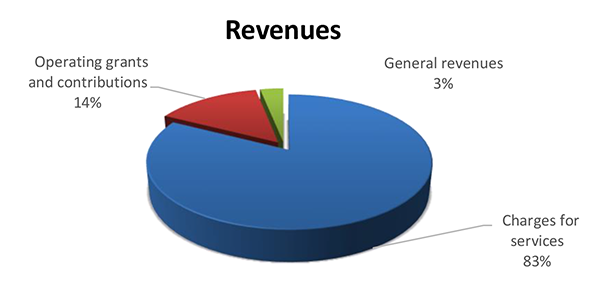

FOR THE FISCAL YEAR ended June 30, 2024, DOH reported total revenues of $1.04 billion and total expenses of $1.01 billion, resulting in an increase in net position of $29.1 million. Revenues included $719 million from general revenues, $274.3 million from operating grants and contributions, and $48.6 million from service charges.

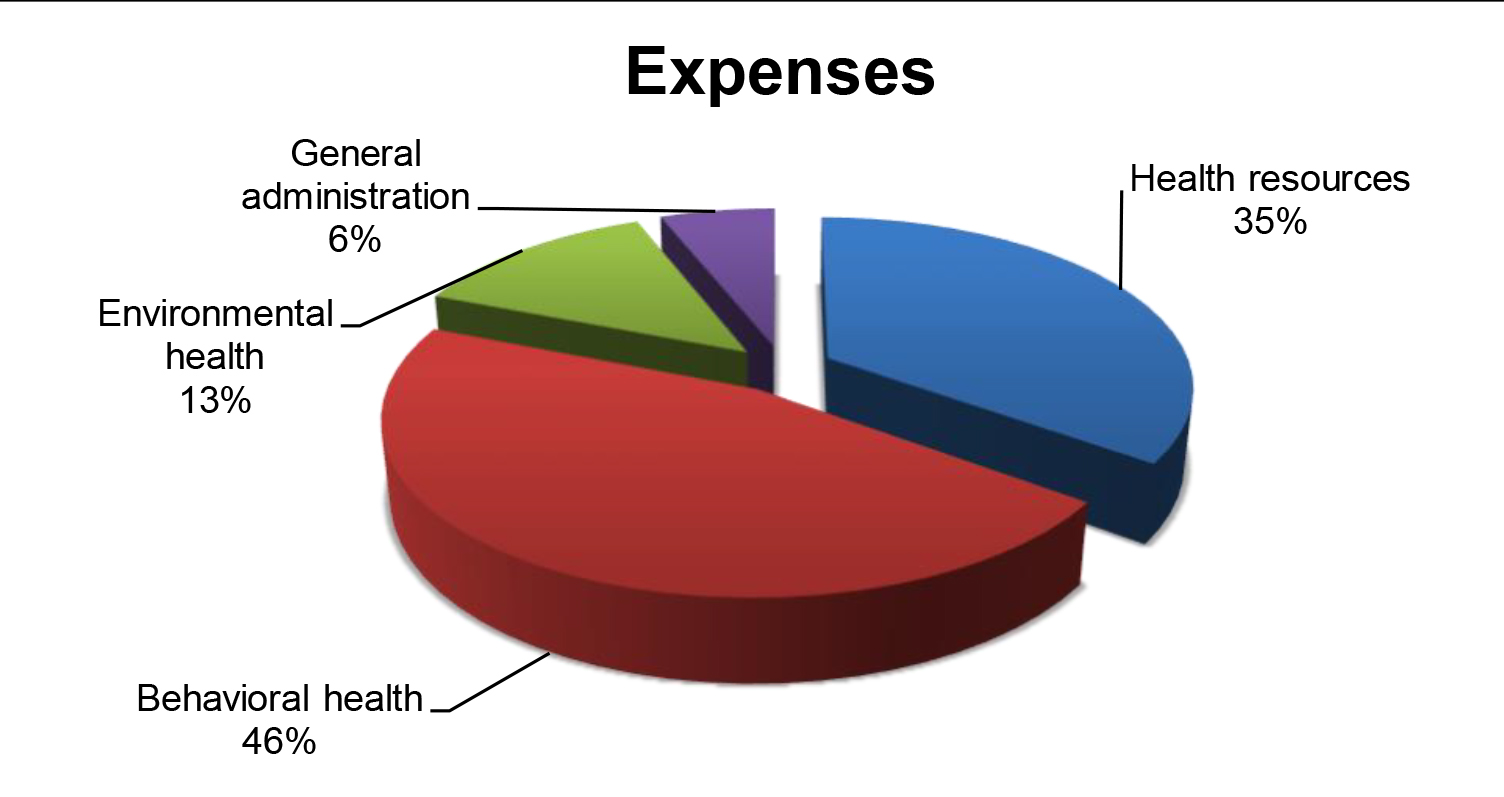

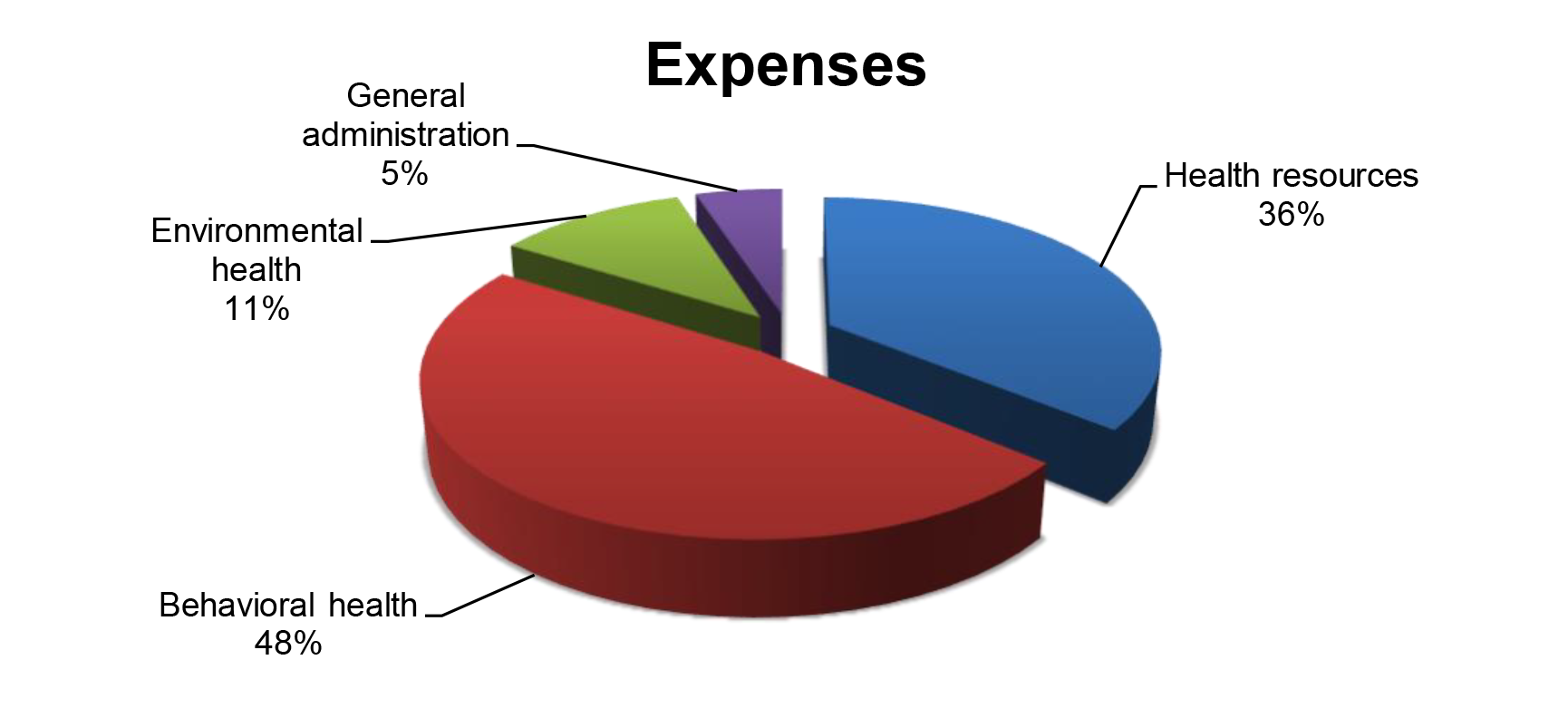

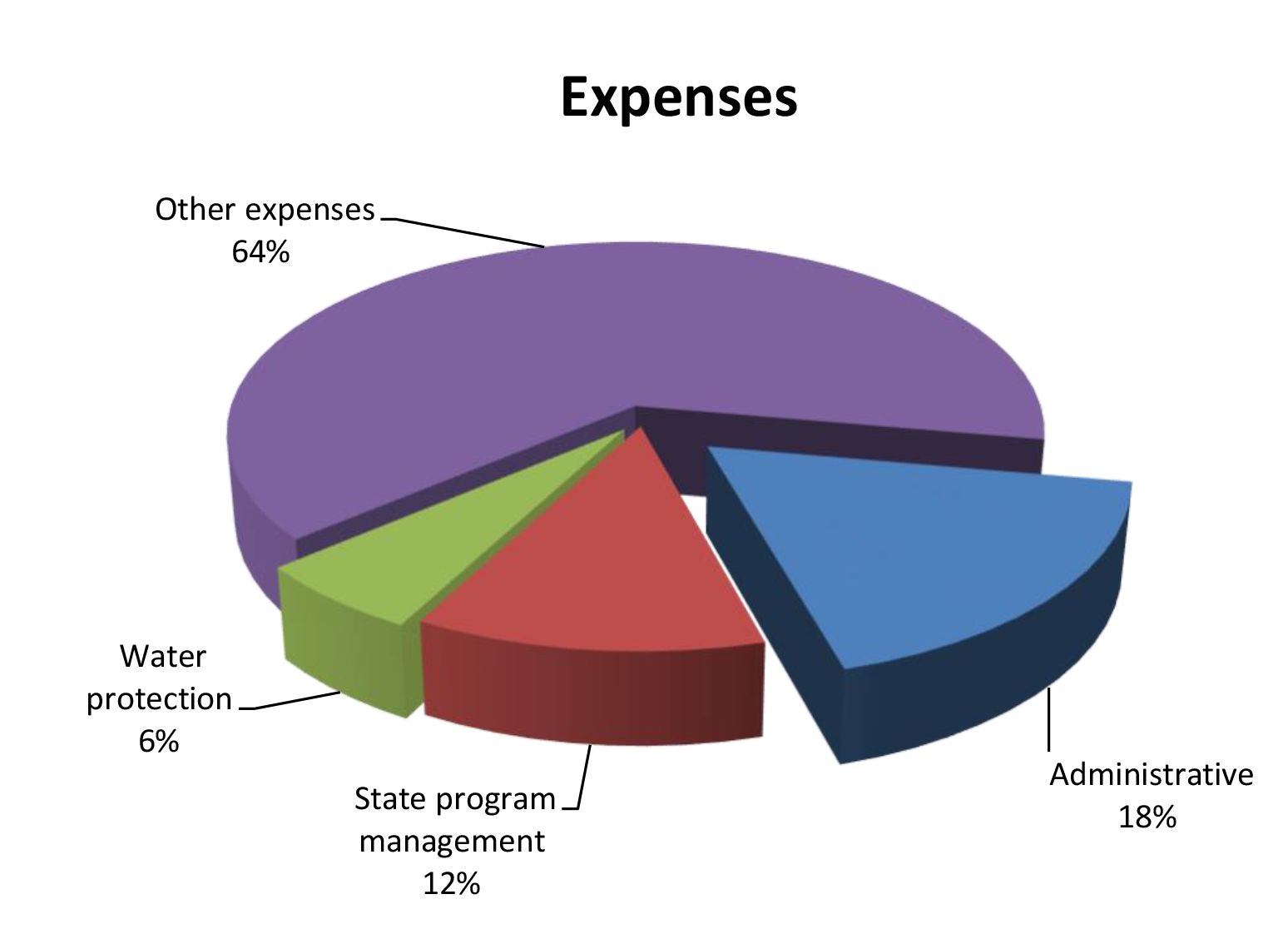

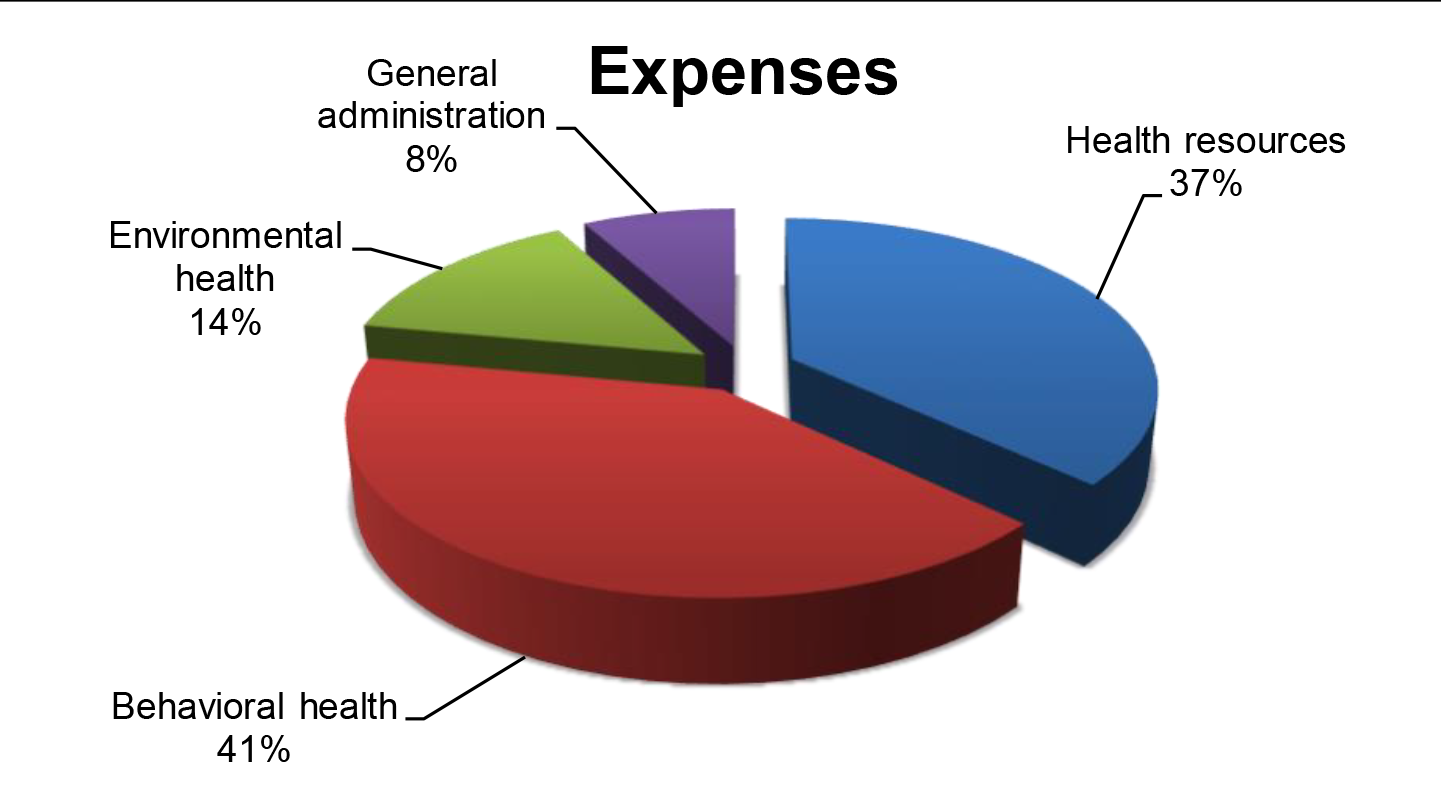

Expenses included $350 million for health resources, $461.2 million for behavioral health, $130.6 million for environmental health, and $70.9 million for general administration.

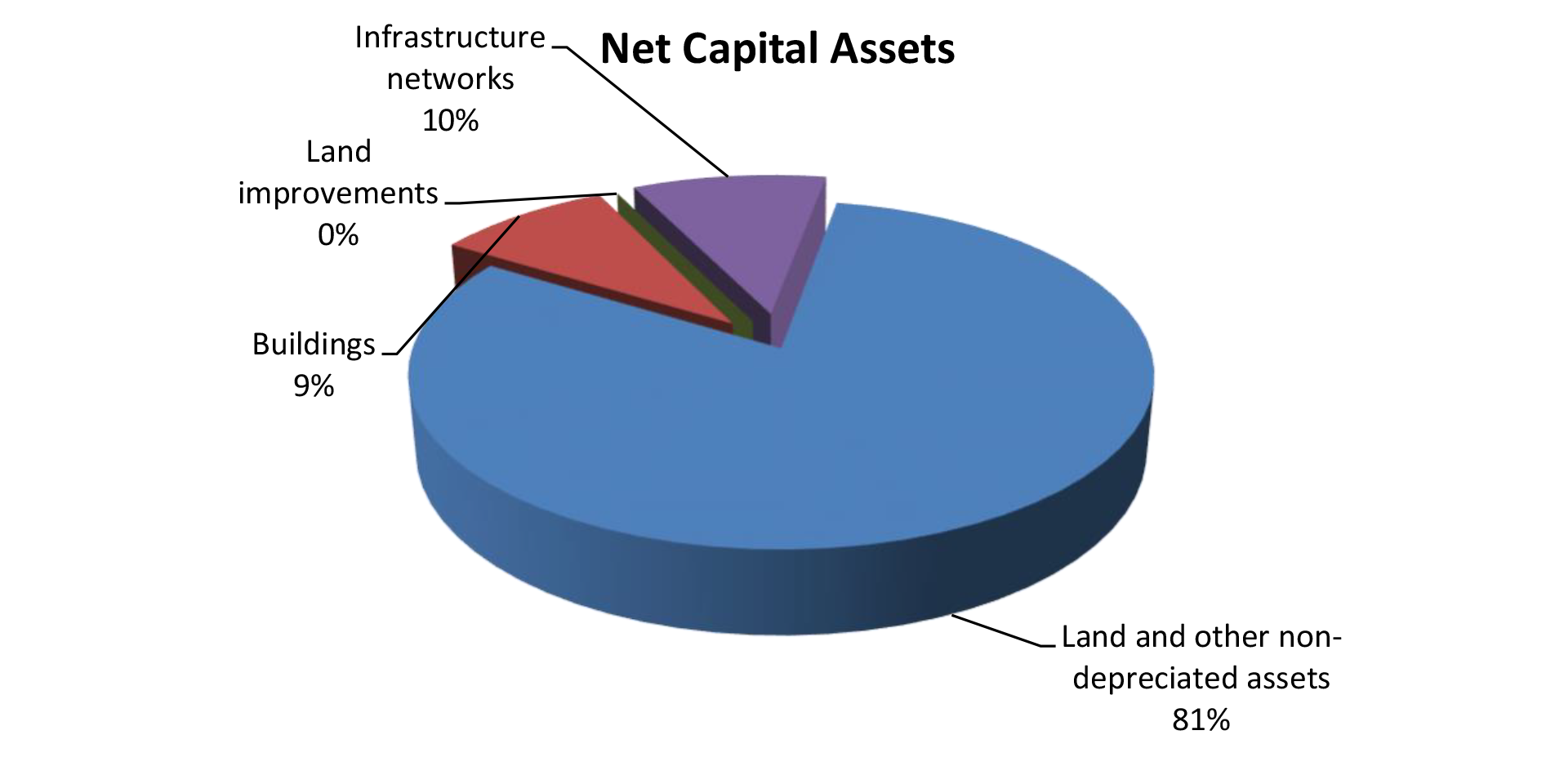

As of June 30, 2024, total assets and deferred outflows of resources exceeded total liabilities and deferred inflows of resources by $1.48 billion. Total assets and deferred outflows of resources of $1.73 billion included (1) cash of $599 million, (2) receivables of $97 million, (3) loans receivable of $773 million, (4) accrued interest and loan fees of $3 million, (5) deferred outflows of resources of $2 million, and (6) net capital assets of $257.5 million. Total liabilities and deferred inflows of resources totaled $251 million. DOH’s net position of $1.48 billion is comprised of a restricted amount of $976 million, of which $904 million is for loans; an unrestricted amount of $247 million; and net investment in capital assets of $257.5 million.

Auditors’ Opinions DOH RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles. DOH received an unmodified opinion on its compliance for all major federal programs, except for Special Supplemental Nutrition Program for Women, Infants and Children; Substance Abuse and Mental Health Services Projects of Regional and National Significance; Opioid STR; Block Grants for Community Mental Health Services; and Block Grants for Prevention and Treatment of Substance Abuse, which received a qualified opinion in accordance with the Uniform Guidance.

Findings THERE WAS ONEMATERIAL WEAKNESS and one significant deficiency in internal control over financial reporting that was required to be reported under Government Auditing Standards.

A material weakness is a deficiency, or a combination of deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented or detected and corrected on a timely basis. The material weakness is described on page 101 of the report.

A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. The significant deficiency is described on pages 102-103 of the report.

There were six material weaknesses and one significant deficiency in internal control over compliance that were required to be reported in accordance with the Uniform Guidance. The material weaknesses are described on pages 106-118 of the report and the significant deficiency is described on pages 104-105 of the report.

A material weakness in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance, such that there is reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented or detected and corrected on a timely basis.

A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance.

About the DepartmentThe mission of the Department of Health (DOH) is to protect and improve the health and environment for all people in Hawai‘i. DOH administers and oversees statewide personal health services, health promotion and disease prevention, mental health programs, monitoring of the environment, and the enforcement of environmental health laws. It administers federal grants to support the State’s health services and programs and is organized into four major administrations: Behavioral Health Services Administration, Health Resources Administration, Environmental Health Administration, and General Administration.

Financial Statements, Fiscal Year Ended June 30, 2024

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the Department of Education, as of and for the fiscal year ended June 30, 2024, and to comply with the requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by Accuity LLP.

Financial Highlights

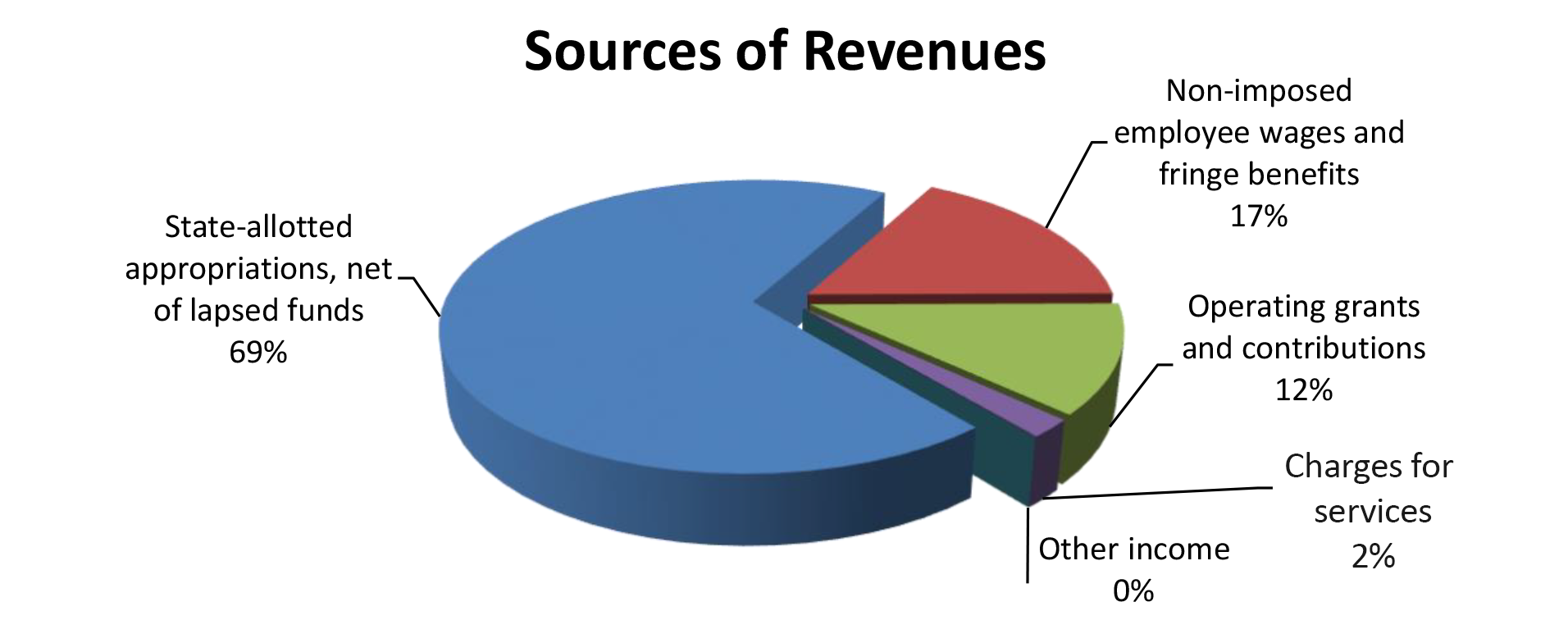

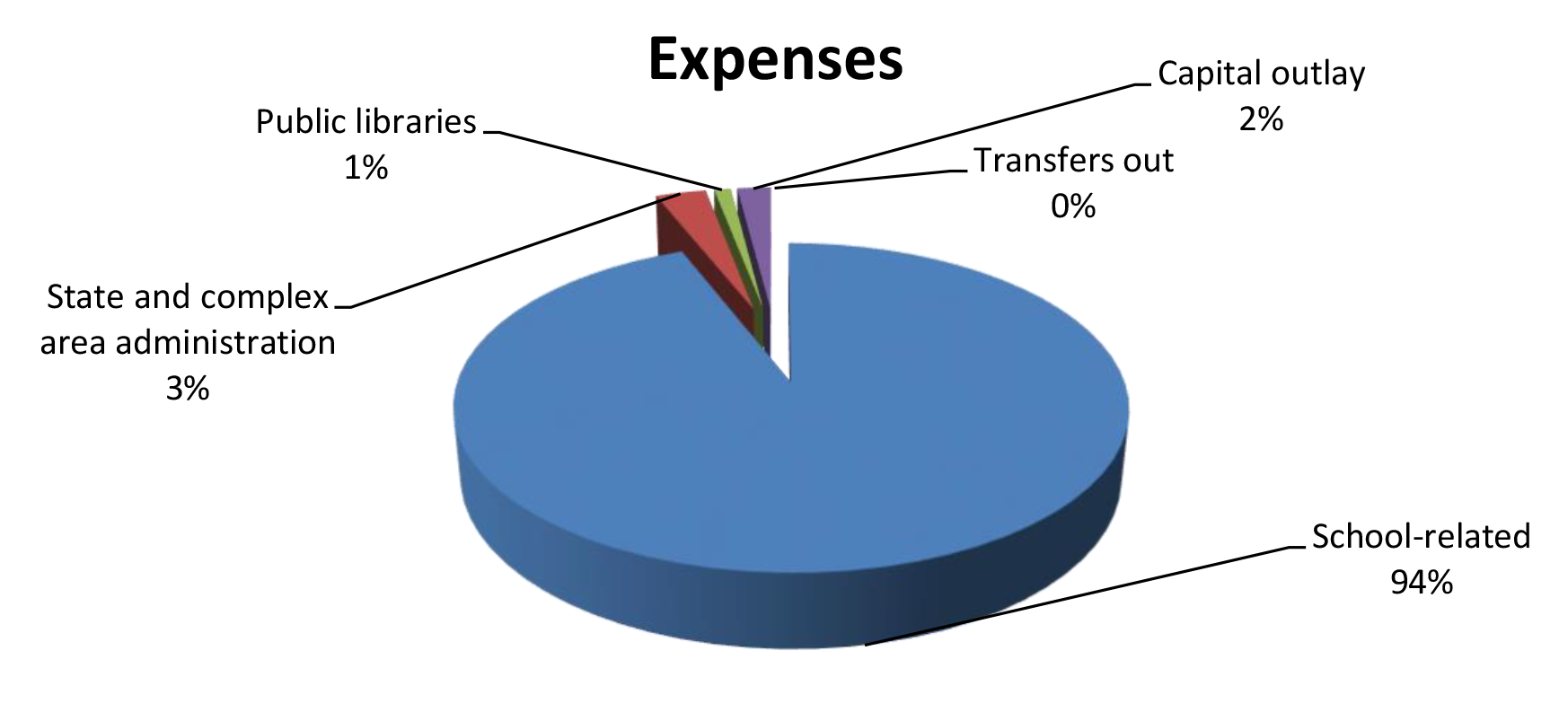

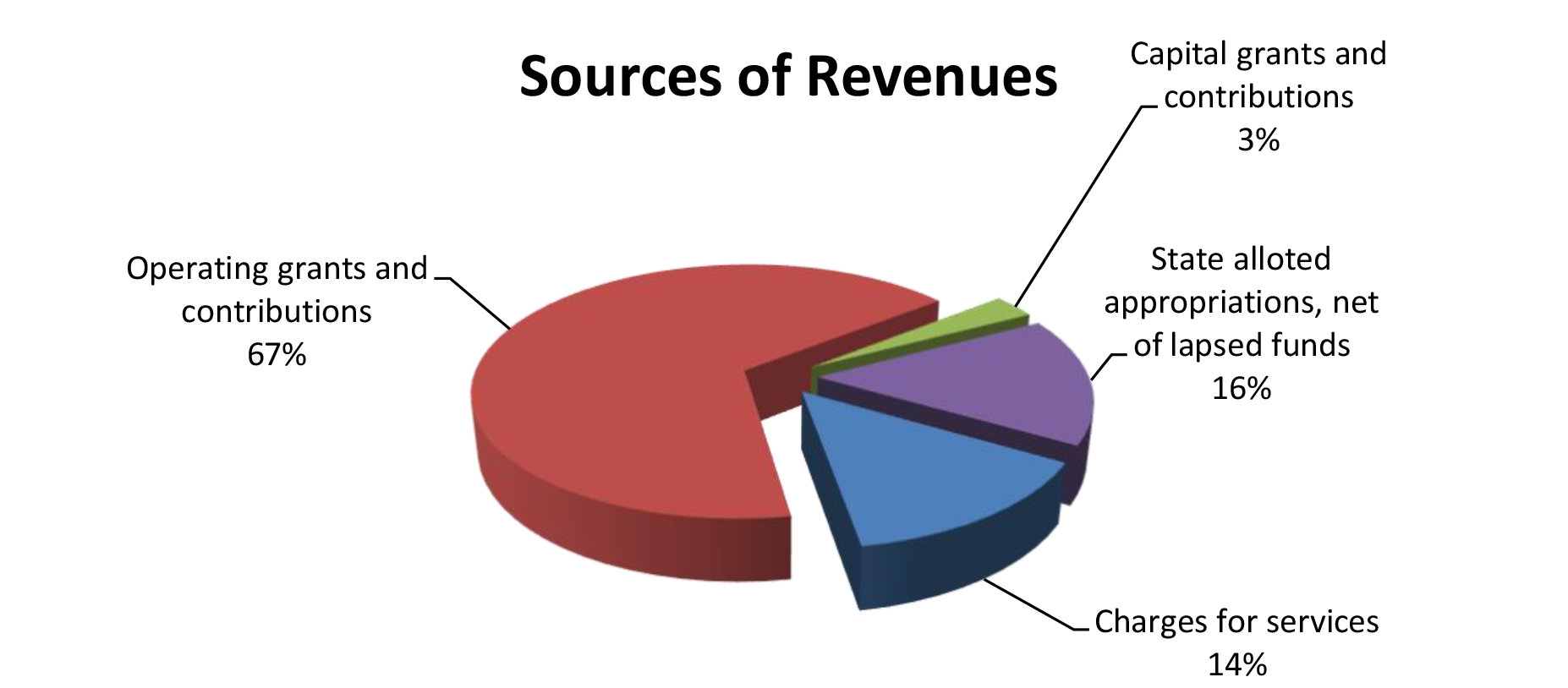

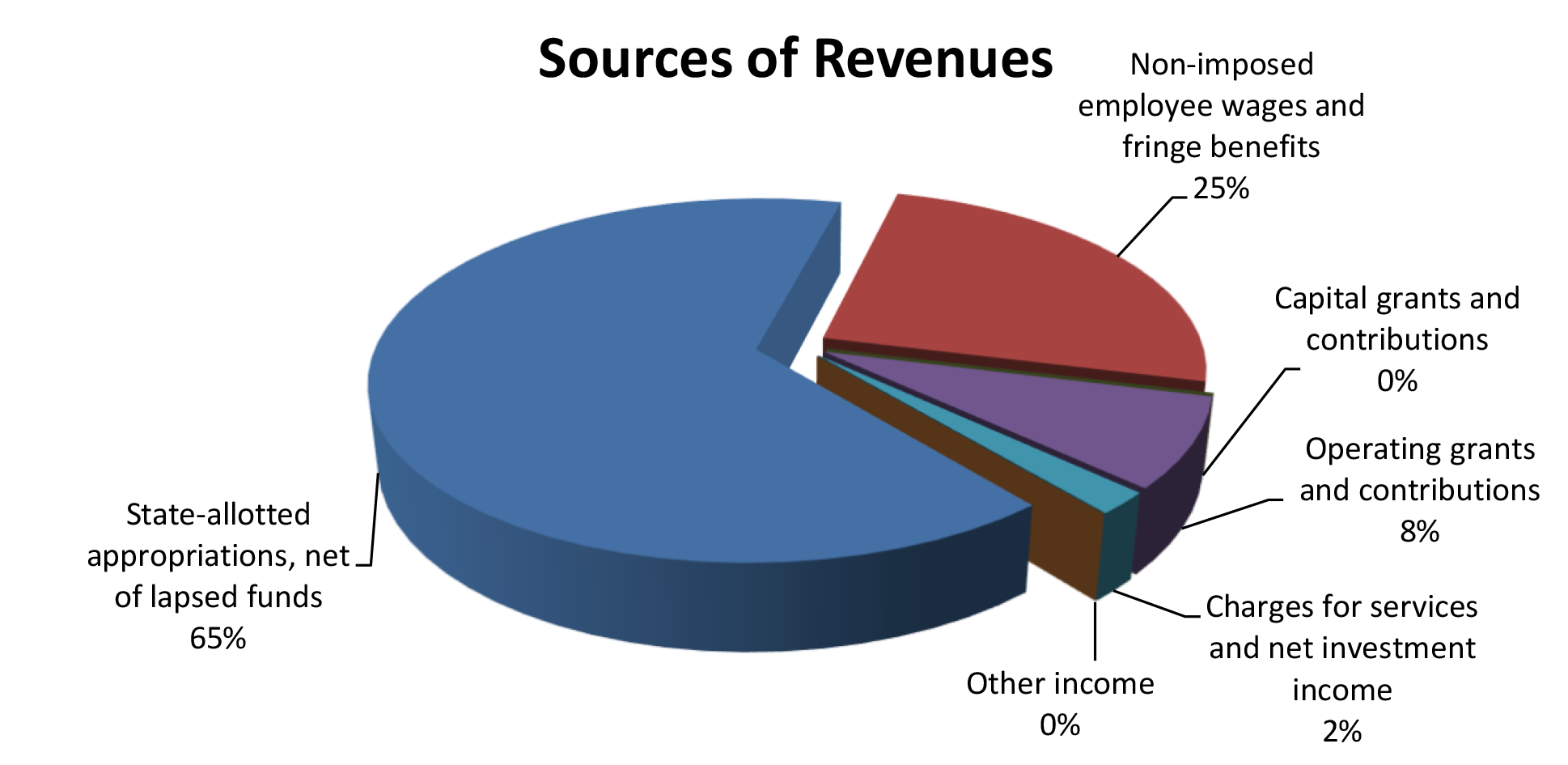

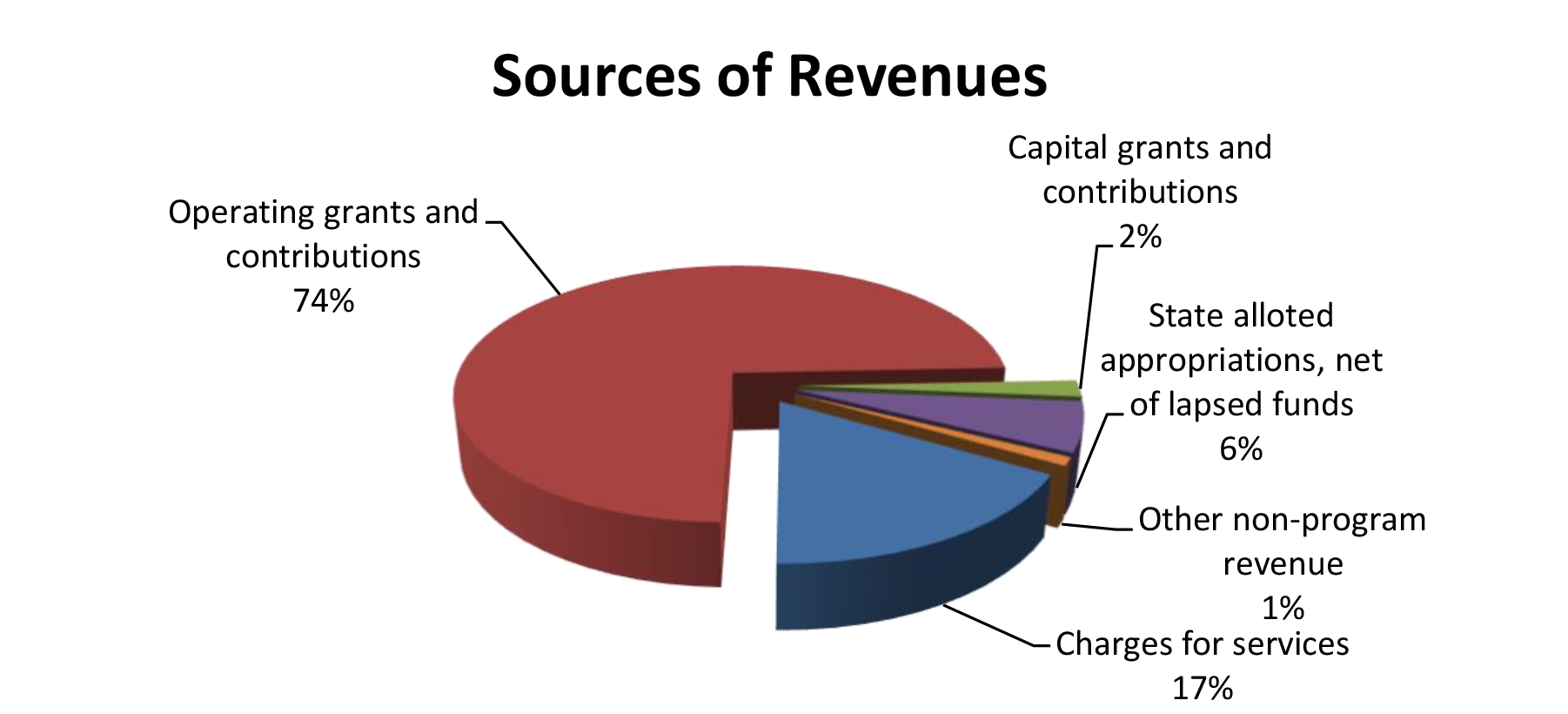

FOR THE FISCAL YEAR ended June 30, 2024, DOE reported total revenues of $4.13 billion and total expenses of $4.32 billion, resulting in a decrease in net position of $183.2 million.

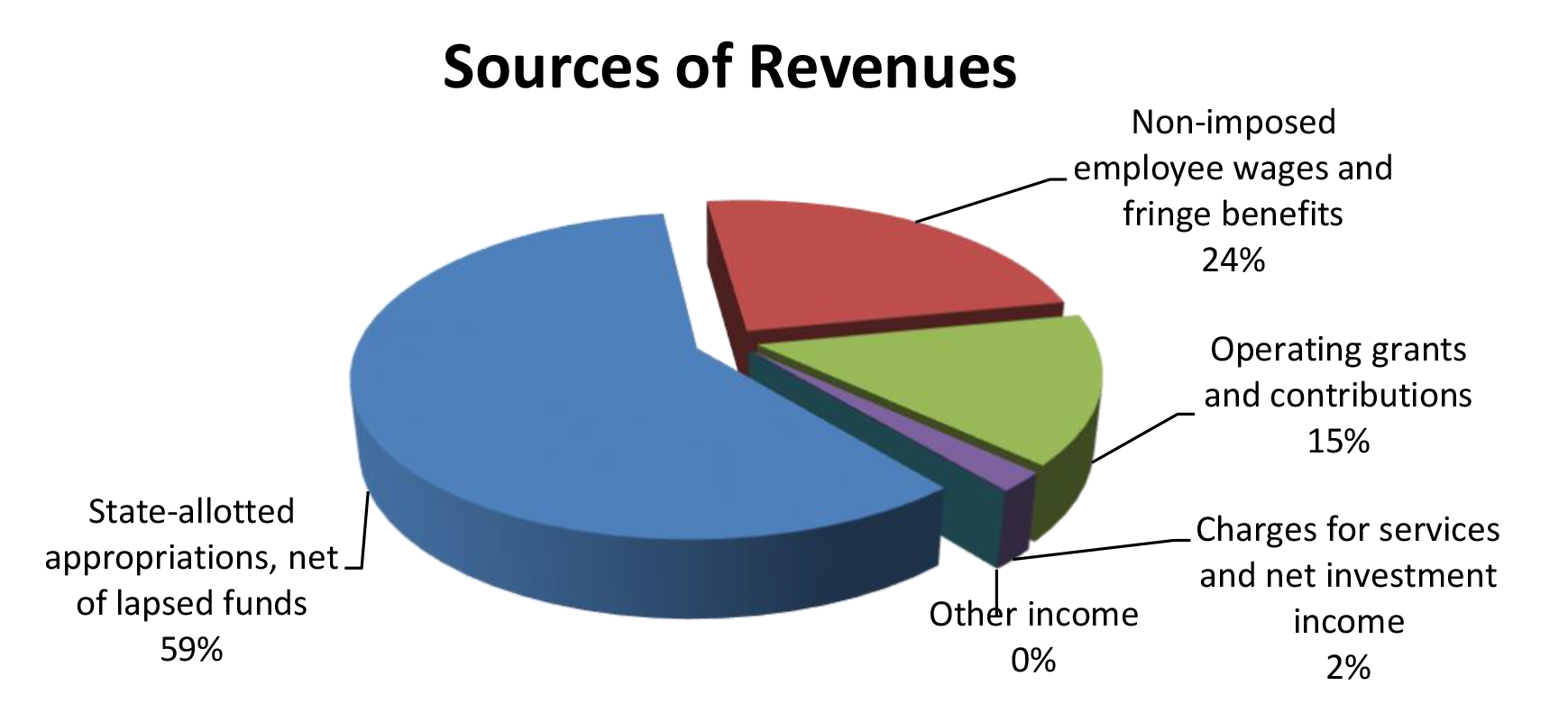

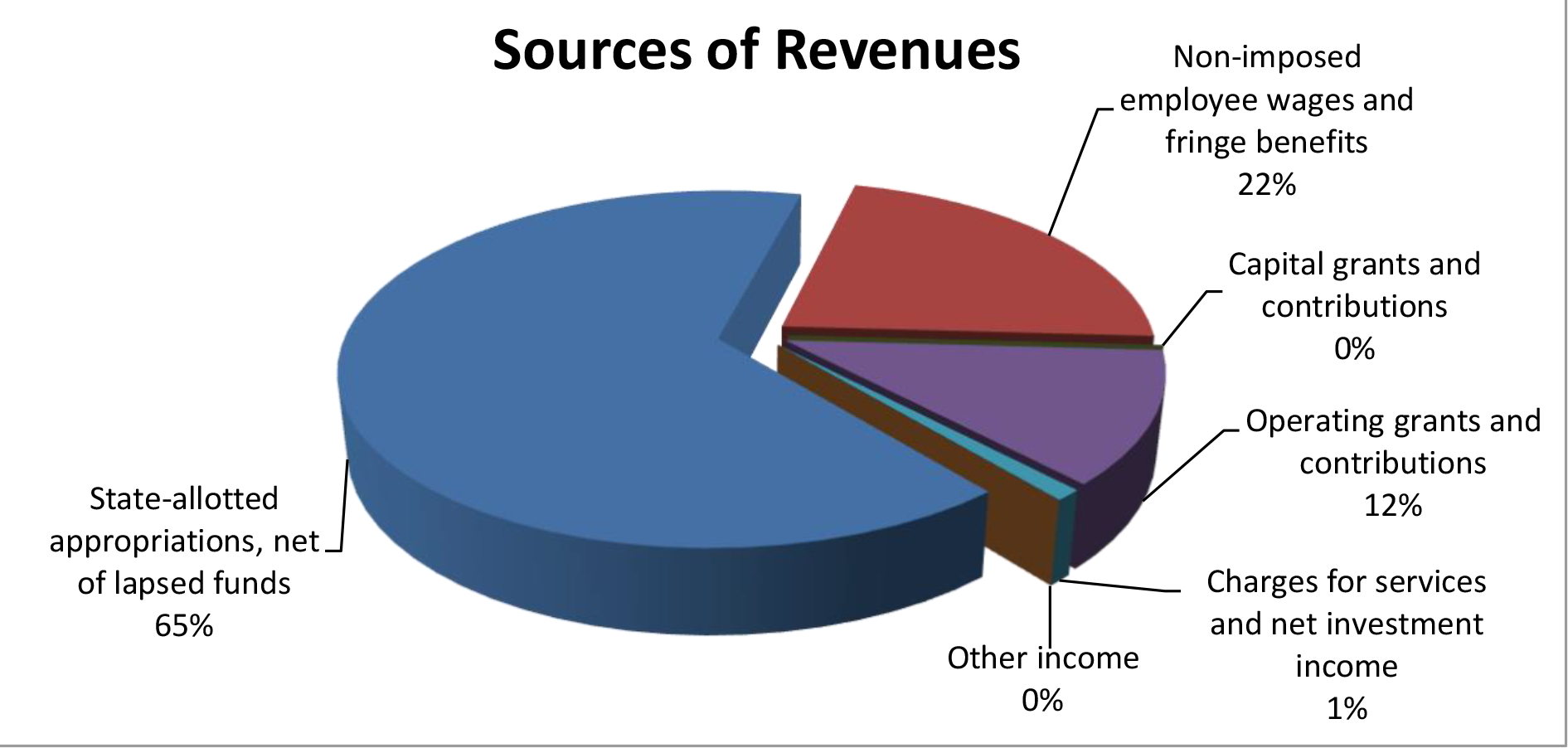

Total revenues of $4.13 billion consisted of (1) $2.46 billion in state-allotted appropriations, net of lapsed funds, (2) $973.8 million in non-imposed employee wages and fringe benefits, (3) $603.4 million in operating grants and contributions, (4) $94.4 million in charges for services, and (5) $4.2 million in other income.

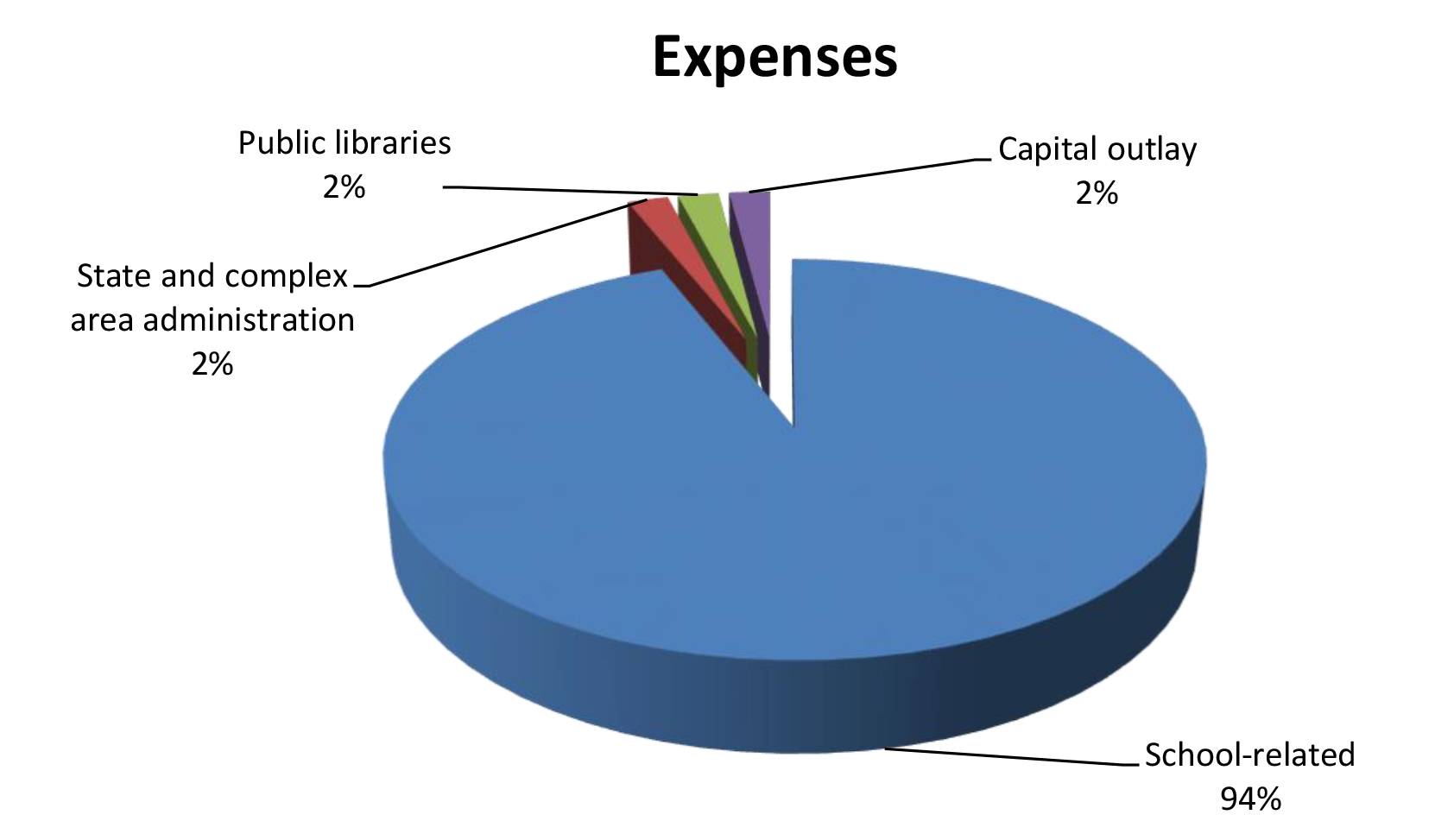

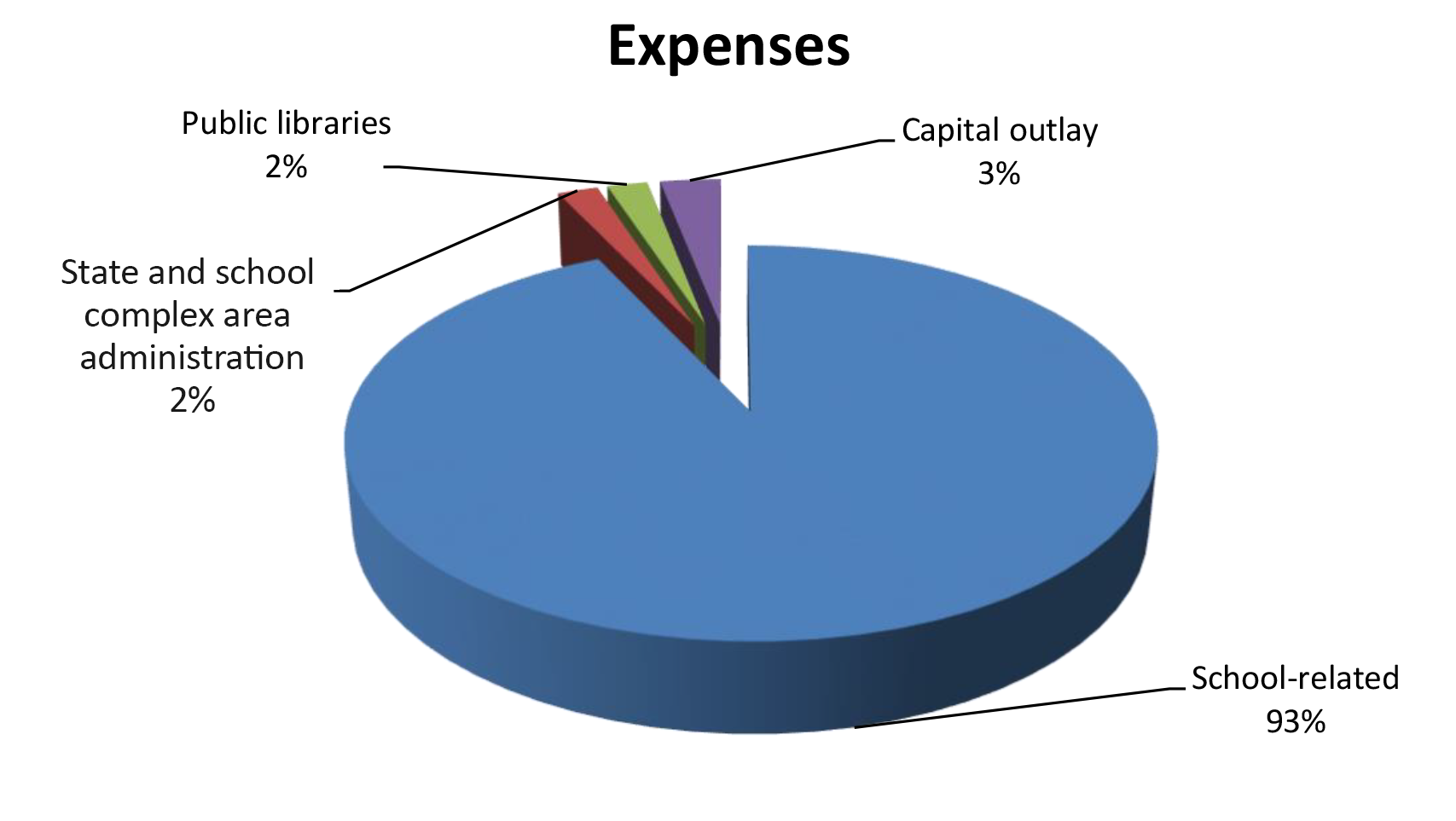

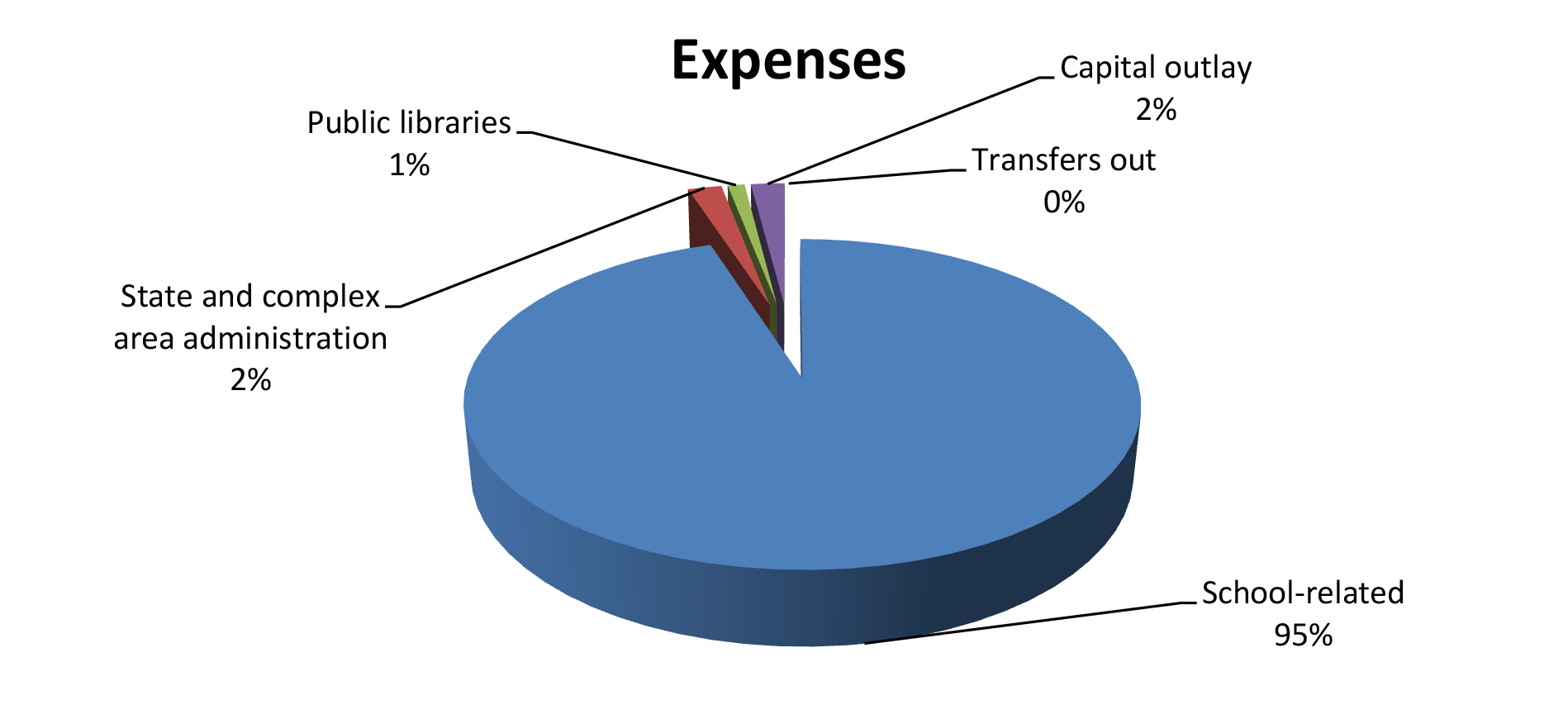

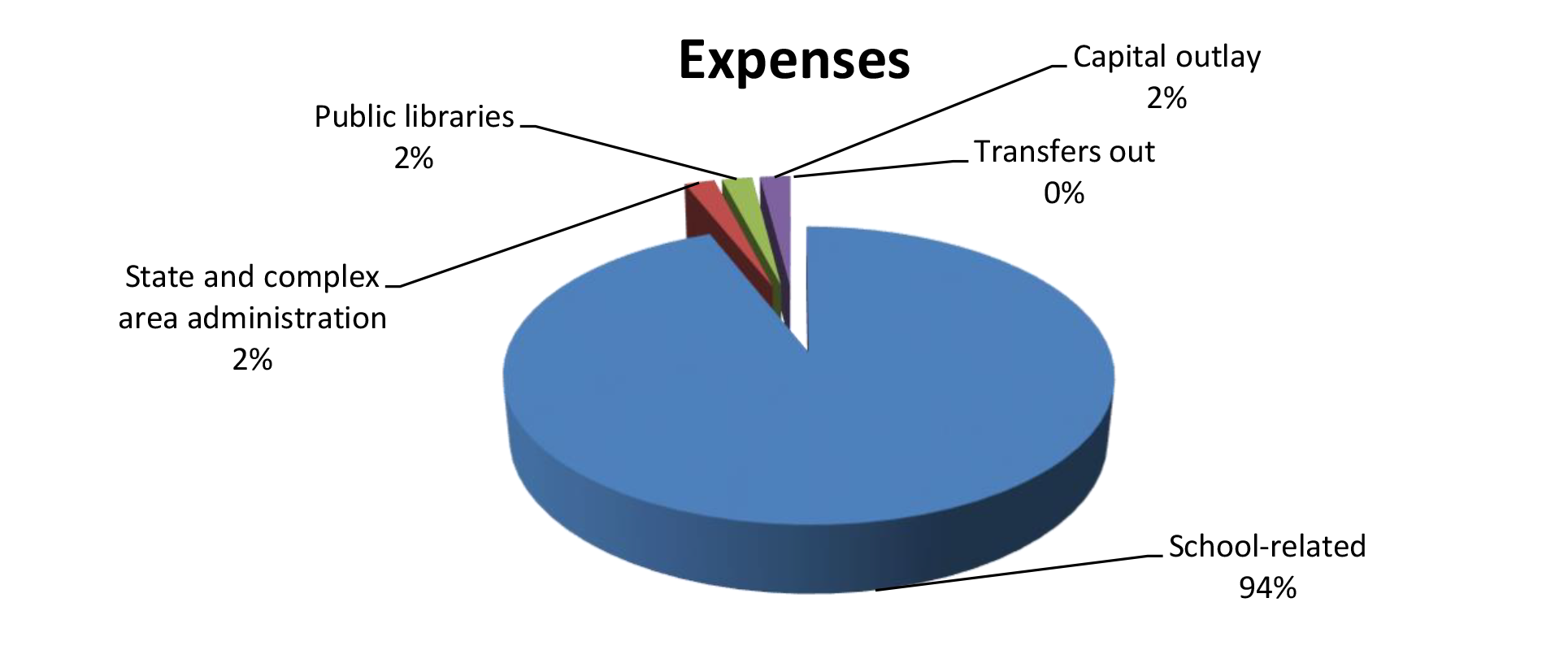

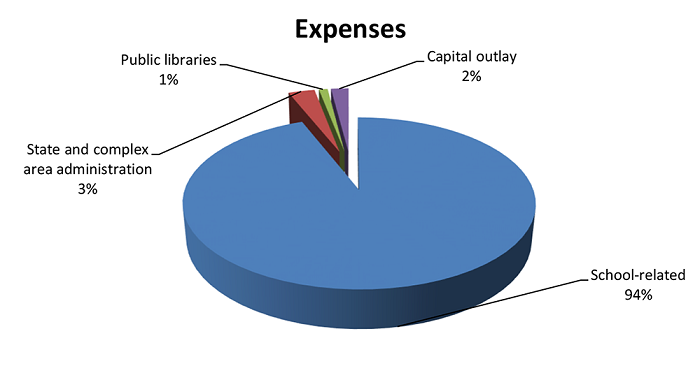

Total expenses of $4.32 billion consisted of (1) $4.06 billion for school-related costs, (2) $99.3 million for state and school complex area administration, (3) $63.2 million for public libraries, and (4) $96.5 million for capital outlay.

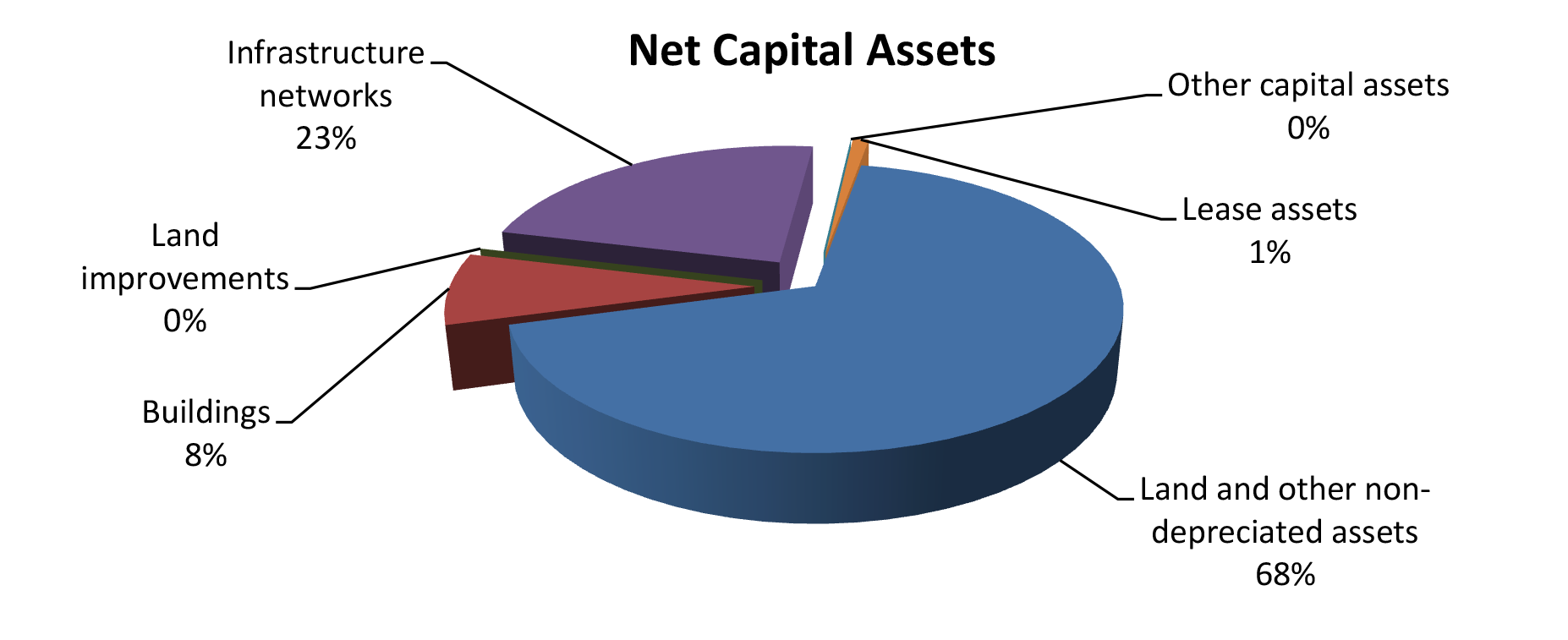

As of June 30, 2024, total assets exceeded total liabilities by $3.96 billion. Of this amount, $1.41 billion is unrestricted and may be used to meet ongoing expenses and obligations. Total assets of $4.83 billion were comprised of (1) cash of $2.07 billion, (2) receivables of $110.1 million, and (3) net capital assets of $2.64 billion. Total liabilities of $869.4 million were comprised of (1) vouchers and contracts payable of $236.4 million, (2) accrued wages and employee benefits of $312 million, (3) accrued compensated absences of $90.9 million, (4) workers’ compensation claims reserve of $151.6 million, (5) amount due to the state general fund of $5 million, (6) notes payable of $29.9 million, (7) lease liability of $30.8 million, (8) subscription liability of $12.5 million, and (9) other liabilities of $300,000.

Auditors’ Opinion DOE RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles. DOE also received an unmodified opinion on its compliance with major federal programs in accordance with the Uniform Guidance.

Findings THERE WERE NOREPORTED DEFICIENCIES in internal controls over financial reporting that were considered to be material weaknesses and no instance of noncompliance or other matters that were required to be reported under Government Auditing Standards. There were no findings that were considered material weaknesses in internal control over compliance in accordance with the Uniform Guidance.

About the Department

The Department of Education (DOE) administers the statewide system of public schools and public libraries. DOE is also responsible for administering state laws regarding regulation of private school operations through a program of inspection and licensing and the professional certification of all teachers for every academic and noncollege type of school. DOE’s financial statements are comprised of the assets and liabilities and financial activities of DOE, the Hawai‘i State Public Library System (Public Library System), and the Hawai‘i State Public Charter Schools (Public Charter Schools). The fiscal and oversight authority for DOE, Public Library System, and Public Charter Schools are managed independently. DOE relies on certain Public Charter Schools financial information which has been audited by other auditors and coordinated by Public Charter Schools. Federal grants received to support public school and public library systems are administered by DOE on a statewide basis; the federal expenditures of Public Charter Schools are separately audited and excluded from the Schedule of Expenditures of Federal Awards.

Financial Statements, Fiscal Year Ended June 30, 2024

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the Department of Human Services, as of and for the fiscal year ended June 30, 2024, and to comply with Title 2, U.S. Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by Accuity LLP.

Financial Highlights

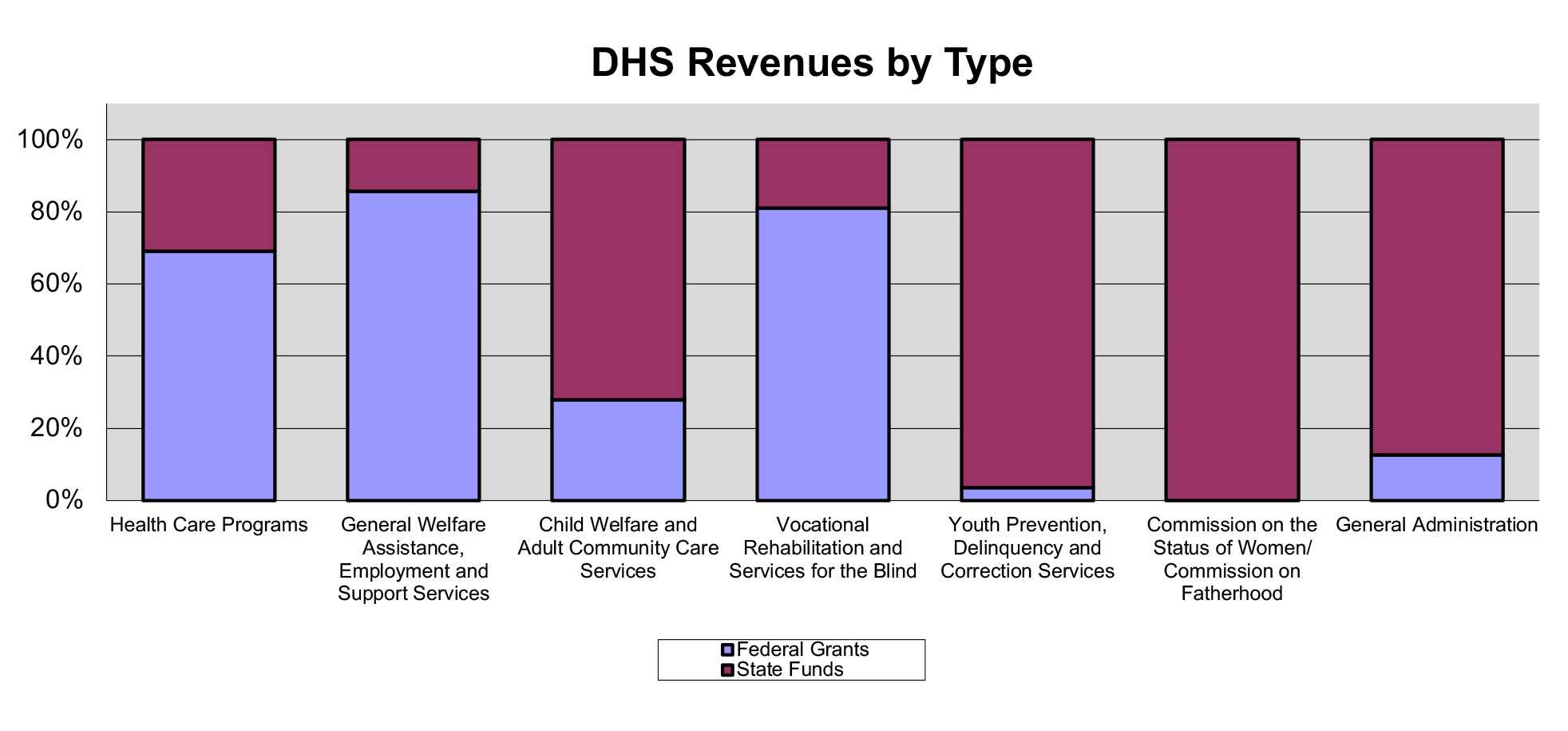

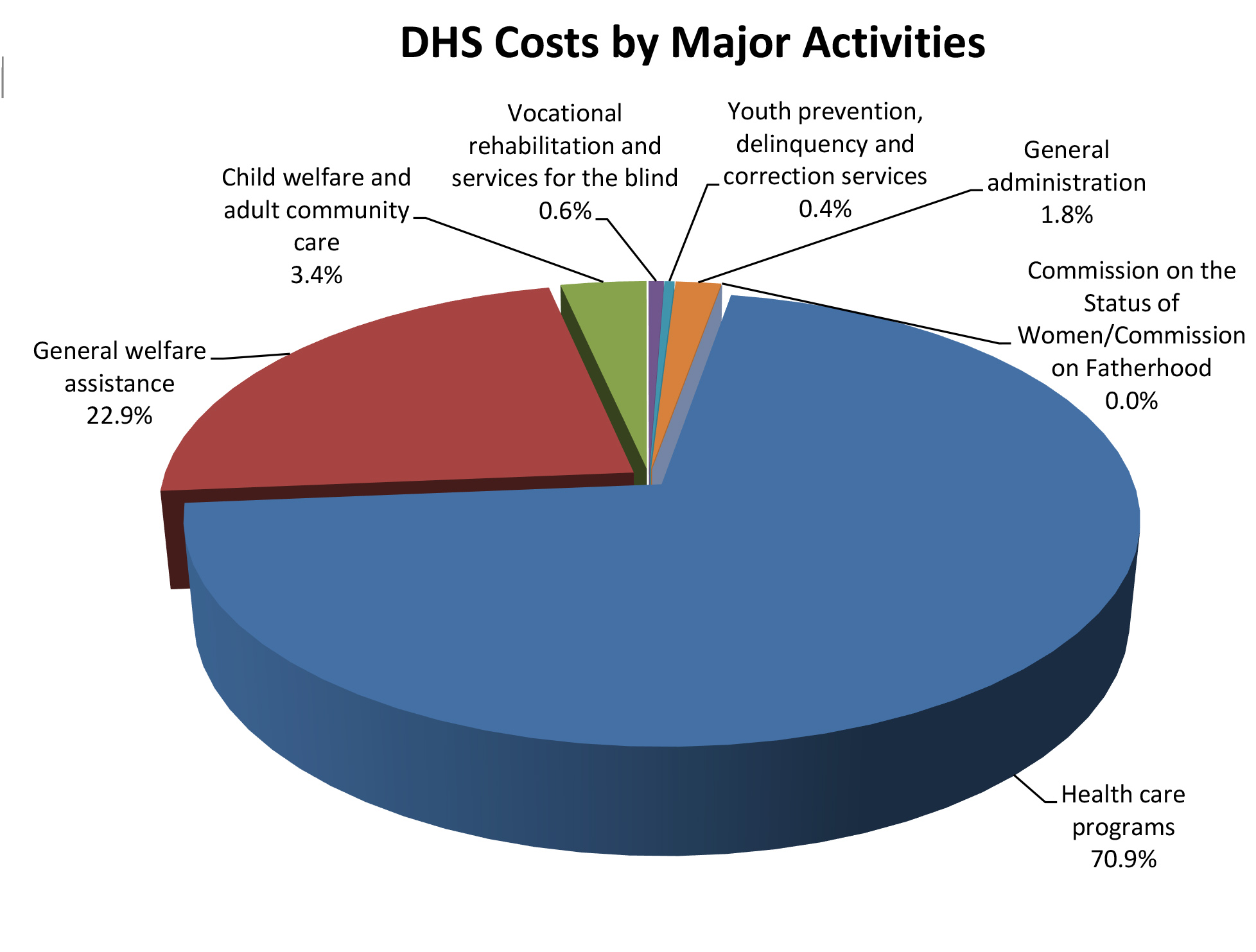

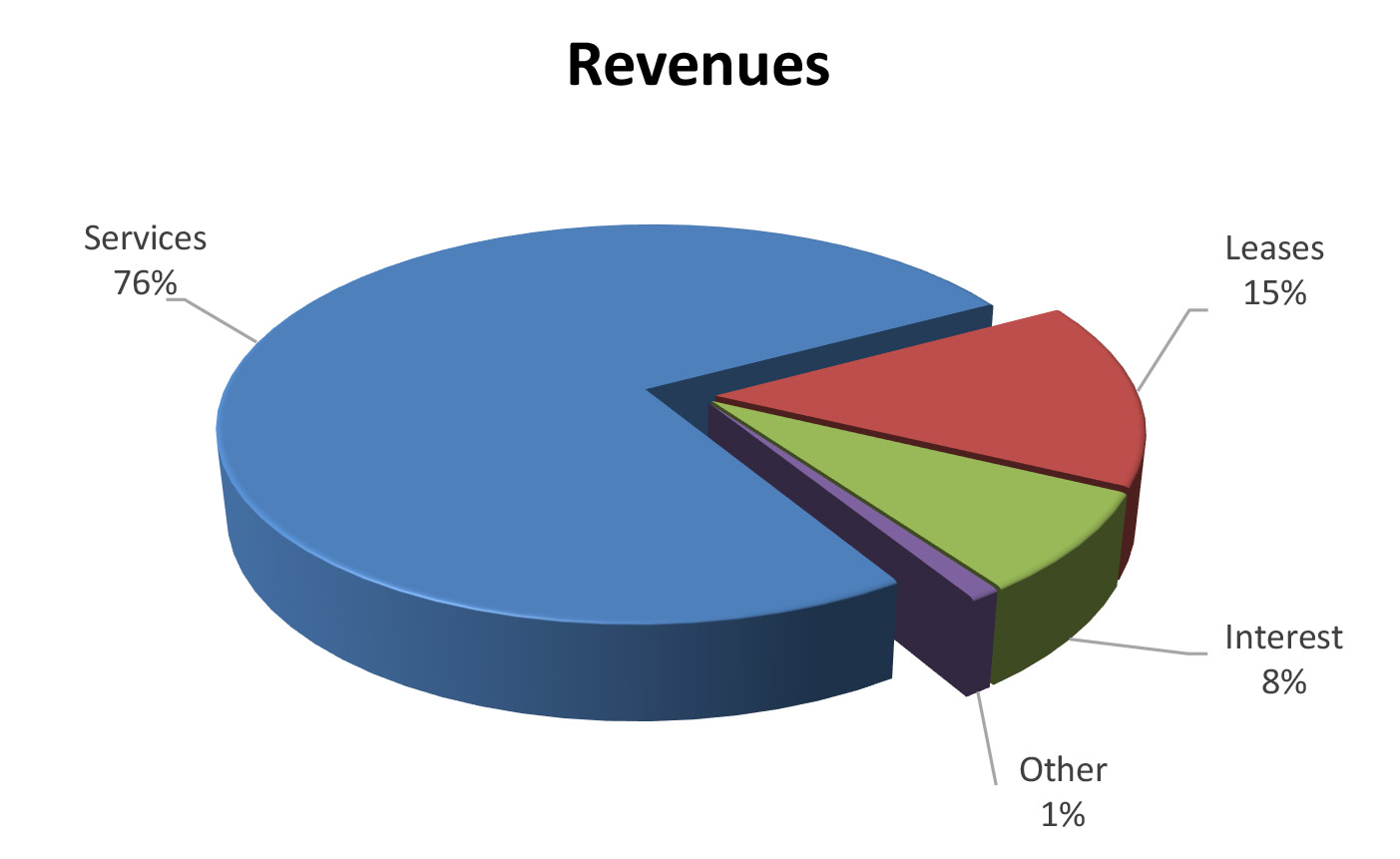

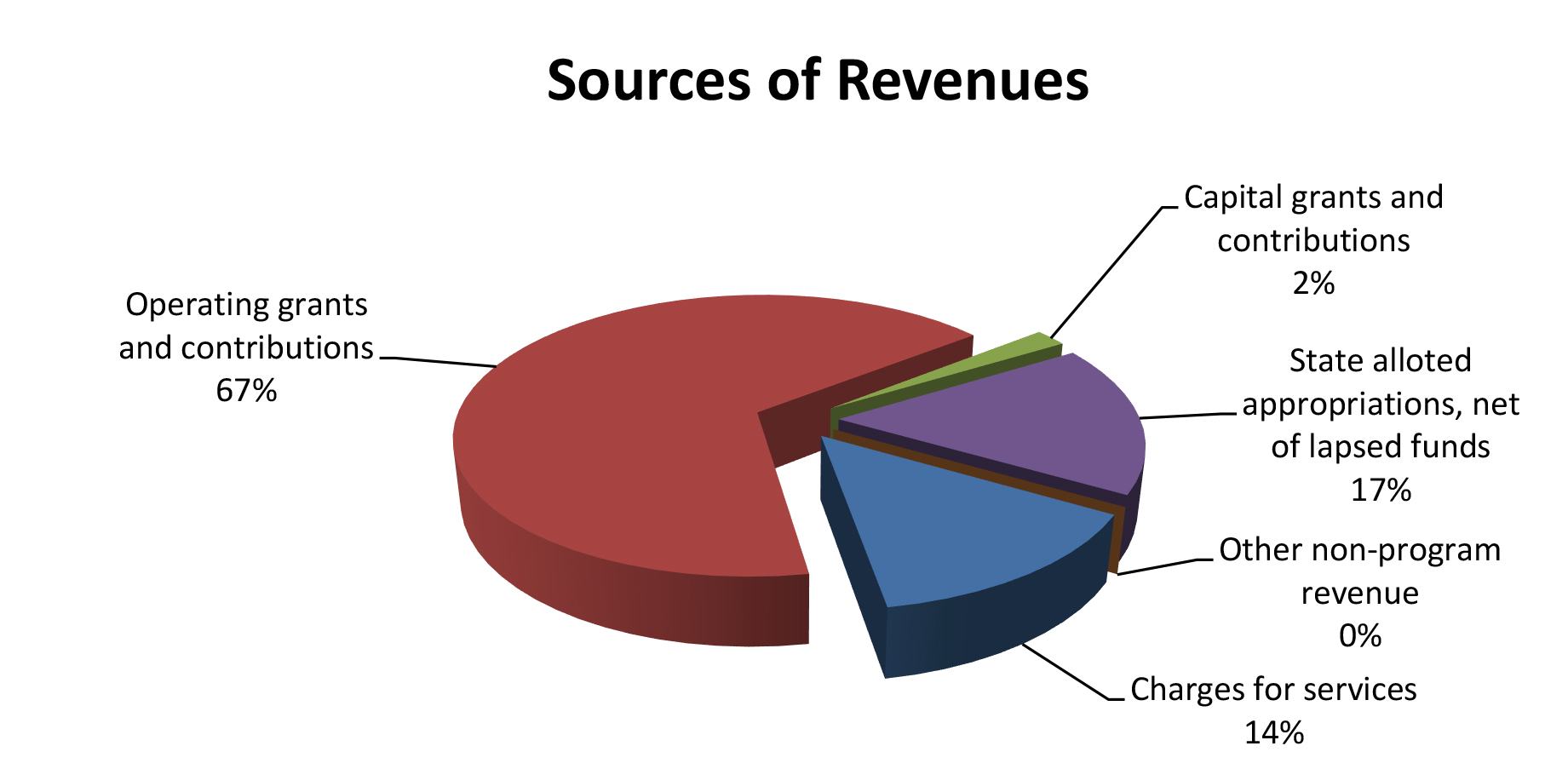

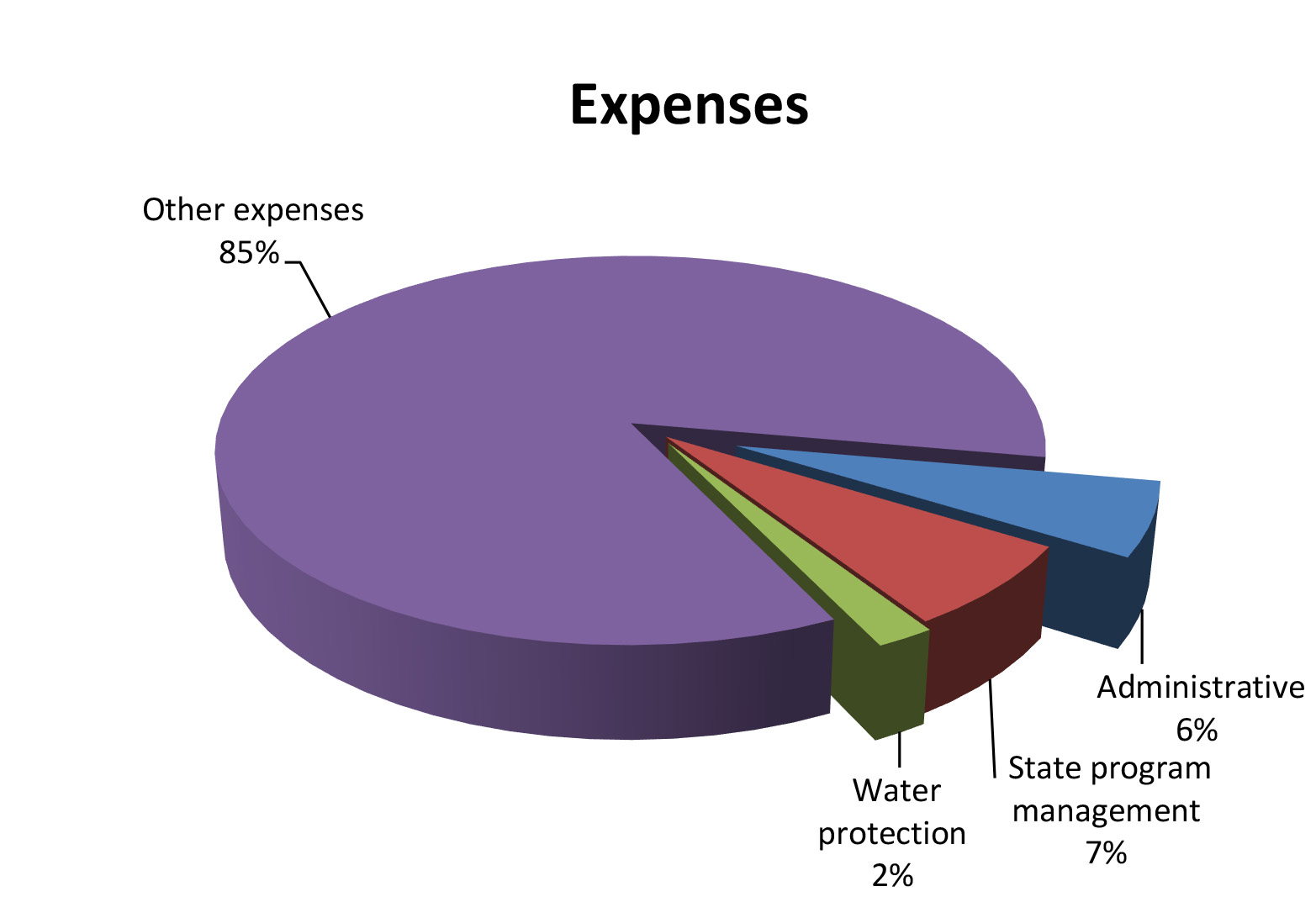

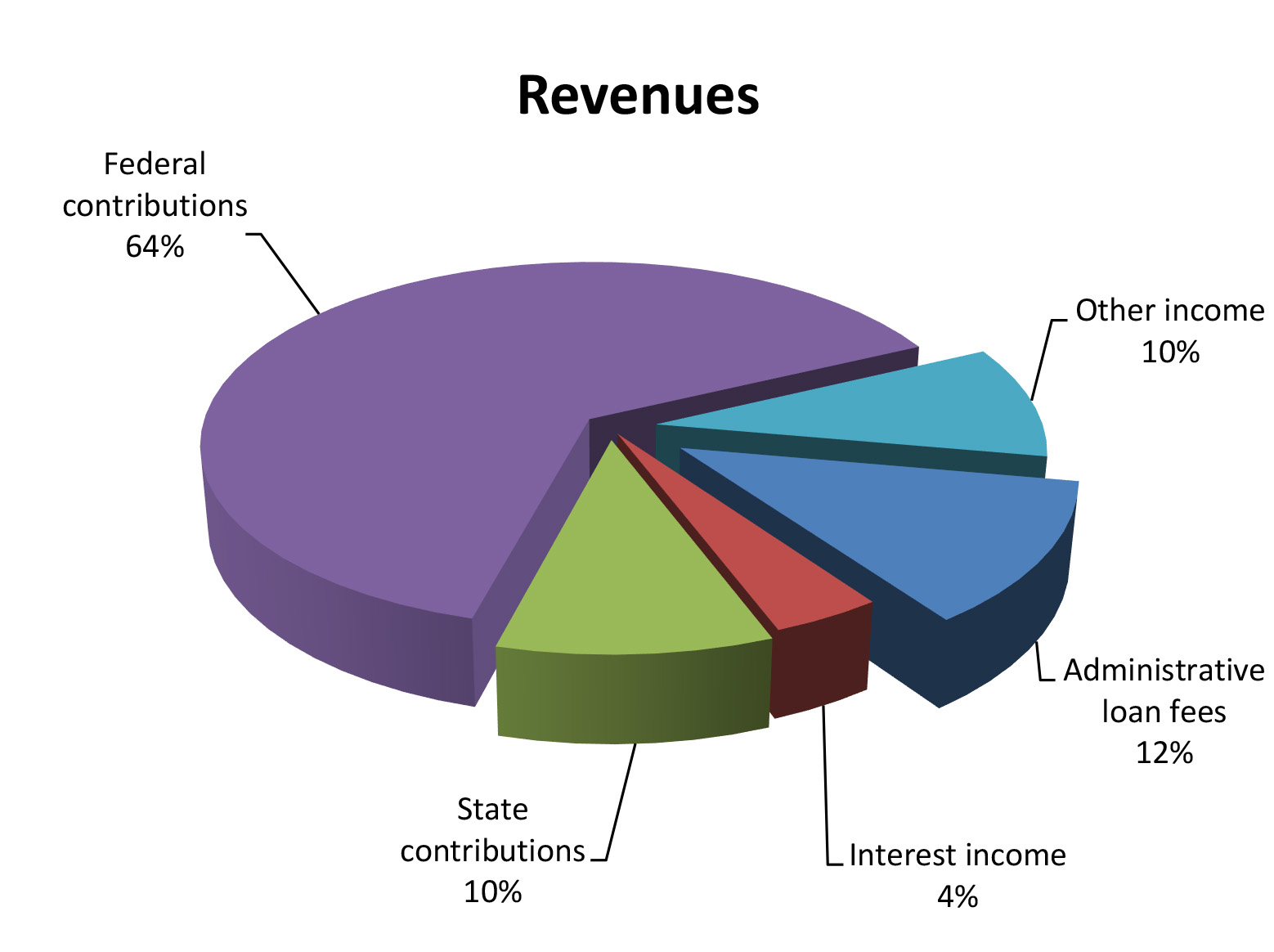

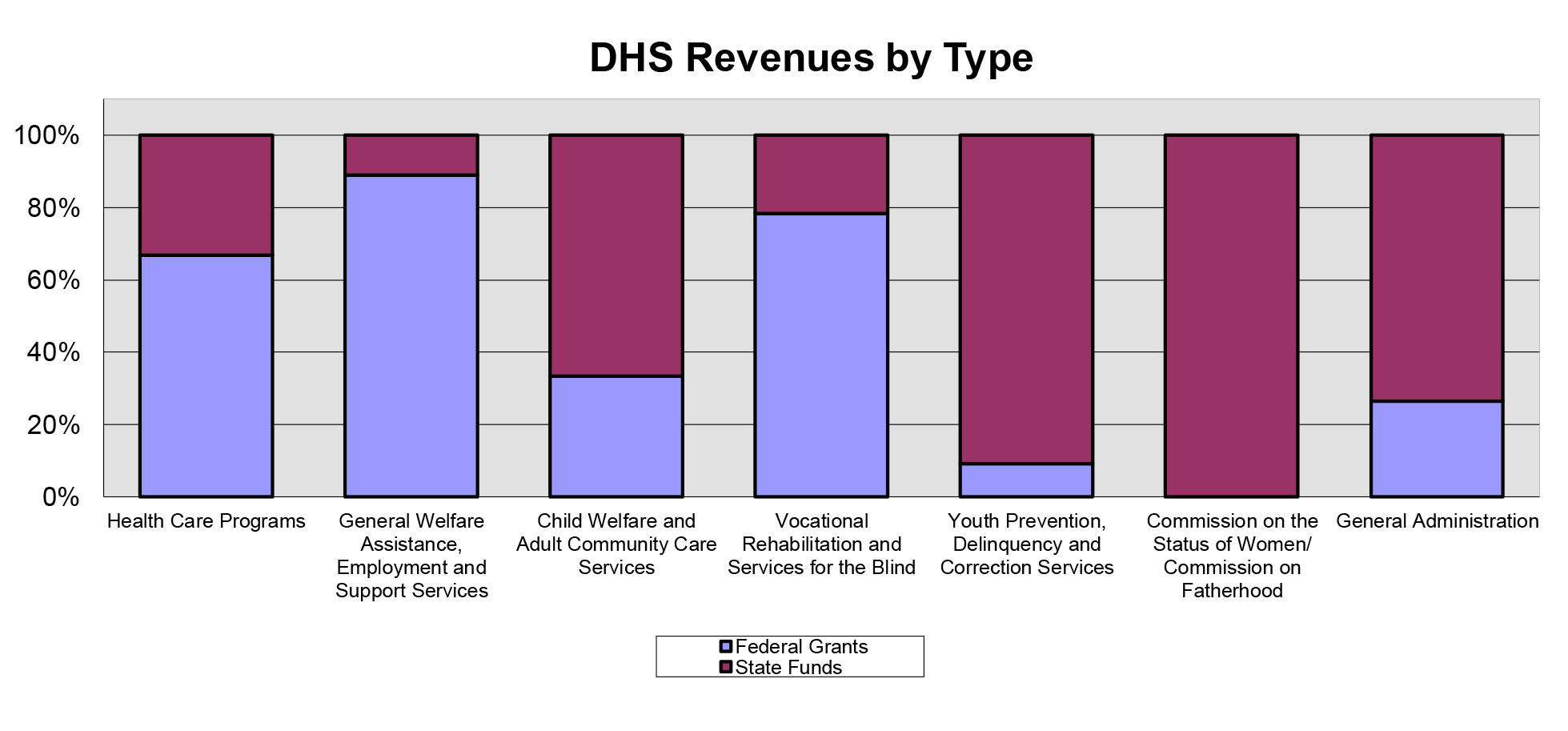

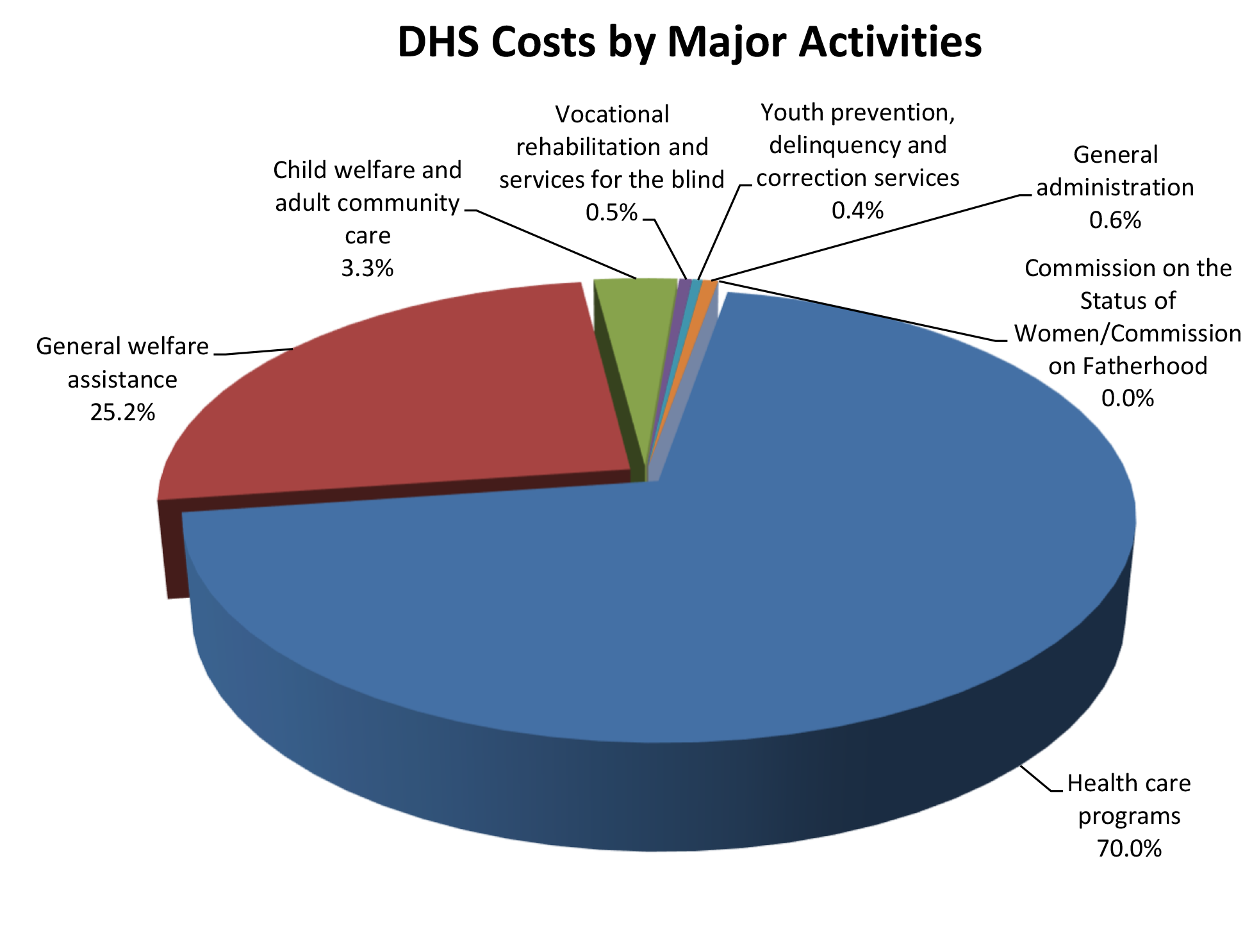

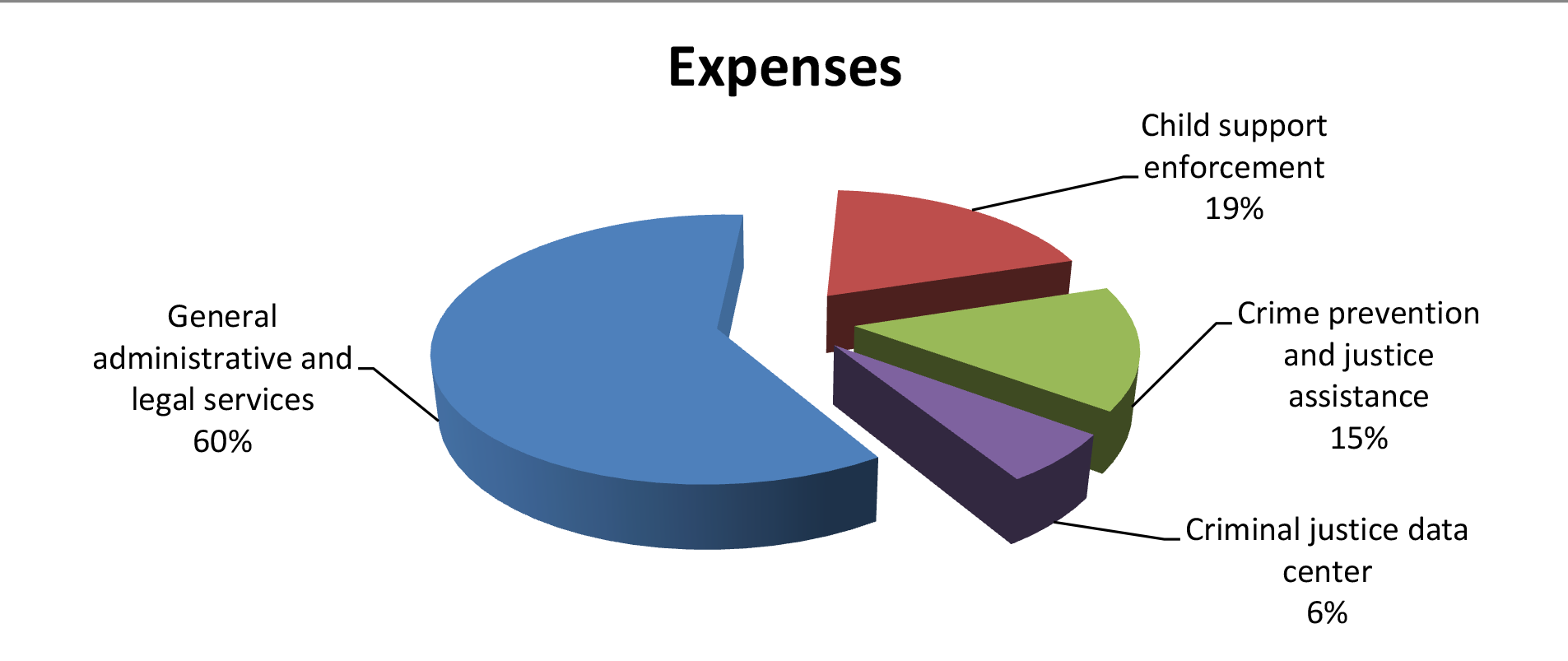

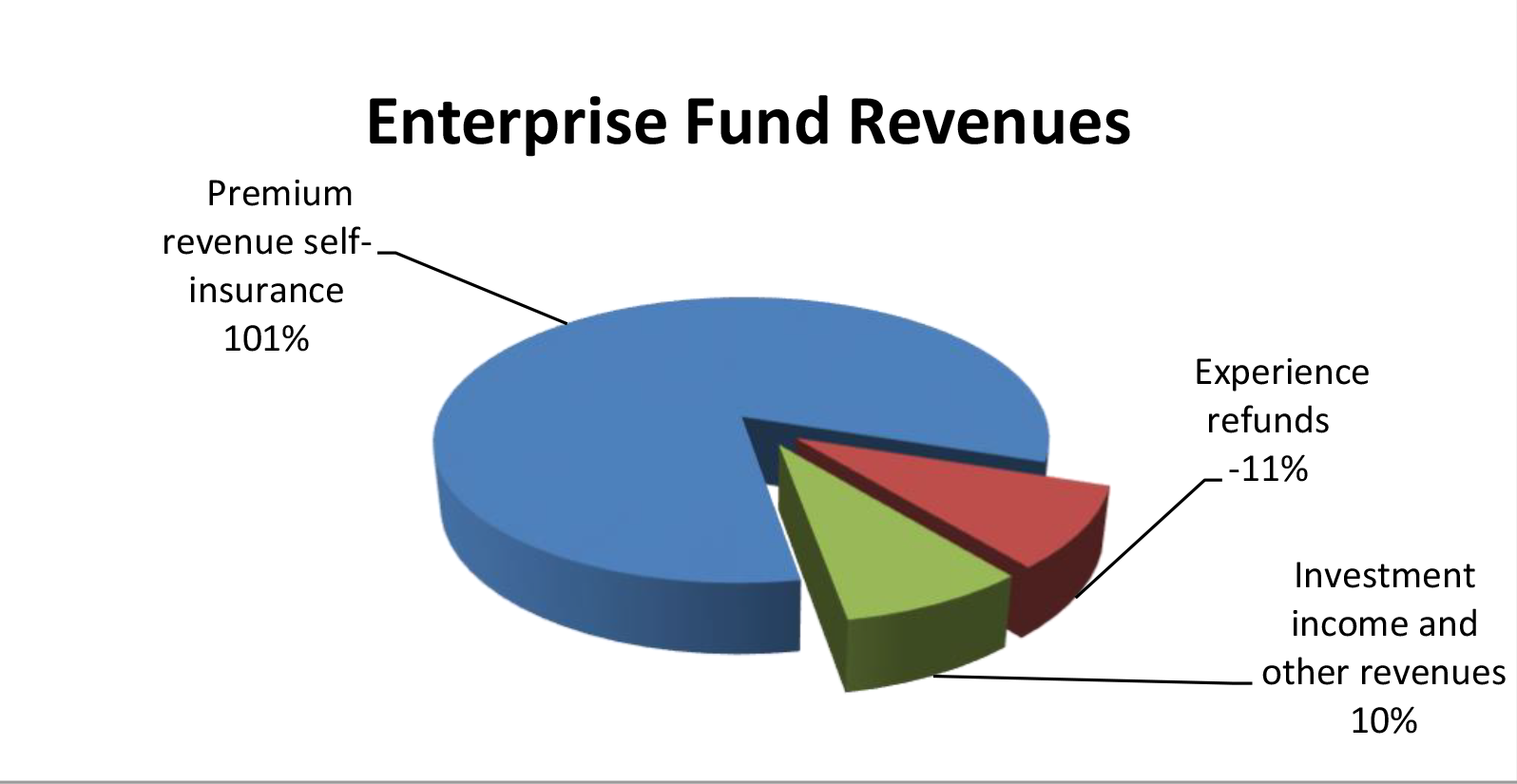

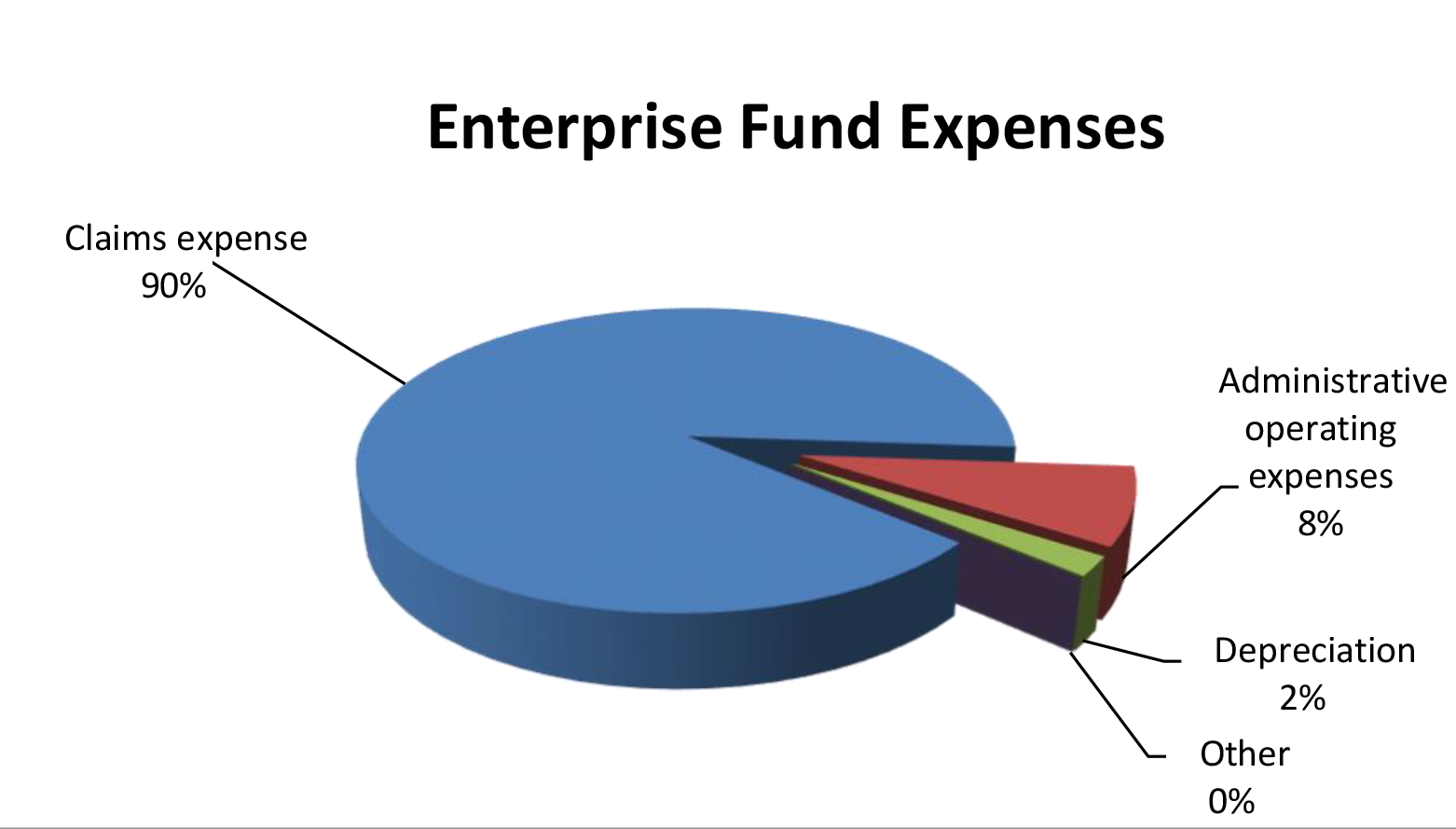

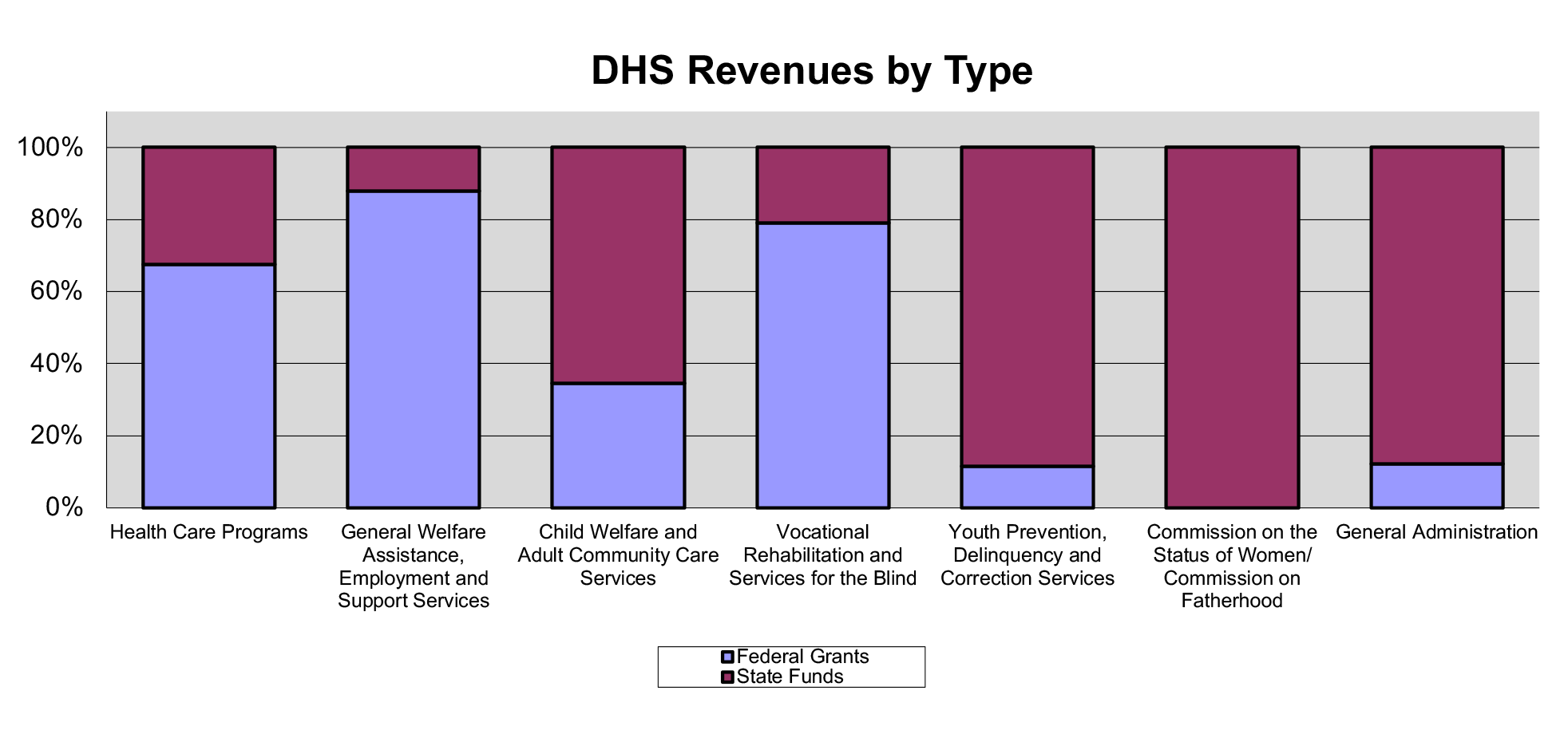

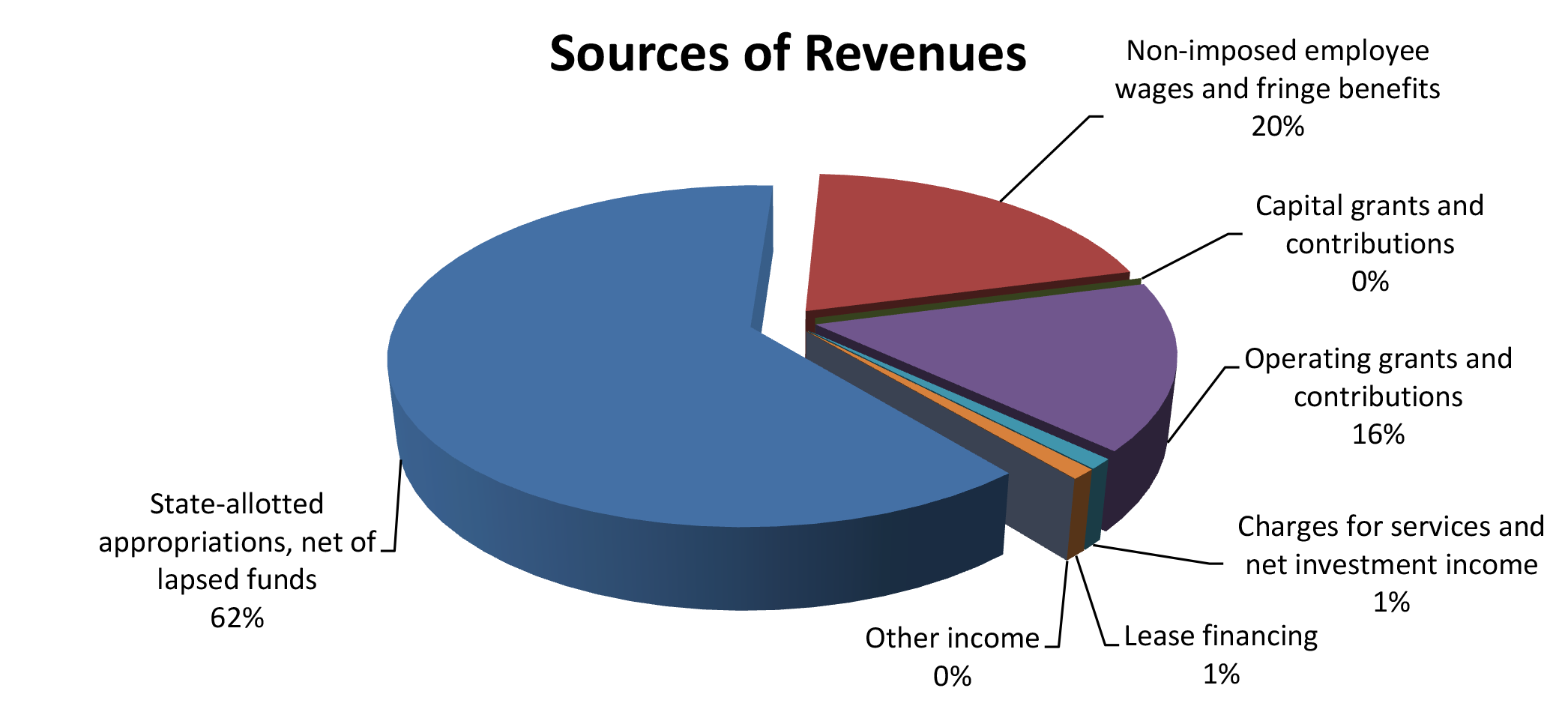

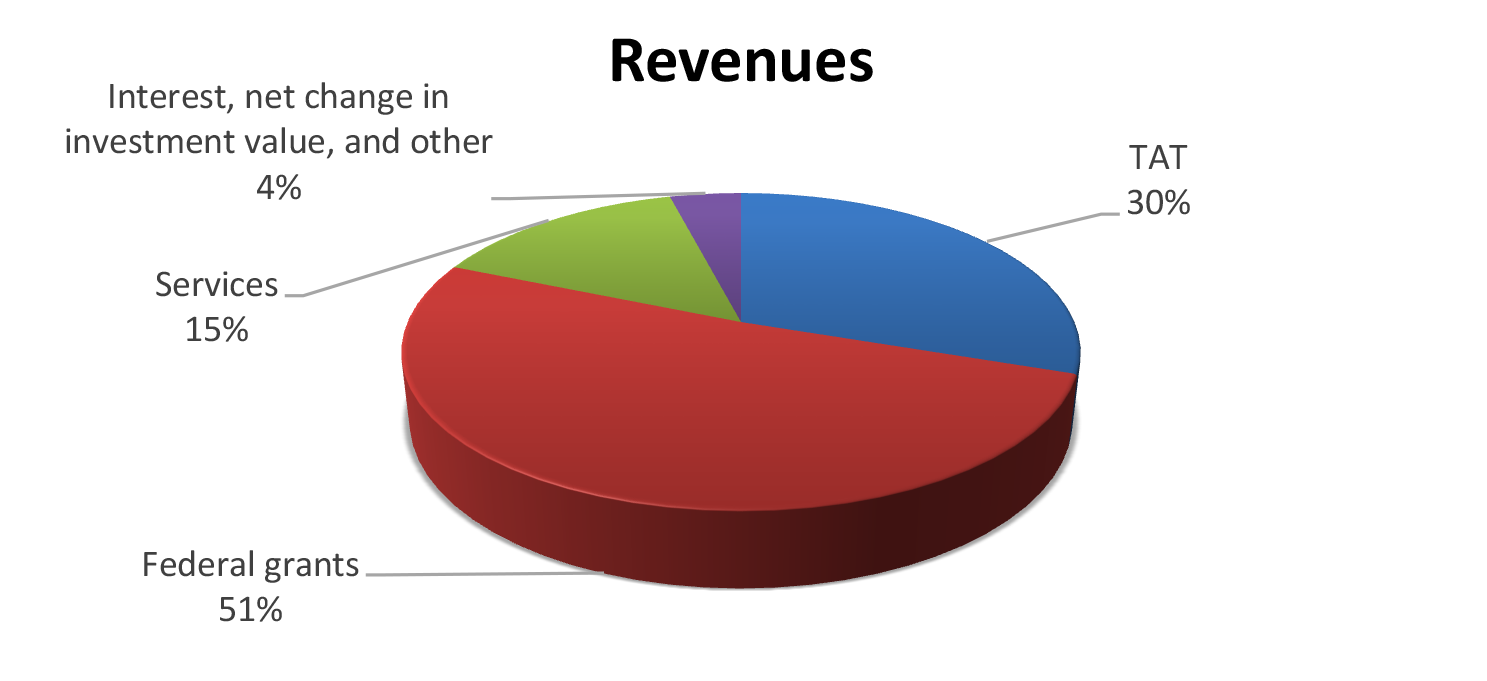

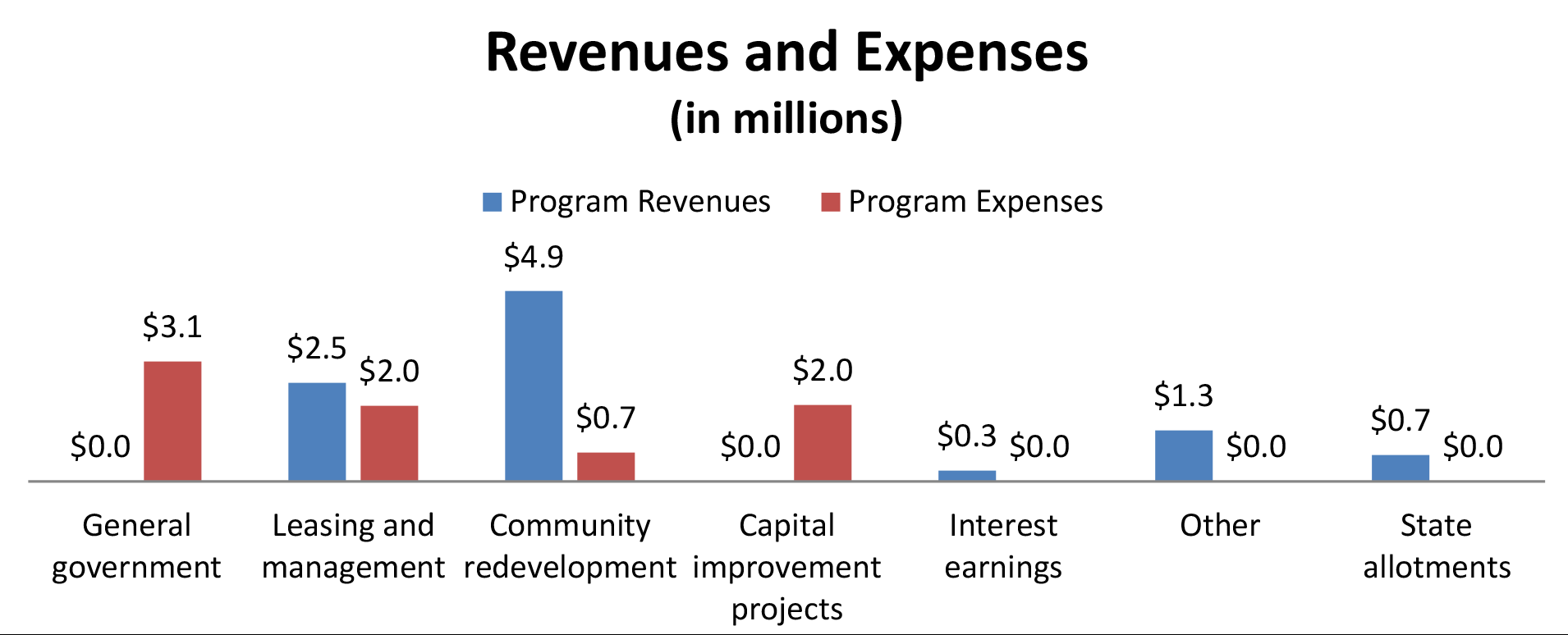

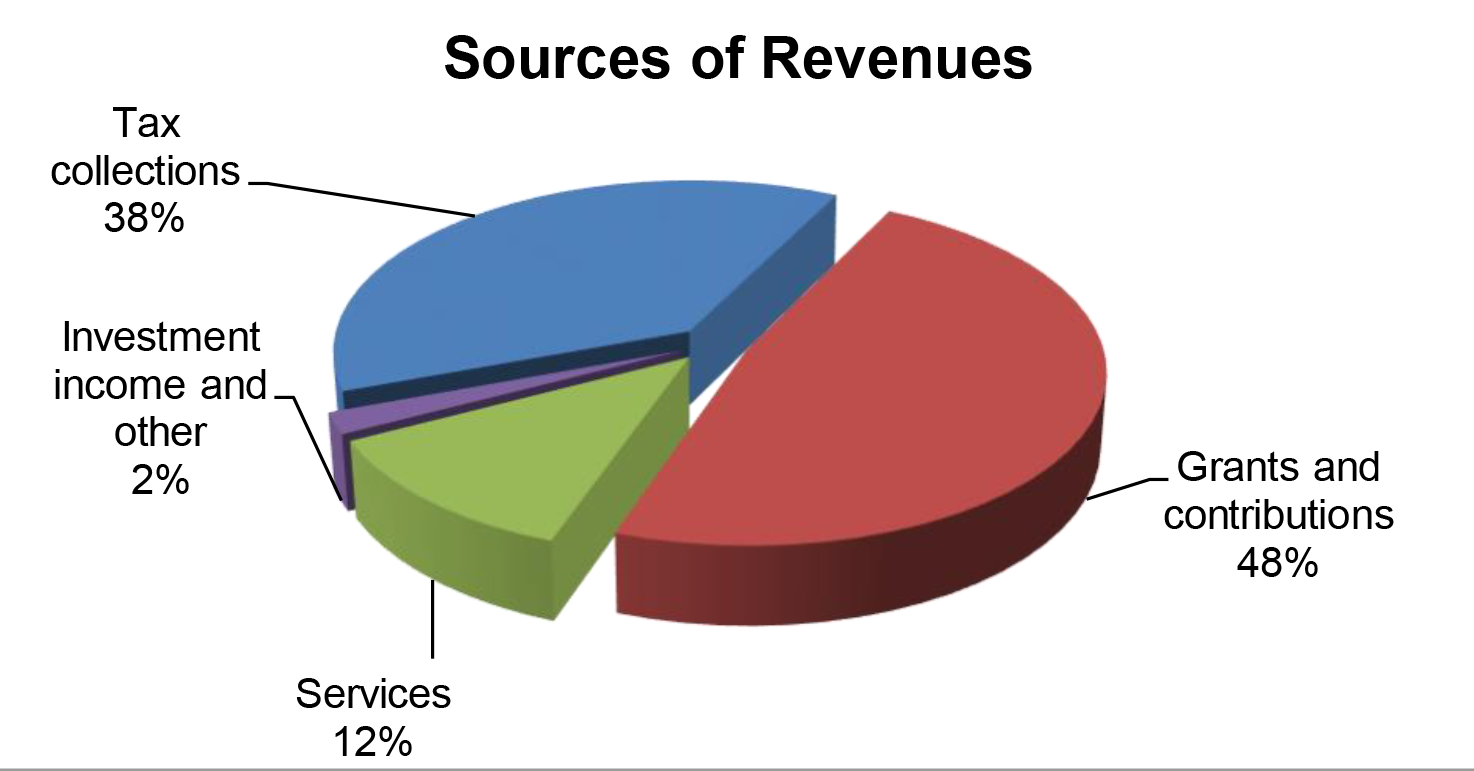

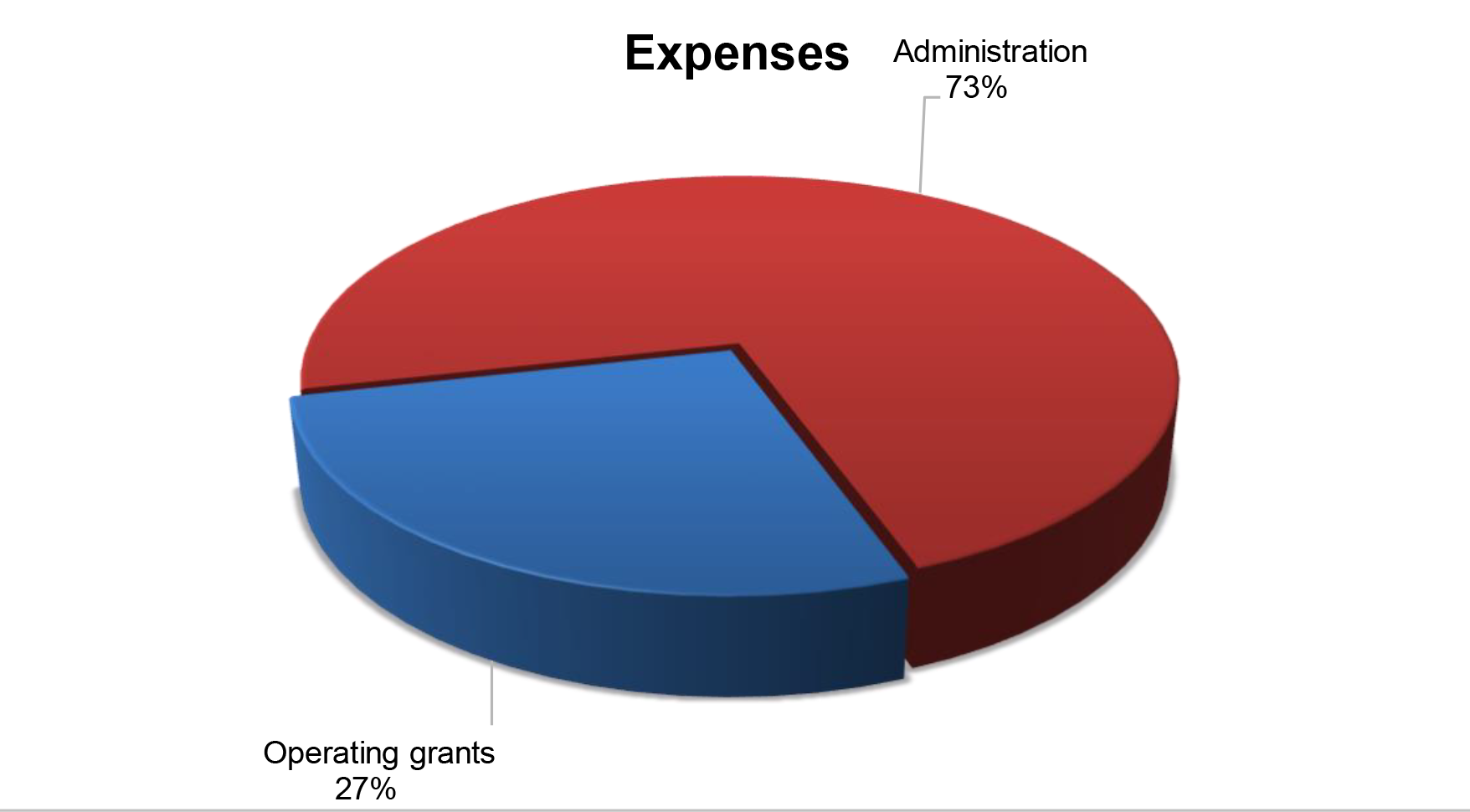

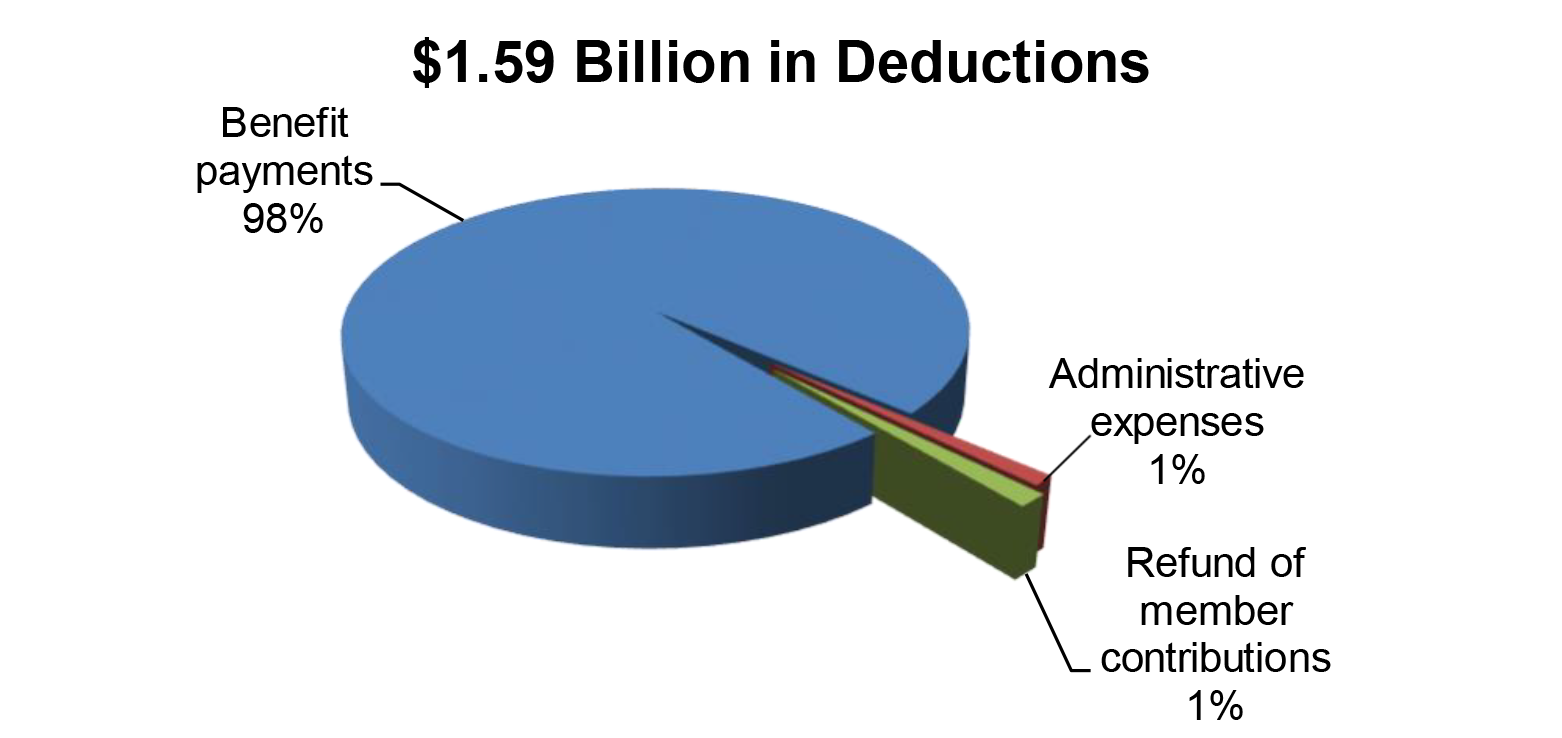

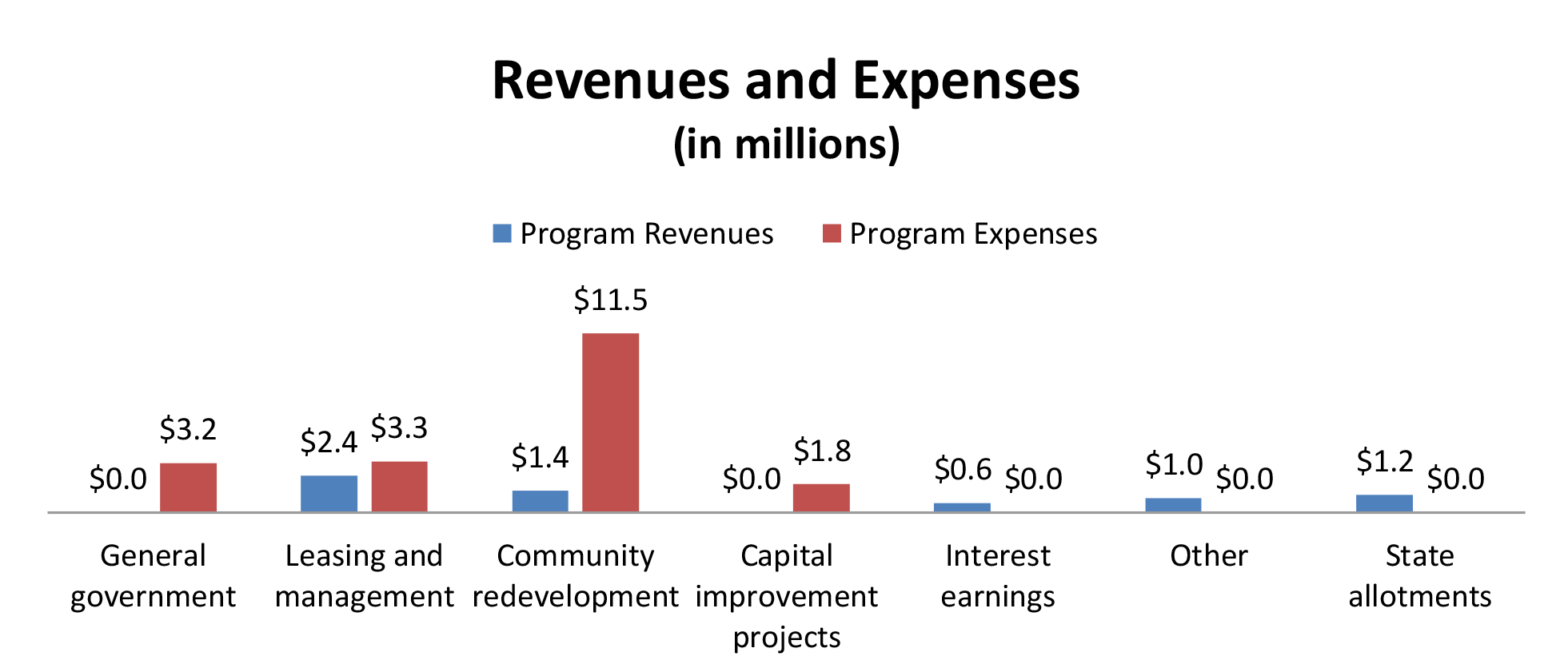

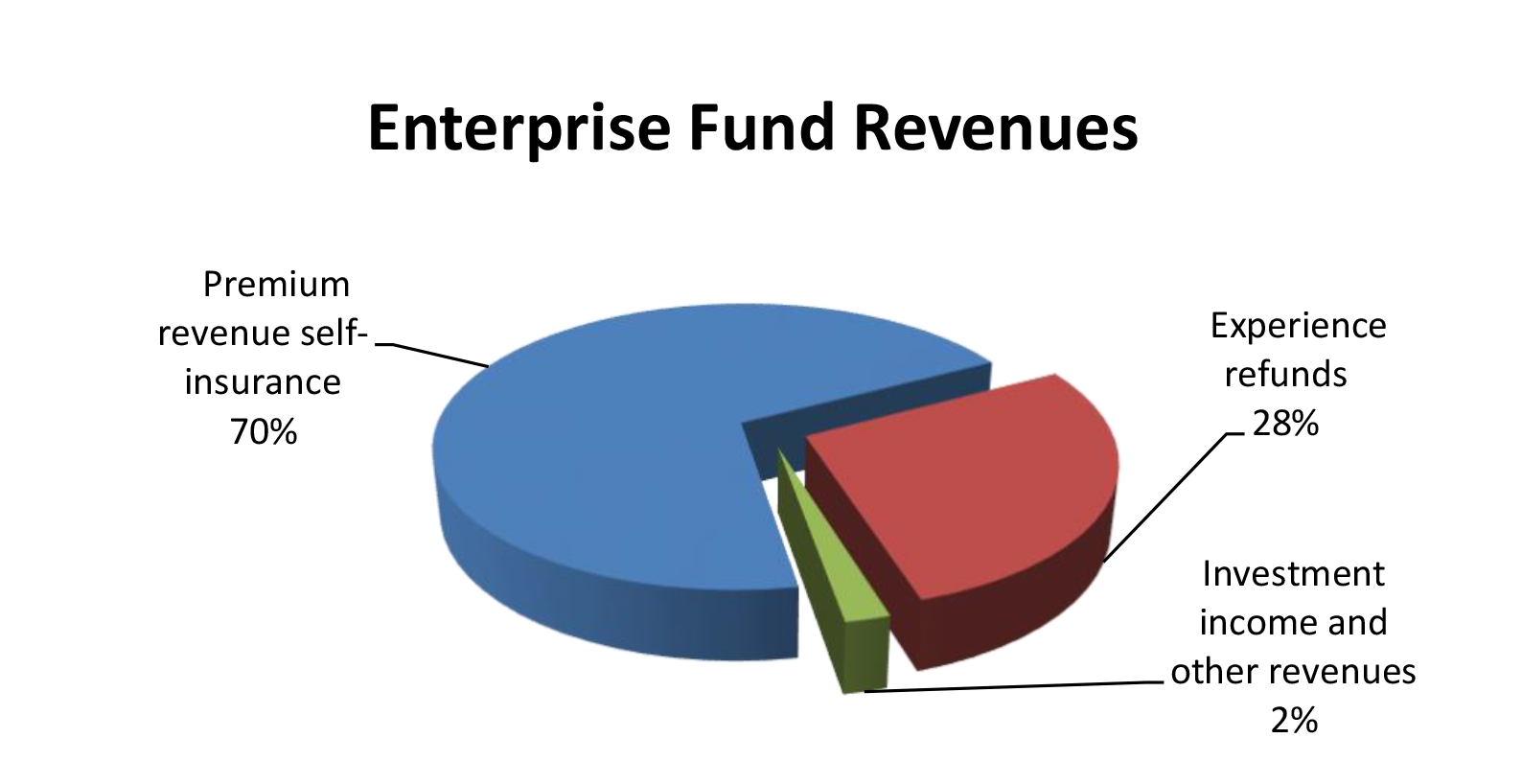

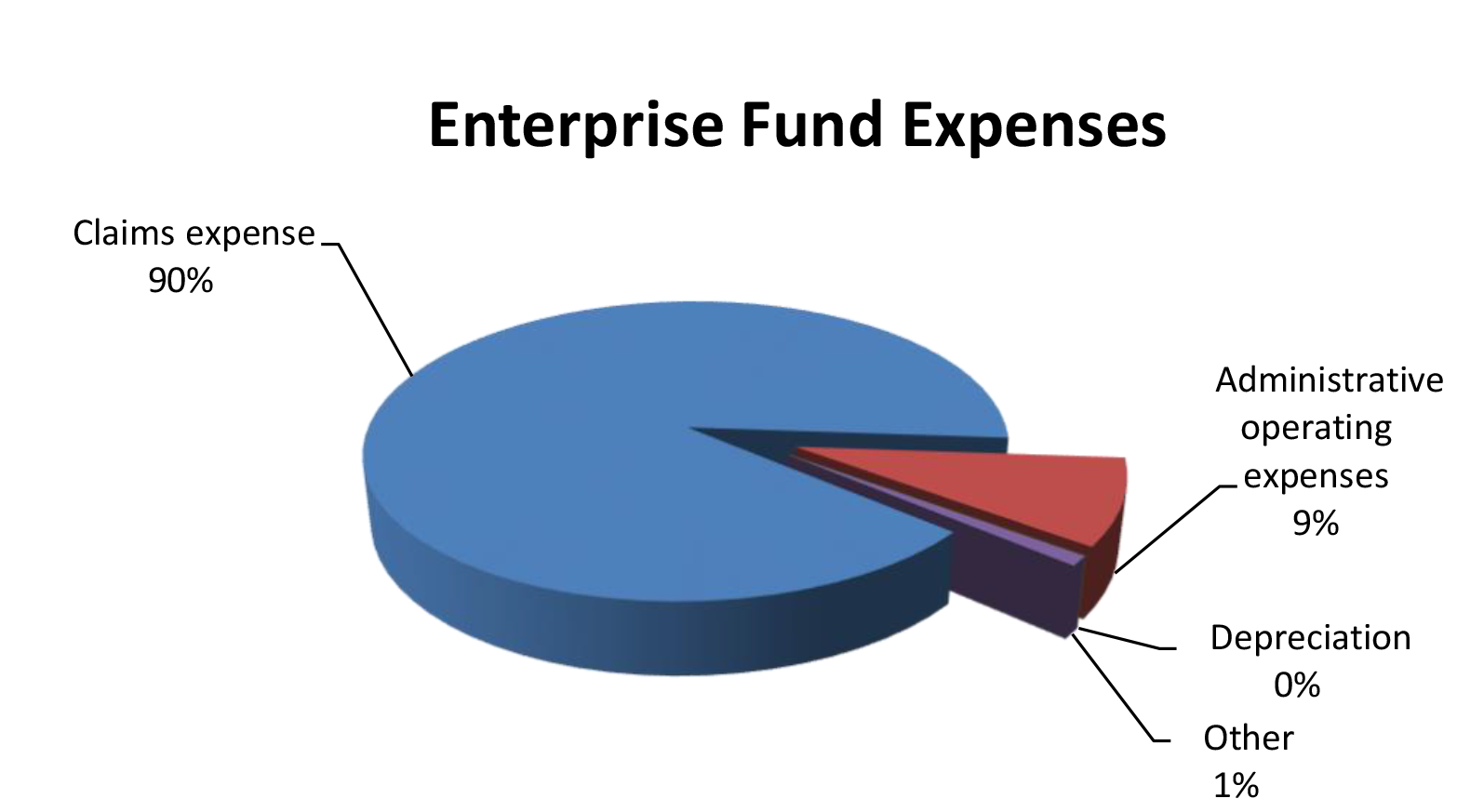

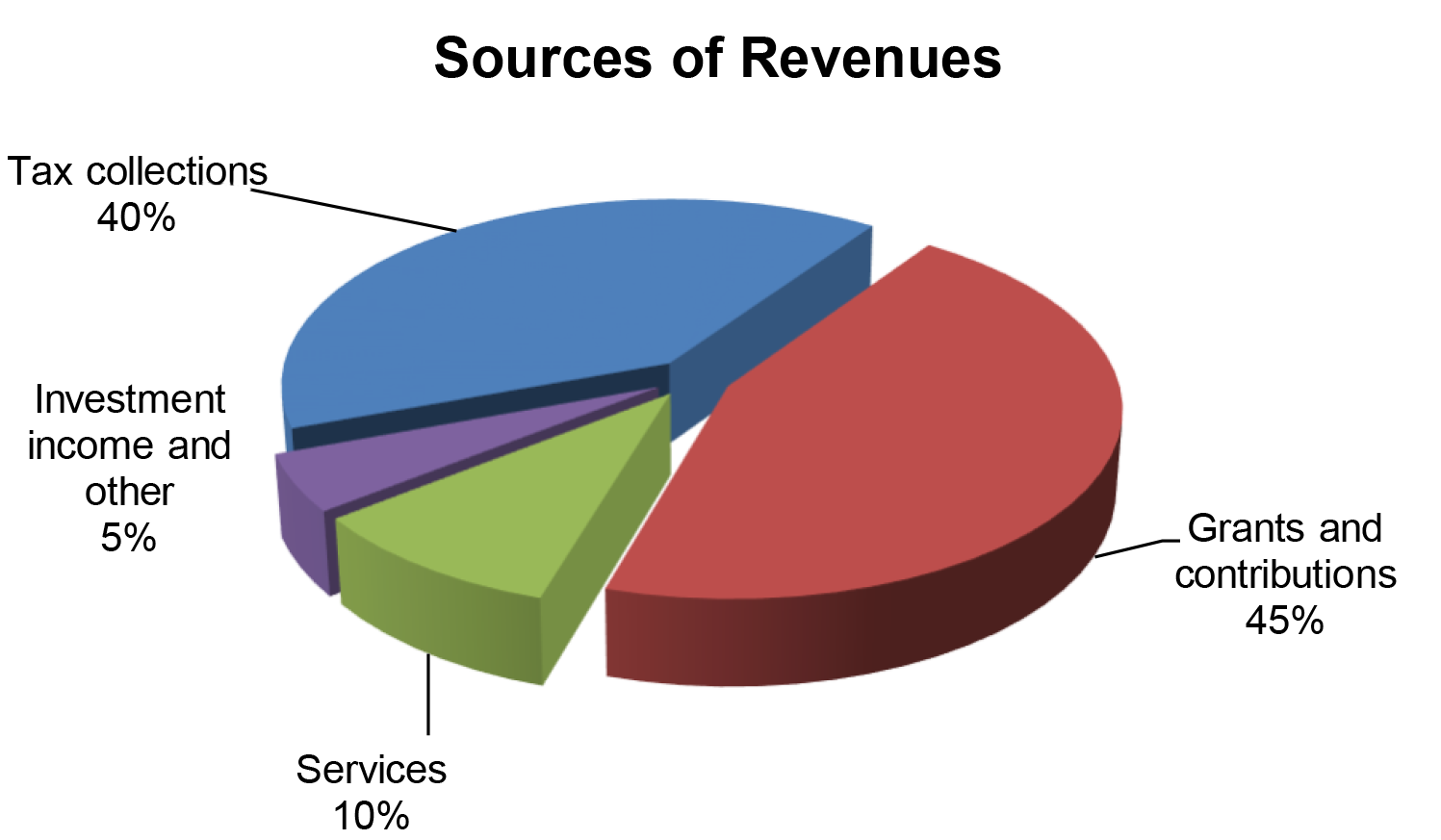

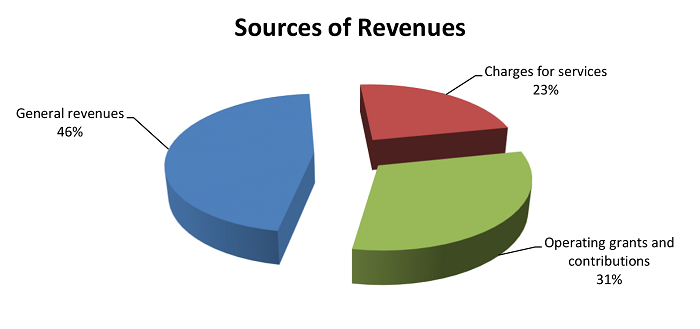

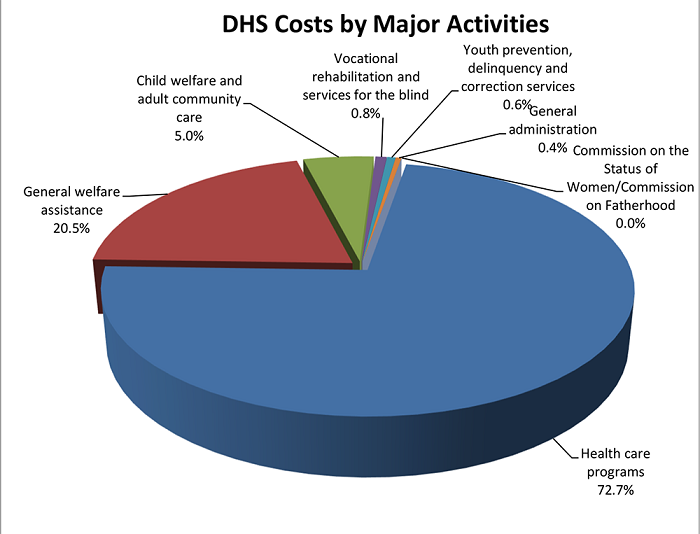

FOR THE FISCAL YEAR ended June 30, 2024, DHS reported total revenues of $5.11 billion and total expenses of $5.14 billion. Revenues consisted of $1.56 billion in state allotments, net of lapsed amounts plus non-imposed employee fringe benefits, and $3.55 billion in operating grants from the federal government. Revenues from these federal grants paid for 69.2 percent of the cost of DHS’ activities.

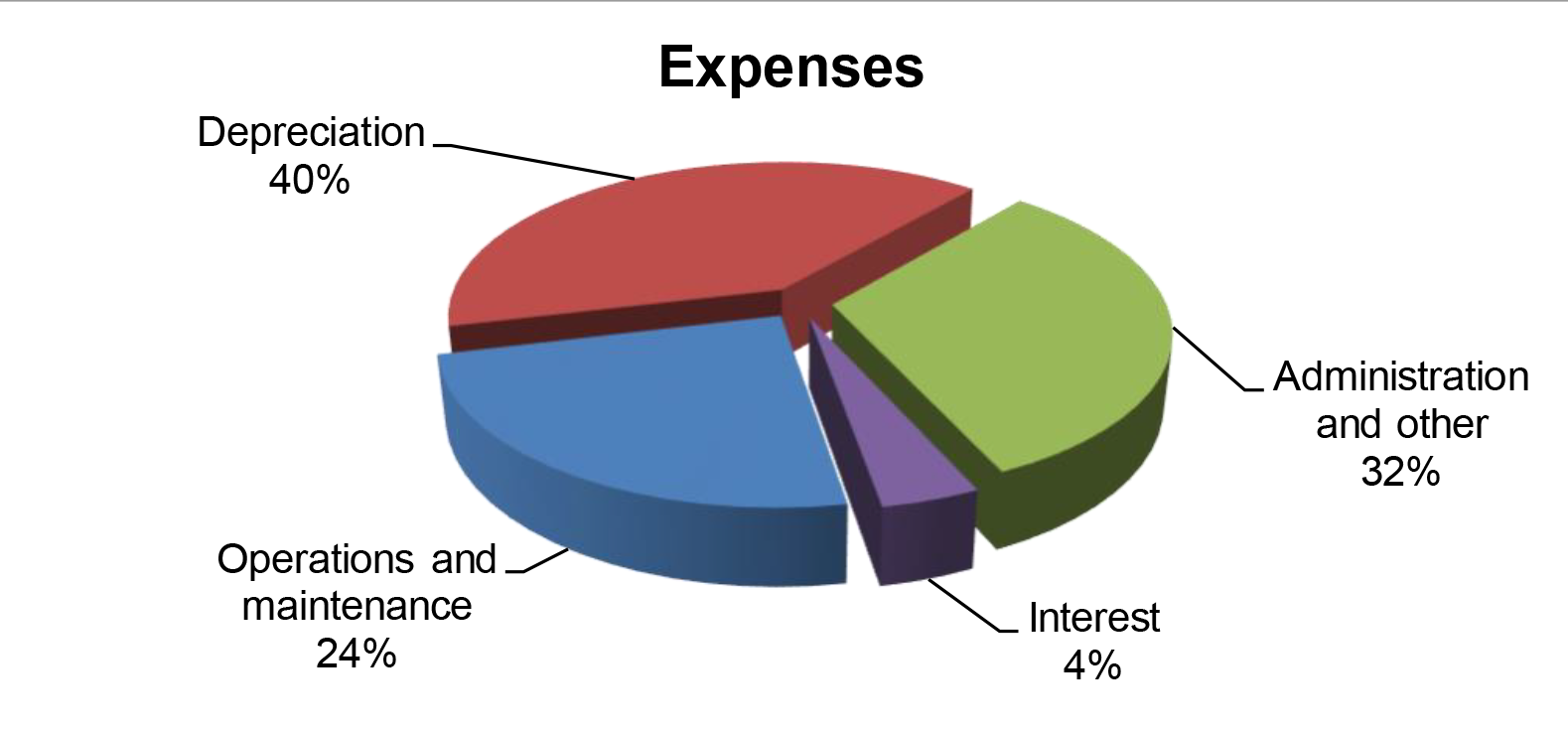

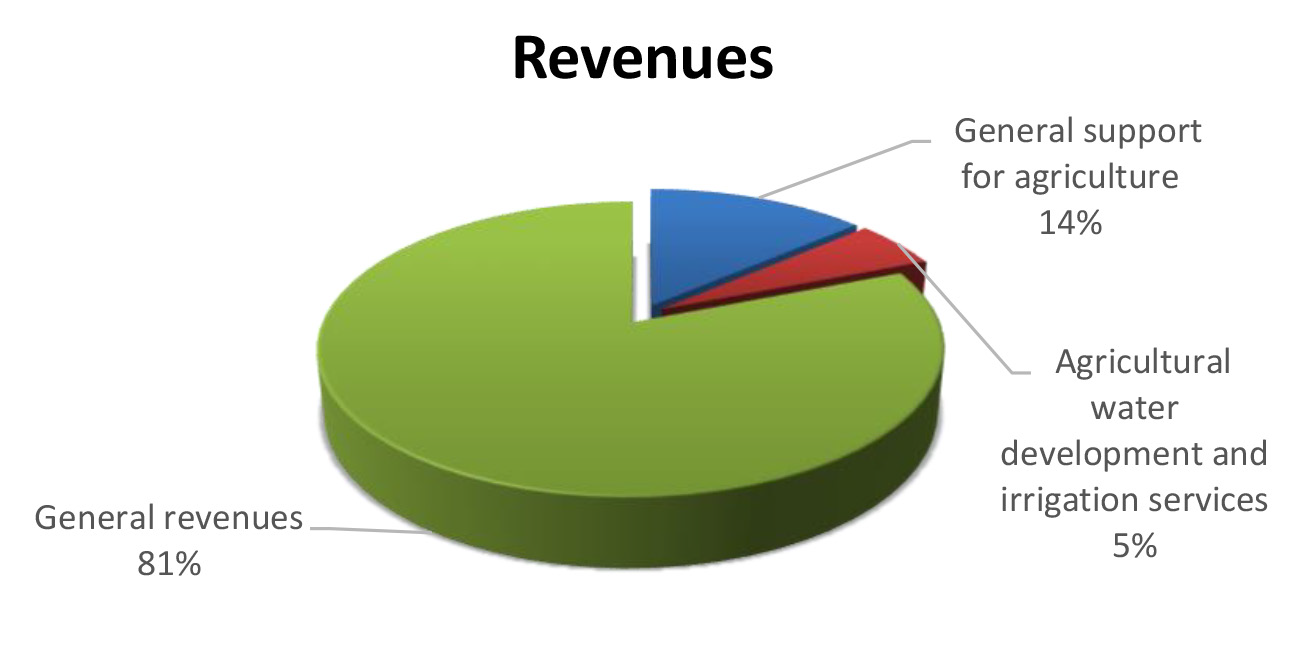

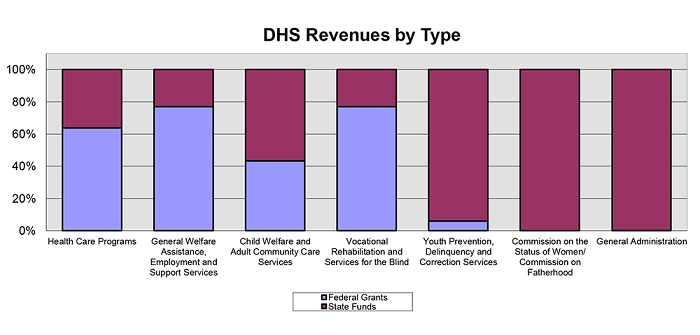

Health care and general welfare assistance programs comprised 70.9 and 22.9 percent, respectively, of the total cost. The following chart presents each major activity as a percentage of the total cost of all DHS activities.

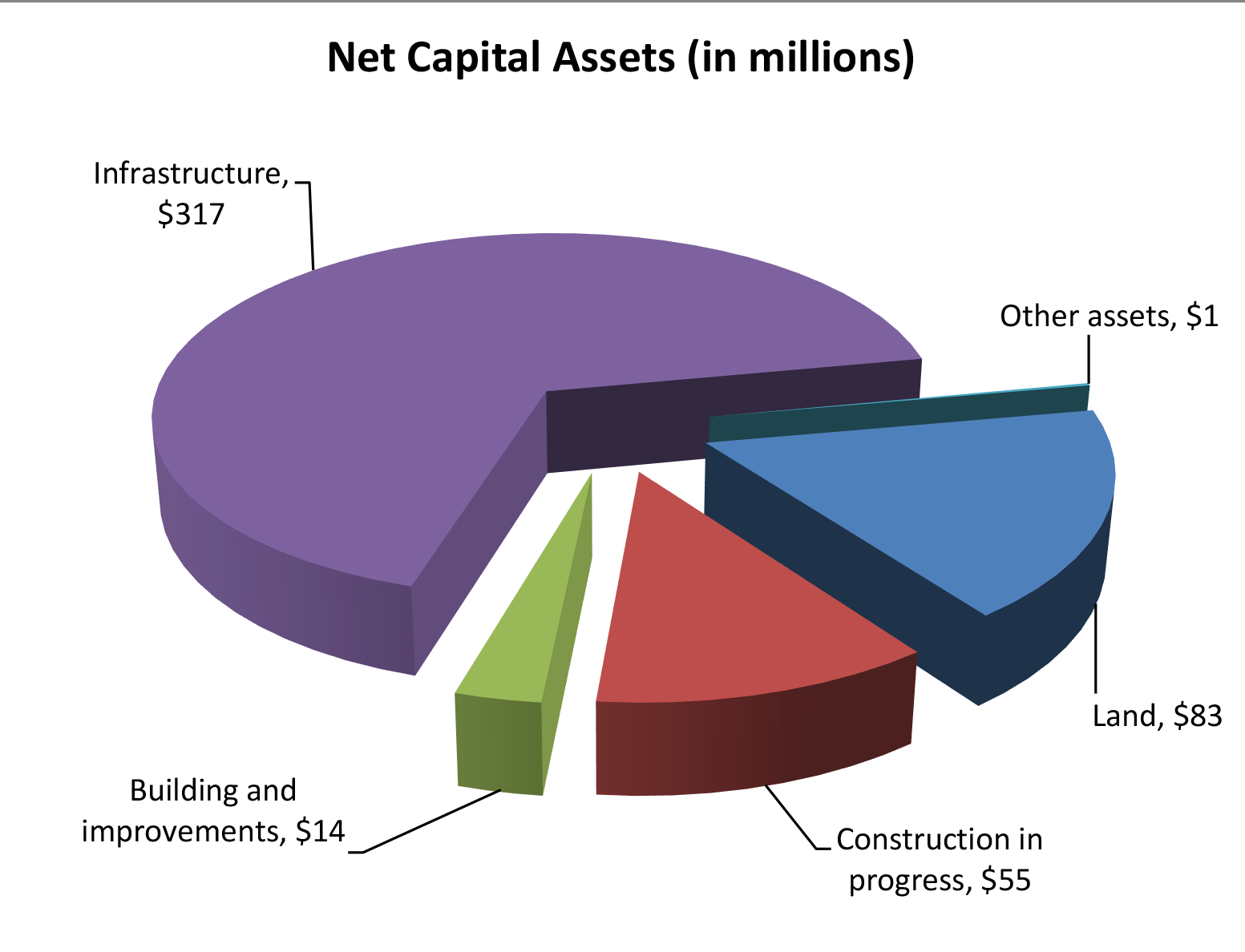

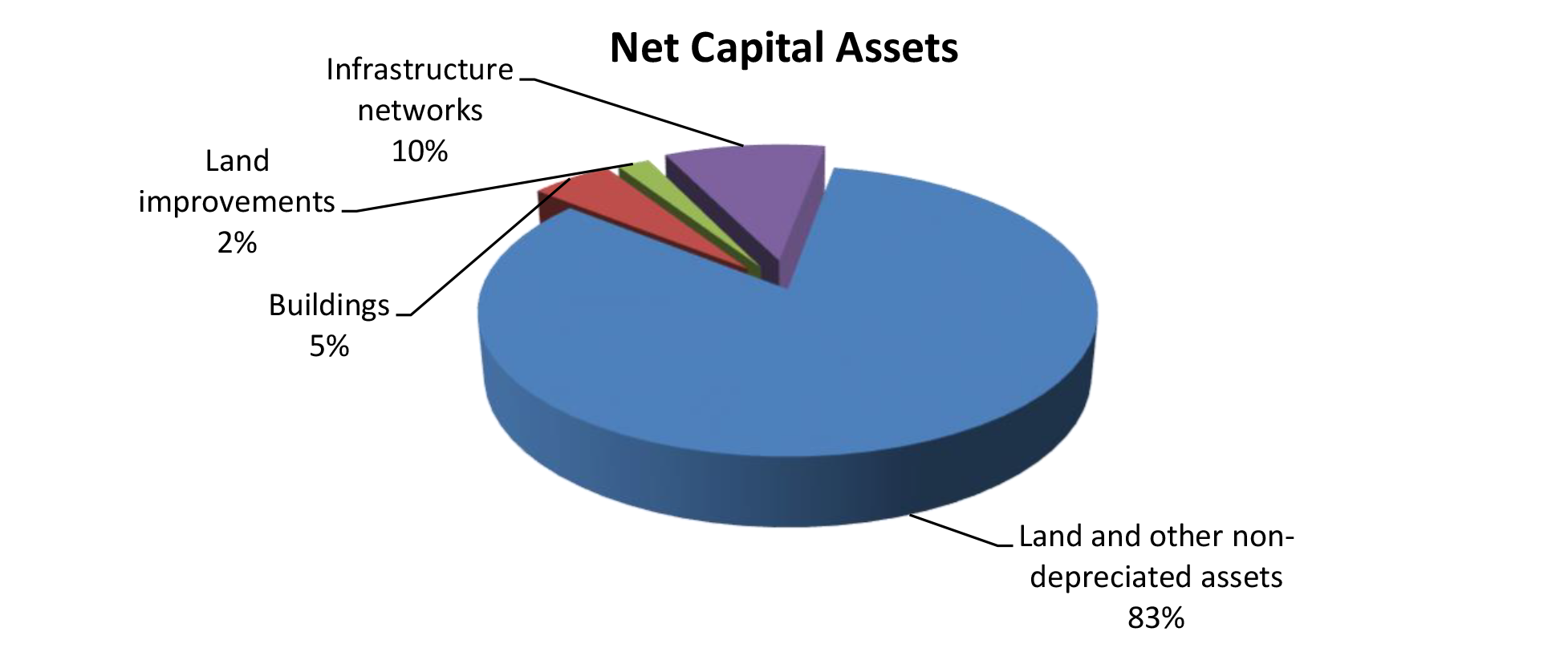

As of June 30, 2024, DHS’ total assets of $771 million included (1) cash of $467.9 million, (2) receivables of $218.77 million, and (3) net capital assets of $84.56 million. Total liabilities of $572.6 million included (1) vouchers payable of $60 million, (2) accrued wages and employee benefits of $34.6 million, (3) amounts due to the state general fund of $150.69 million, (4) amounts due to other governments of $170.98 million, (5) accrued medical assistance payable of $139.5 million, and (6) accrued compensated absences of $16.82 million.

Auditors’ Opinions DHS RECEIVED AN UNMODIFIED OPINION that its financial statements are presented fairly, in all material respects, in accordance with generally accepted accounting principles. DHS received a qualified opinion on its compliance for all major federal programs, except for COVID-19 Coronavirus State and Local Fiscal Recovery Funds, Rehabilitation Services – Vocational Rehabilitation Grants to States, COVID-19 Low-Income Home Energy Assistance, and COVID-19 Medicaid Cluster, which received an unmodified opinion in accordance with the Uniform Guidance.

Findings THE AUDITORS IDENTIFIED two significant deficiencies in internal control over financial reporting that were required to be reported under Government Auditing Standards.

A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. The significant deficiencies are described on pages 59-61 of the report.

There were six material weaknesses in internal control over compliance that were required to be reported in accordance with the Uniform Guidance. A material weakness in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented or detected and corrected on a timely basis. The material weaknesses are described on pages 63-70 and 72 of the report.

There were six significant deficiencies in internal control over compliance that were required to be reported in accordance with the Uniform Guidance. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. The deficiencies are described on pages 62, 71, and 73-77 of the report.

About the DepartmentThe Department of Human Services (DHS) works to provide benefits and services to individuals and families in need. The majority of DHS’ budget is comprised of federal funds. DHS’ mission is to direct its funds toward protecting and helping those least able to care for themselves and to provide services designed toward achieving self-sufficiency for clients as quickly as possible. Activities include health care programs; general welfare assistance, employment and support services; child welfare and adult community care services; vocational rehabilitation and services for the blind; youth prevention, delinquency and correction services; and general administration. Attached programs include the Commission on the Status of Women and the Commission on Fatherhood.

Financial Statements, Fiscal Year Ended June 30, 2024

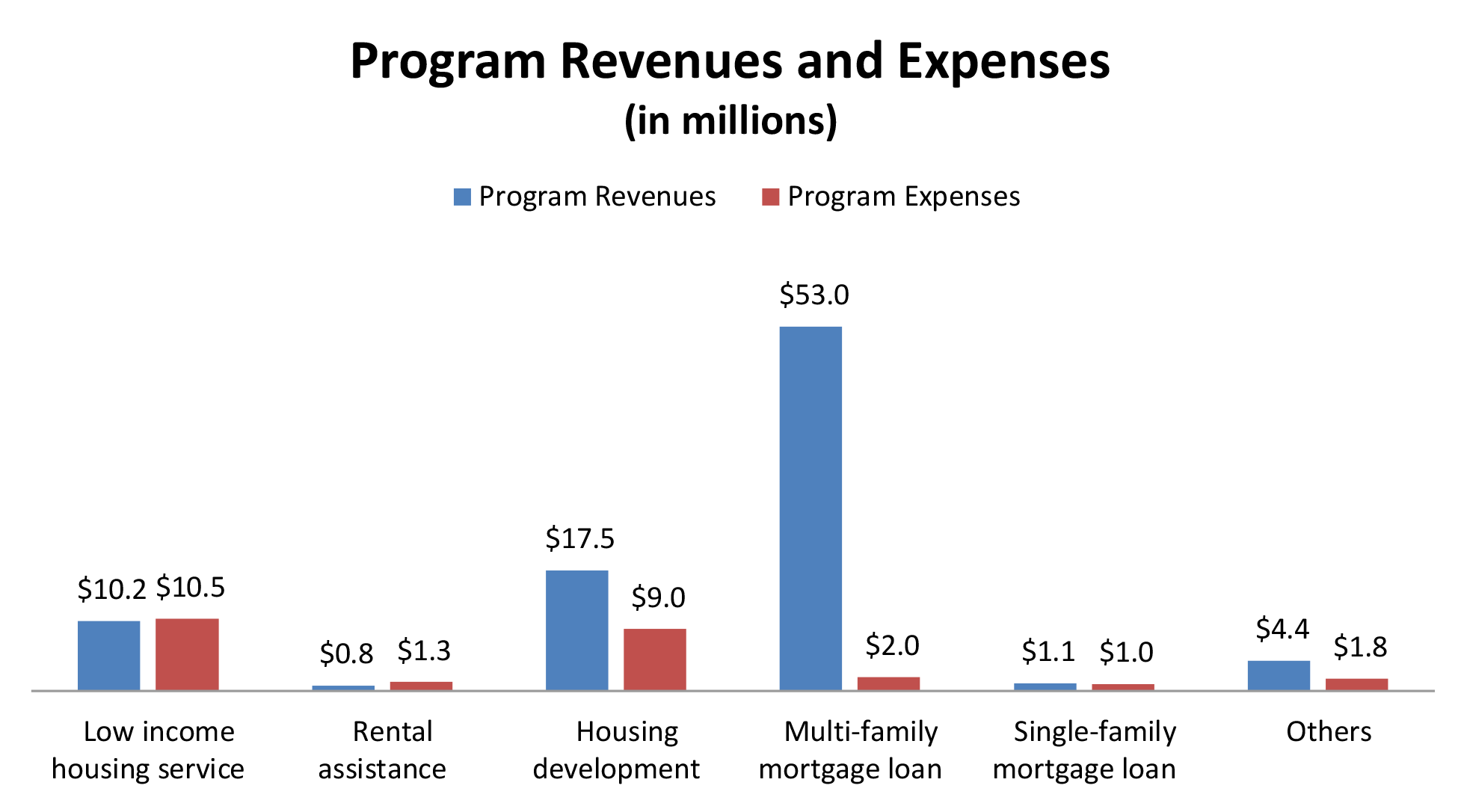

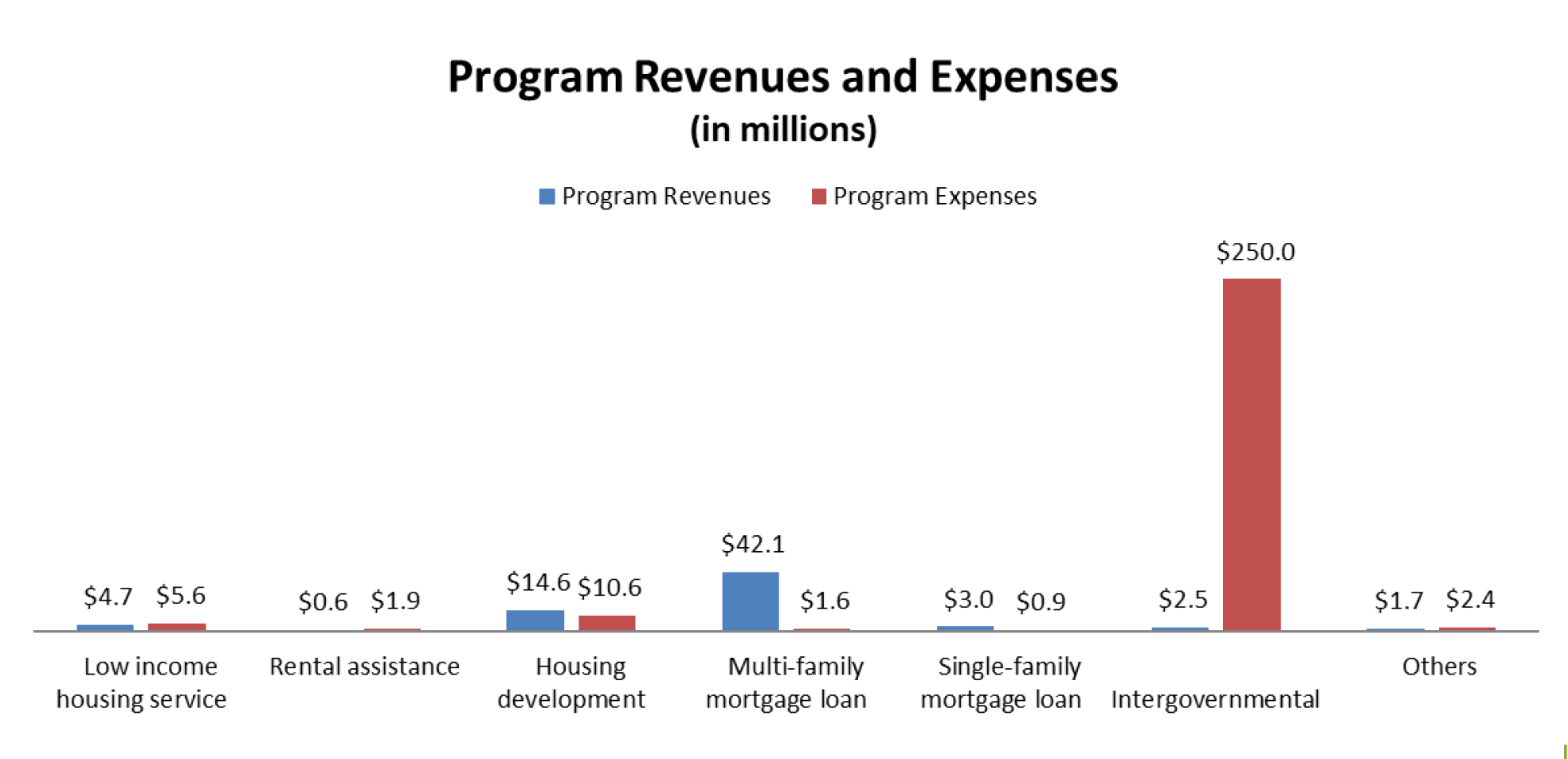

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the Department of Hawaiian Home Lands, as of and for the fiscal year ended June 30, 2024, and to comply with the requirements of Title 2, U.S. Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by Accuity LLP.

Financial Highlights

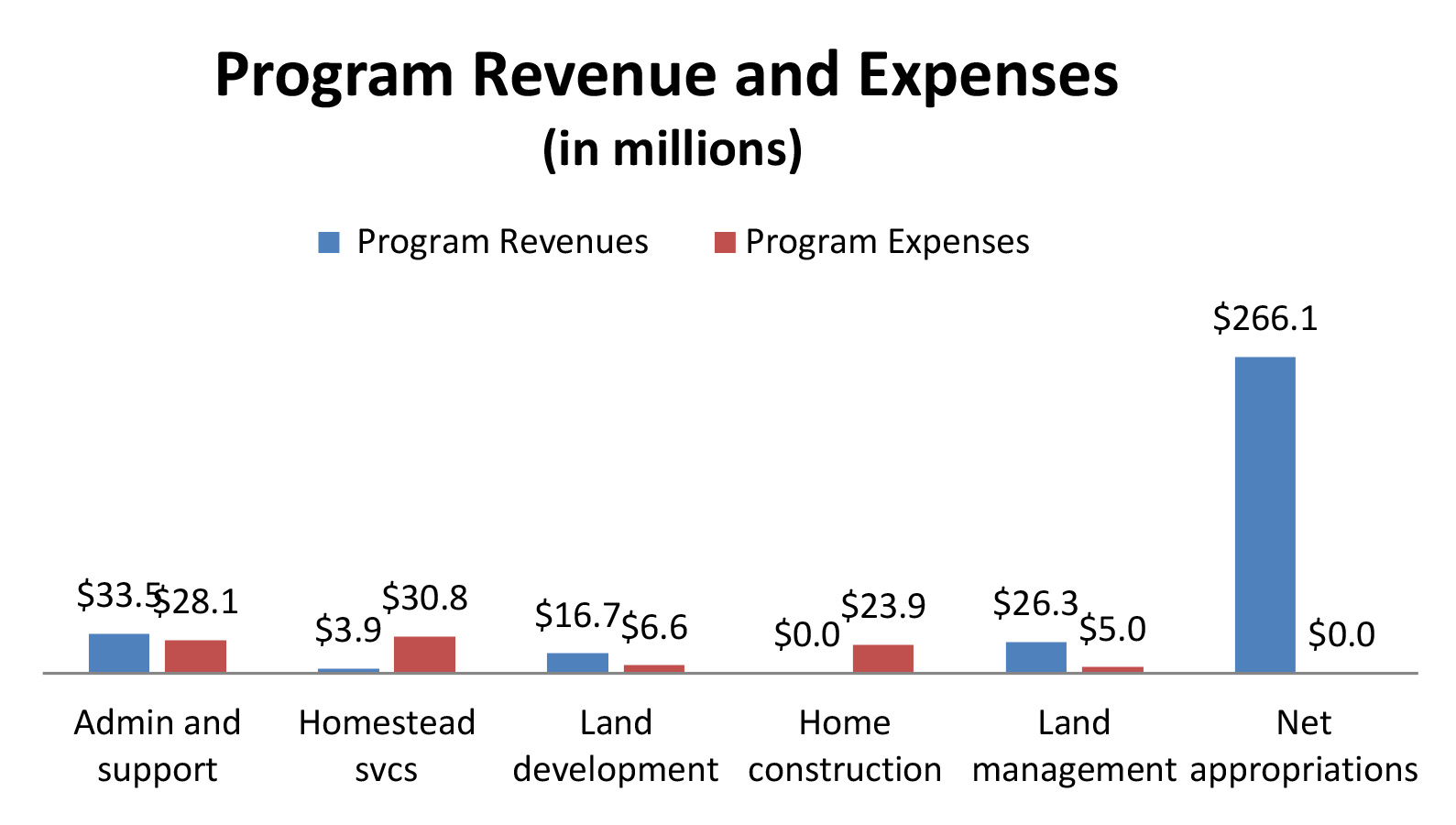

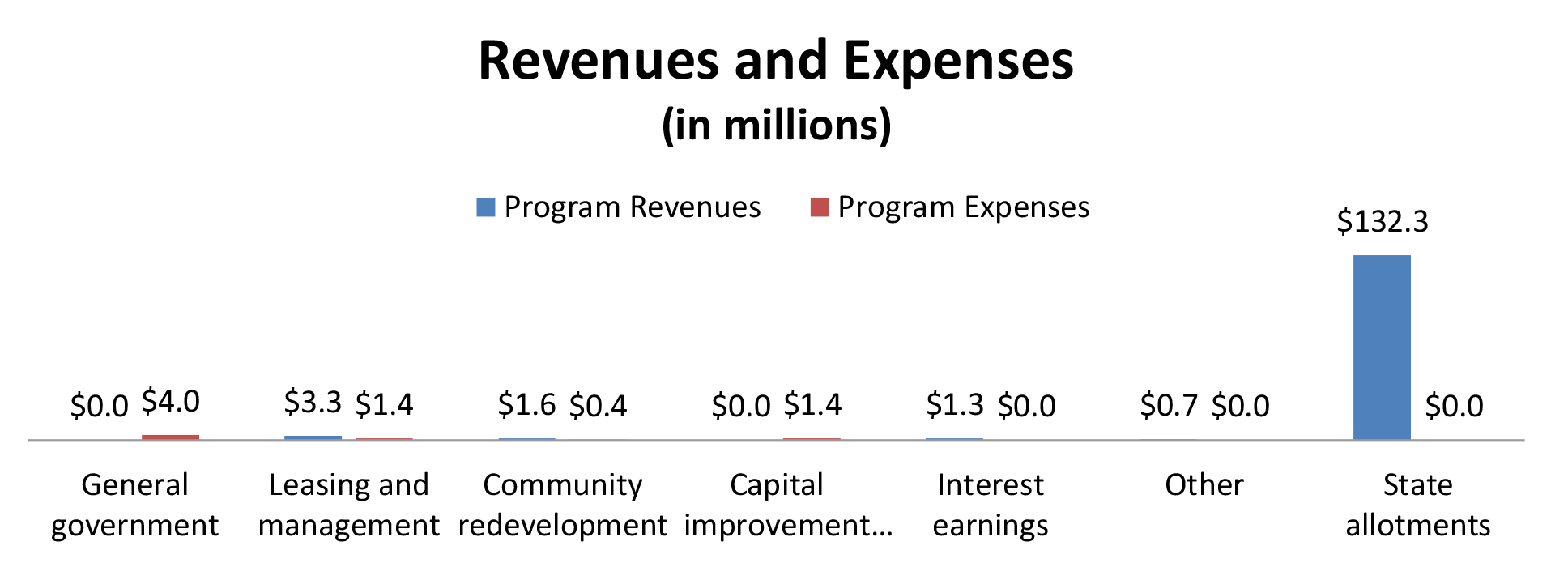

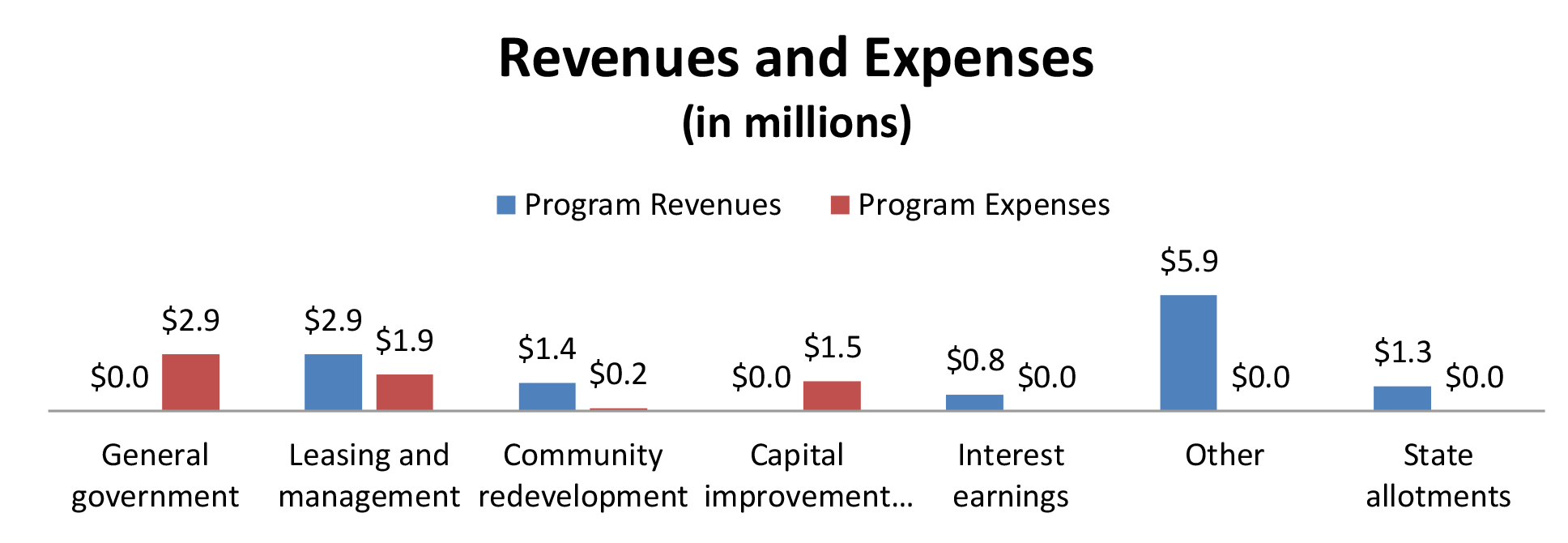

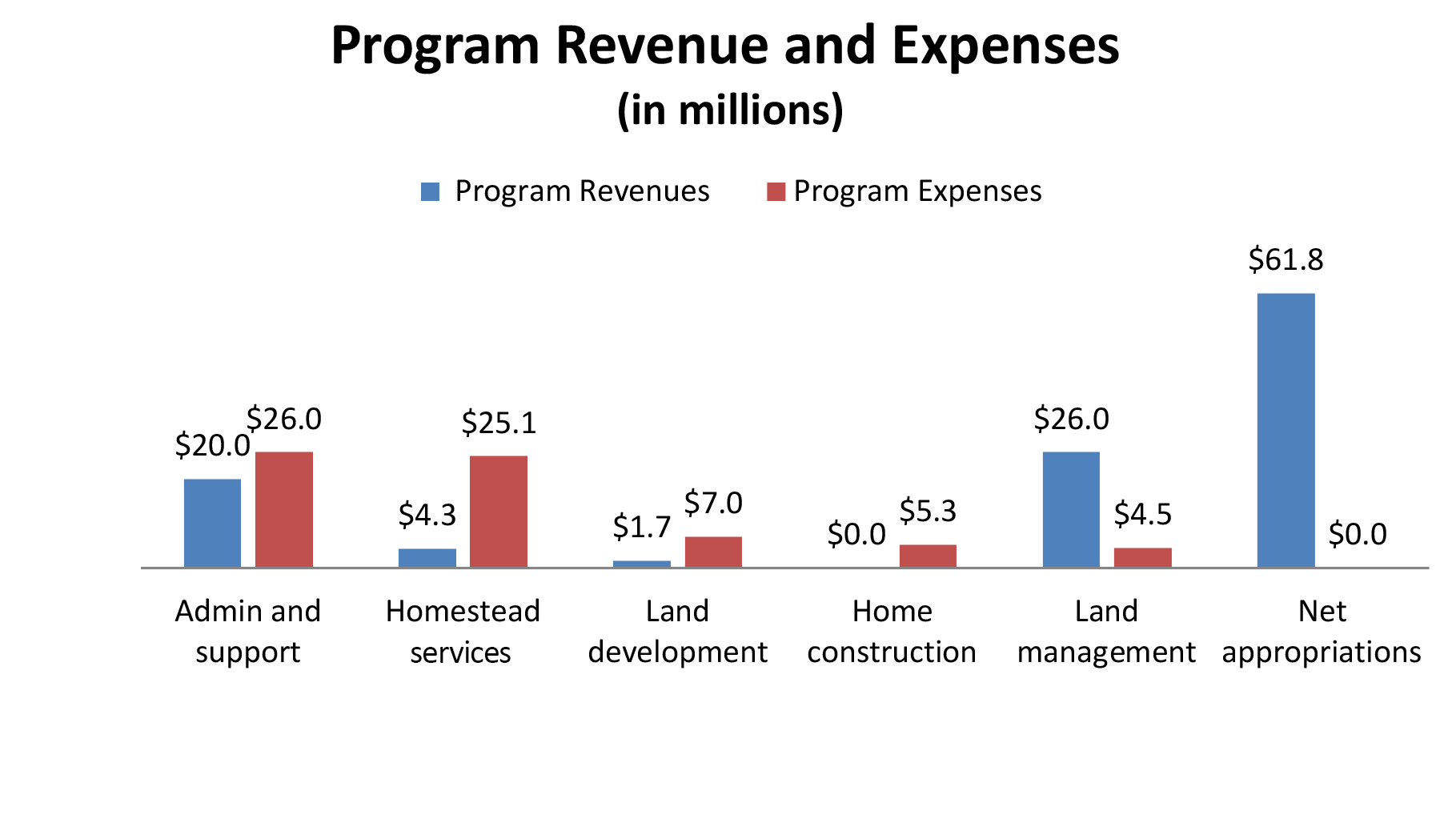

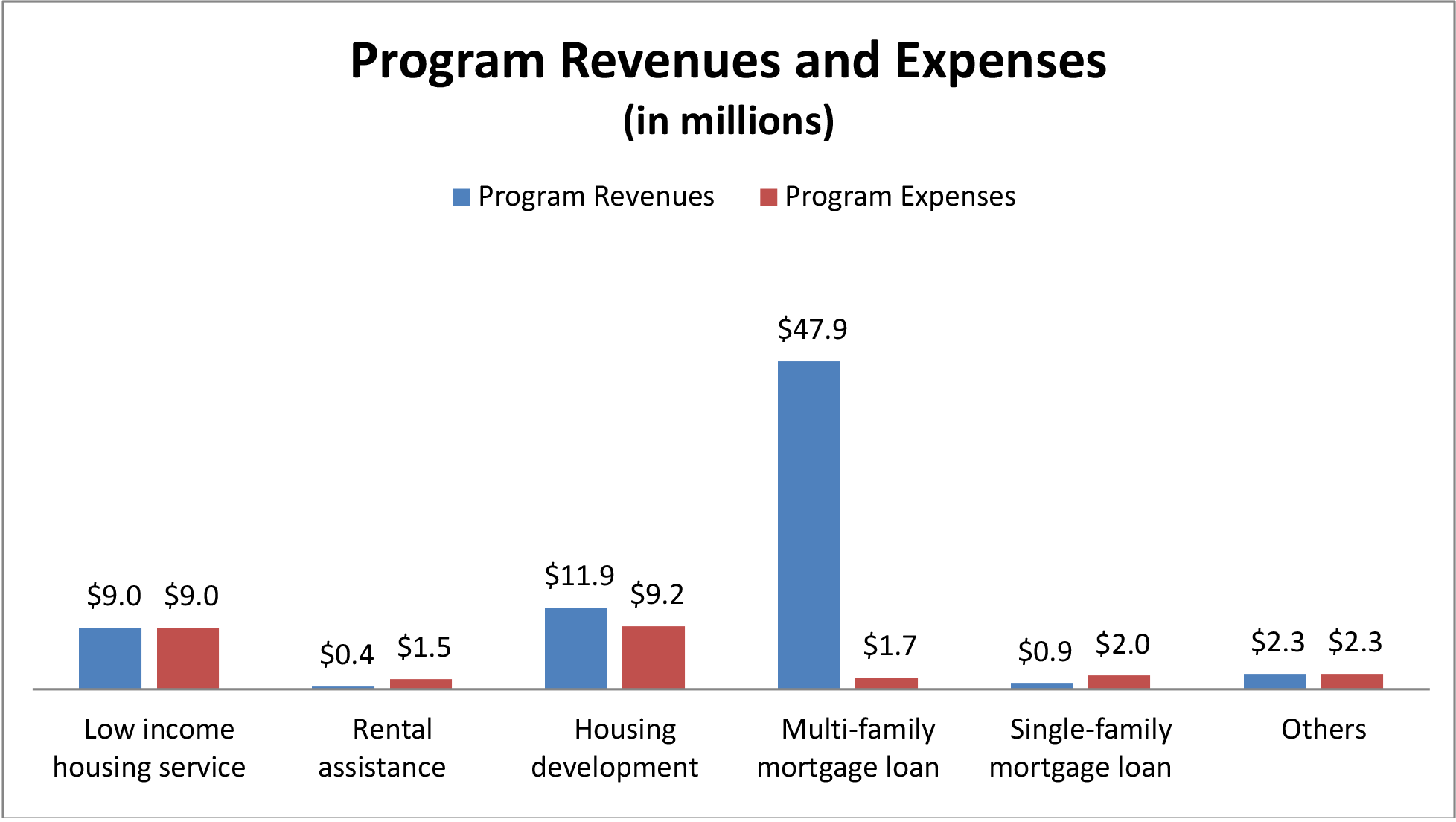

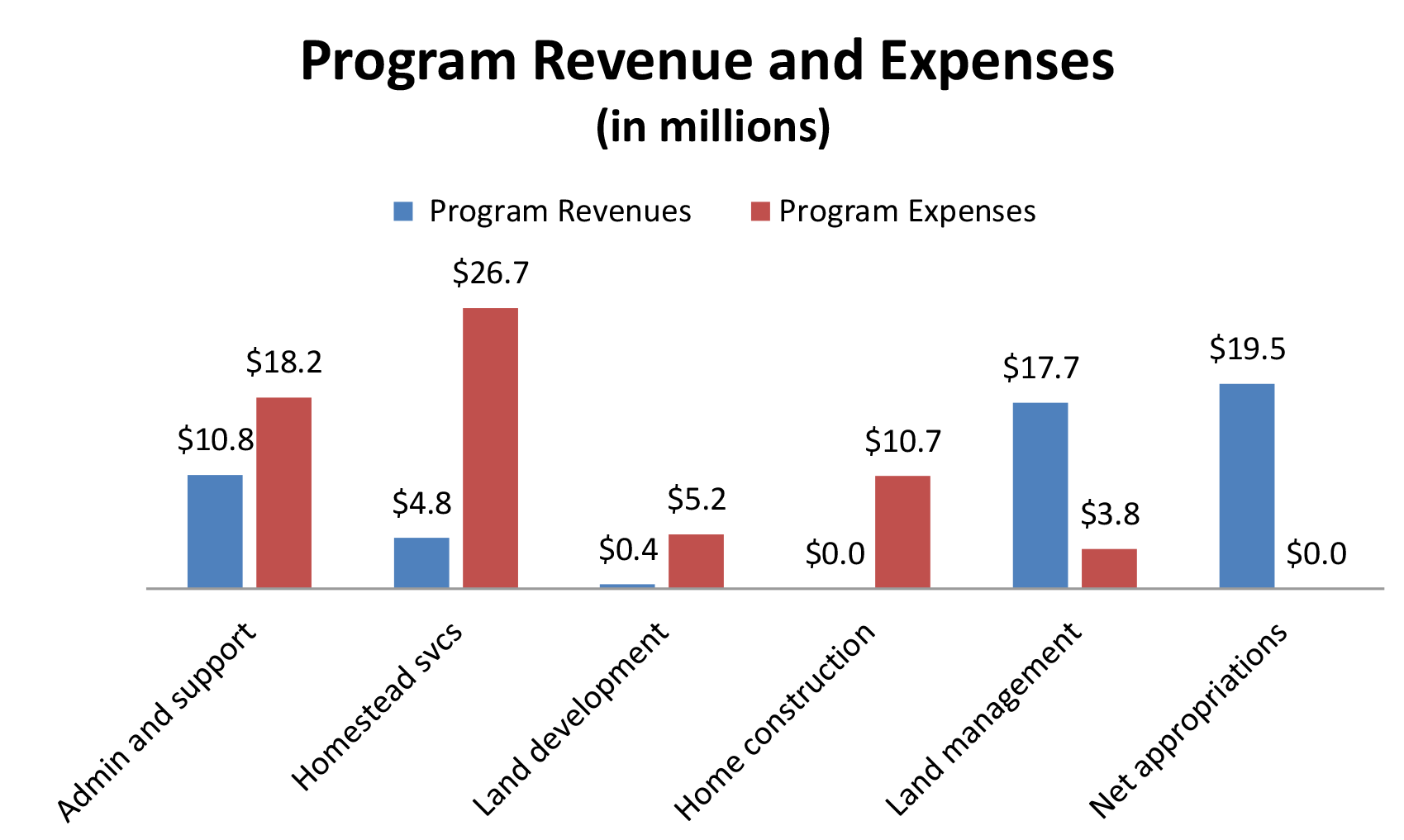

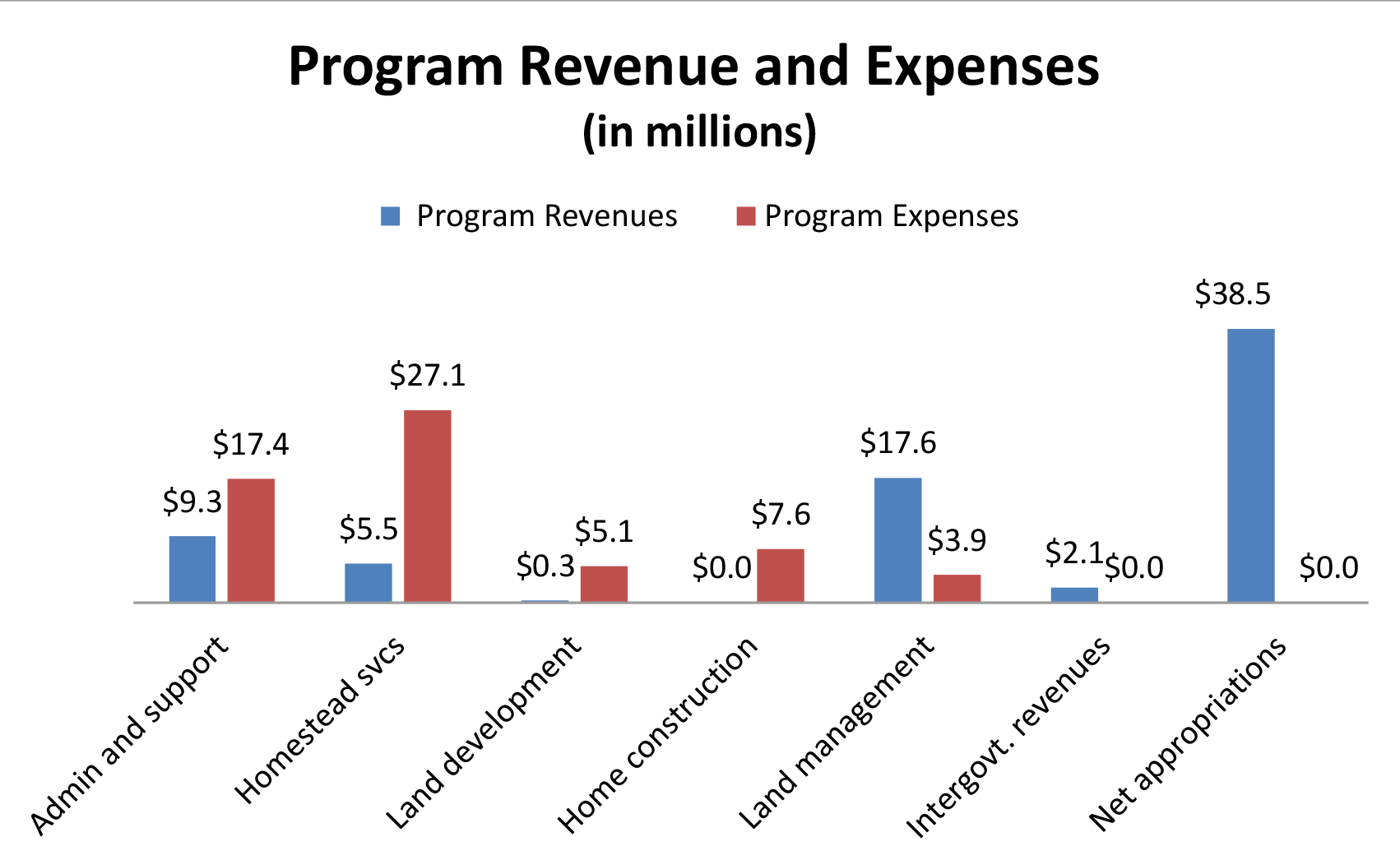

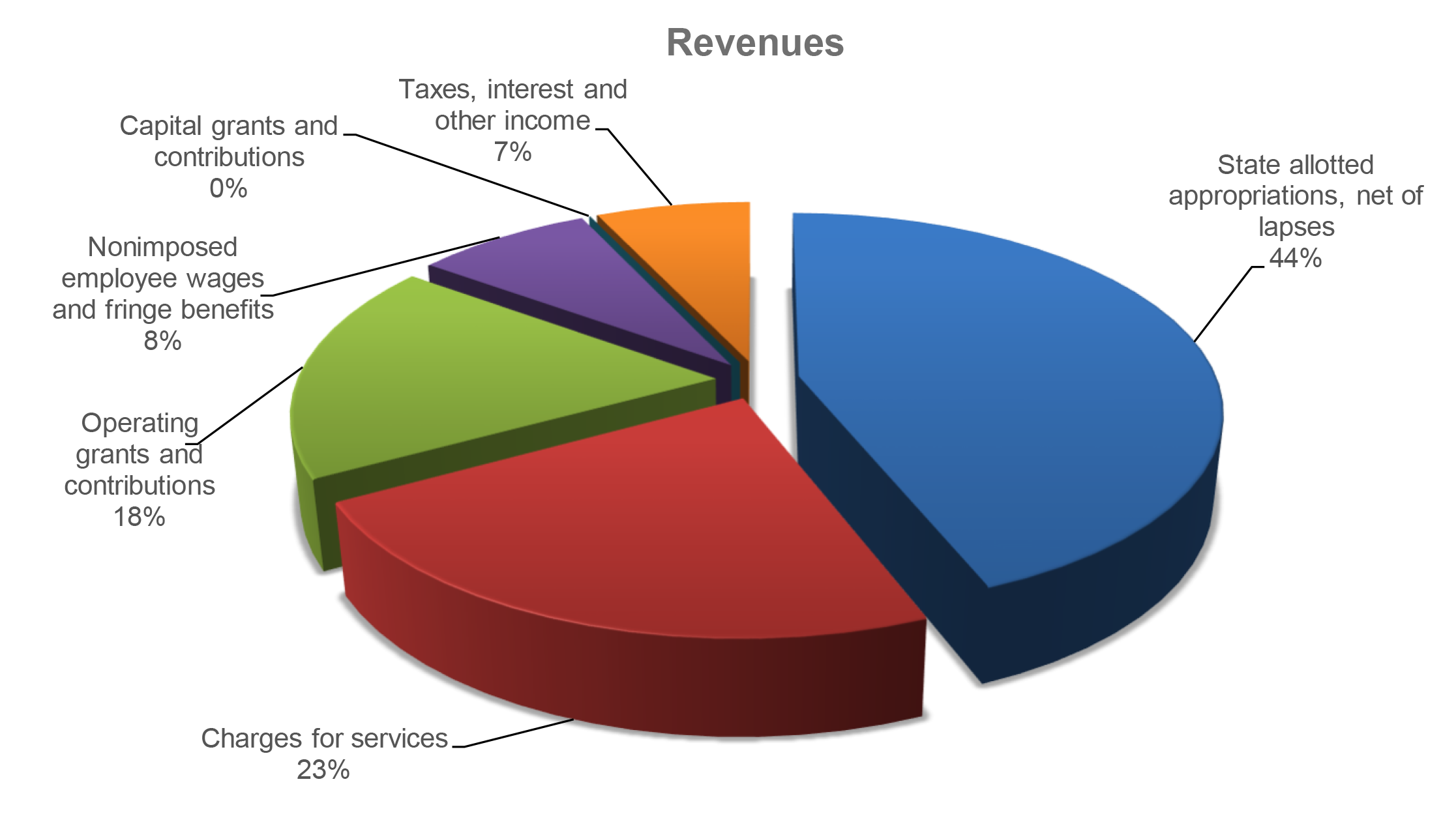

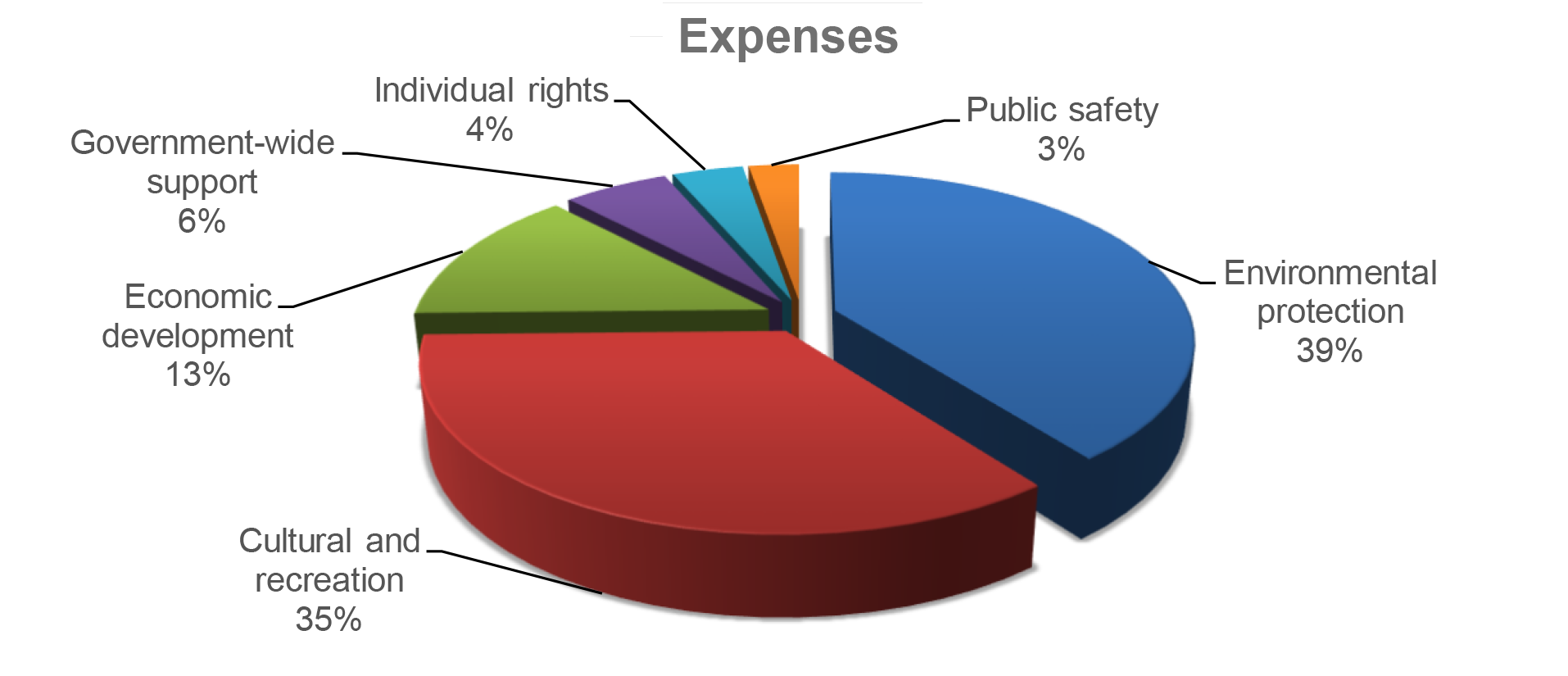

FOR THE FISCAL YEAR ended June 30, 2024, DHHL’s total revenues exceeded total expenses by $252 million. Revenues totaled $346.5 million and consisted of (1) program revenue of $80.4 million and (2) state appropriations, transfers, and adjustments of $266.1 million. Expenses totaled $94.4 million. Program revenues were comprised of interest income (approximately 33 percent), grants and contributions (23 percent), revenue from the general lease program (19 percent), and other sources (25 percent).

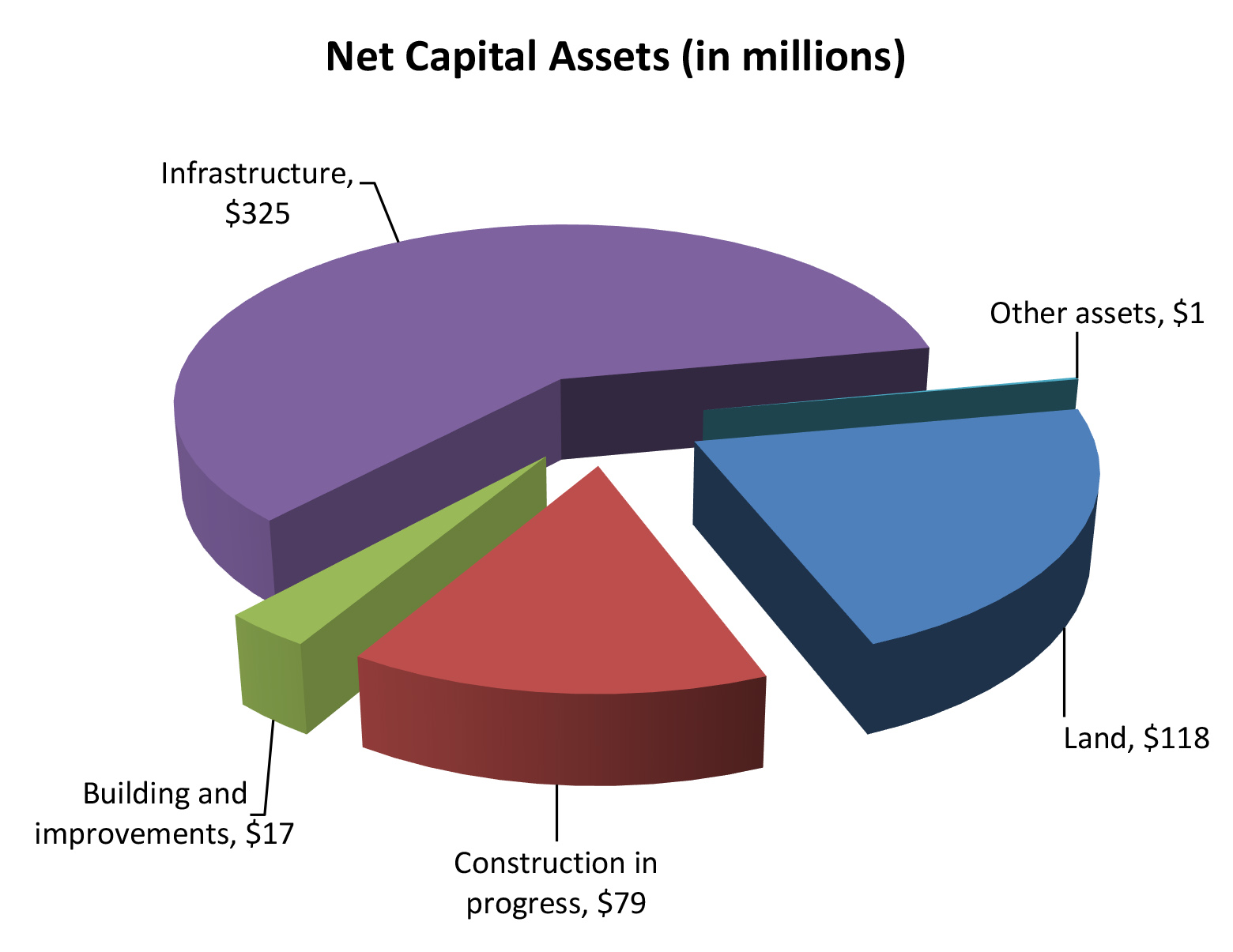

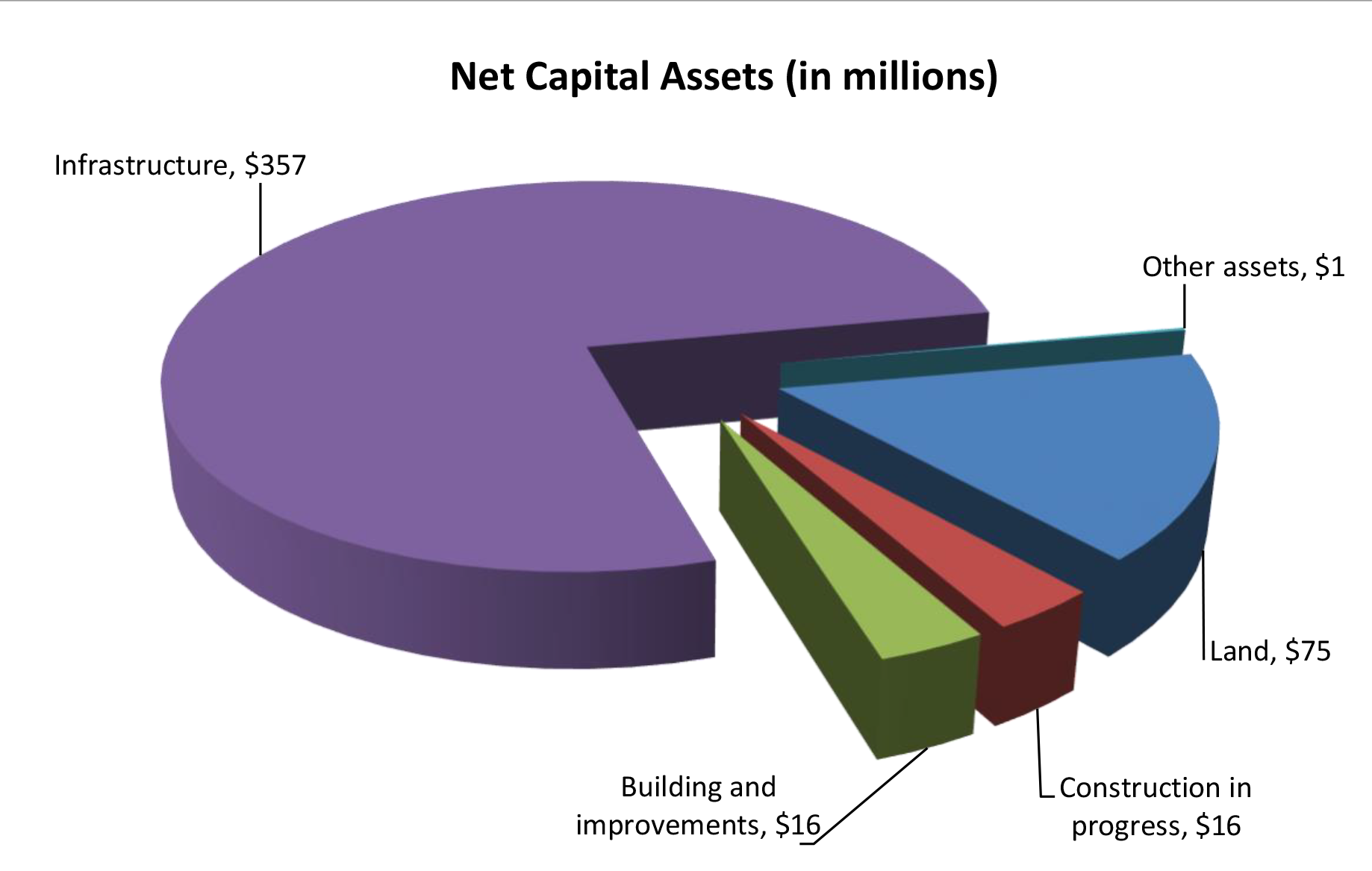

As of June 30, 2024, total assets of $1.78 billion exceeded total liabilities of $391 million, resulting in a net position balance of $1.39 billion. Total assets included net capital assets of $540 million, cash of $828 million, loans receivable of $84 million, and other assets and deferred outflows of resources of $331 million. Loans receivable consisted of 1,290 loans made to Native Hawaiian lessees for the purposes specified in the Hawaiian Homes Commission Act. Loans are for a maximum amount of approximately $452,000 and for a maximum term of 40 years. Interest rates on outstanding loans range up to 10 percent. Total liabilities included bonds and lease liabilities totaling $40 million and temporary deposits payable and other liabilities of $351 million.

Auditors’ Opinions DHHL RECEIVED AN UNMODIFIED OPINION that the financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles. DHHL also received an unmodified opinion on its compliance with major federal programs in accordance with the Uniform Guidance.

Findings THERE WERE NO REPORTED DEFICIENCIES IN INTERNAL CONTROL over financial reporting that were considered to be material weaknesses and no instances of noncompliance or other matters that were required to be reported under Government Auditing Standards. However, the auditors identified one significant deficiency in internal control over financial reporting that was required to be reported under Government Auditing Standards. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. The significant deficiency is described on page 55 of the report.

There were no findings that were considered material weaknesses in internal control over compliance in accordance with the Uniform Guidance.

About the DepartmentThe Hawaiian Homes Commission Act sets aside certain public lands as Hawaiian home lands to be utilized in the rehabilitation of Native Hawaiians. These public lands are managed by the Department of Hawaiian Home Lands (DHHL), a state agency headed by the Hawaiian Homes Commission, whose primary responsibilities are to serve its beneficiaries and to manage this extensive land trust. DHHL provides direct benefits to Native Hawaiians in the form of 99-year homestead leases at $1 per year for residential, agricultural, or pastoral purposes, and financial assistance through direct loans, insured loans, or loan guarantees for home purchase, construction, home replacement, or repair. In addition to administering the homesteading program, DHHL leases trust lands not in homestead use at market value and issues revocable permits, licenses, and rights-of-entry. Its financial statements include the public trusts controlled by the Hawaiian Homes Commission.

Financial Statements, Fiscal Year Ended June 30, 2024

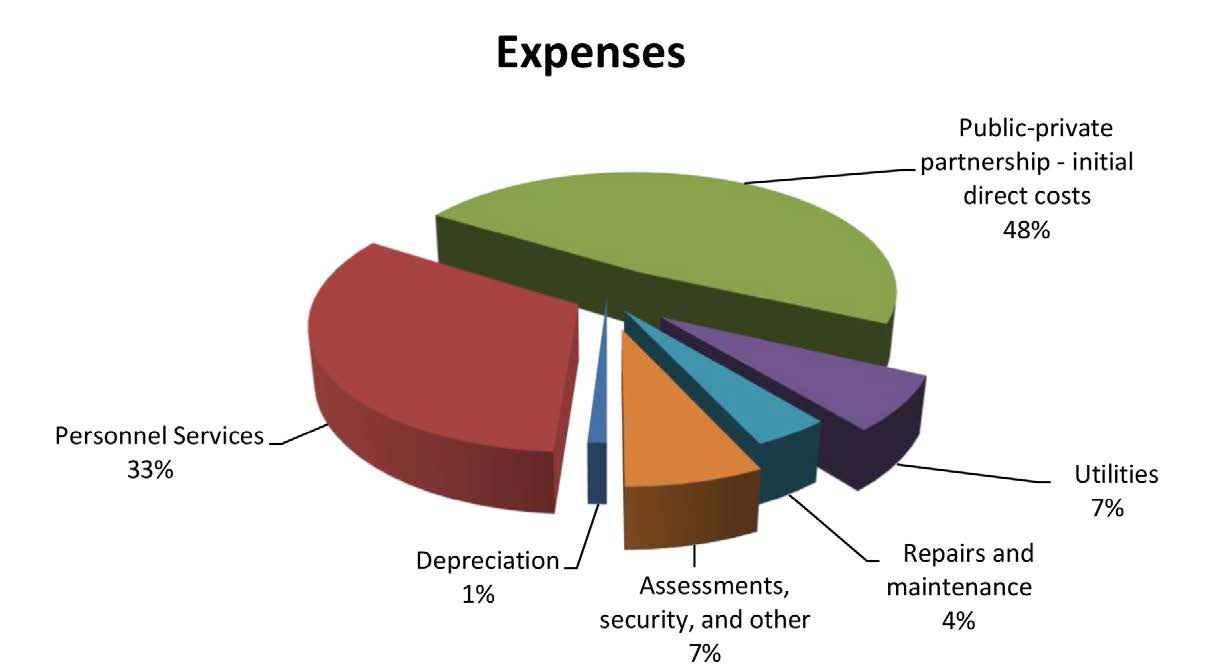

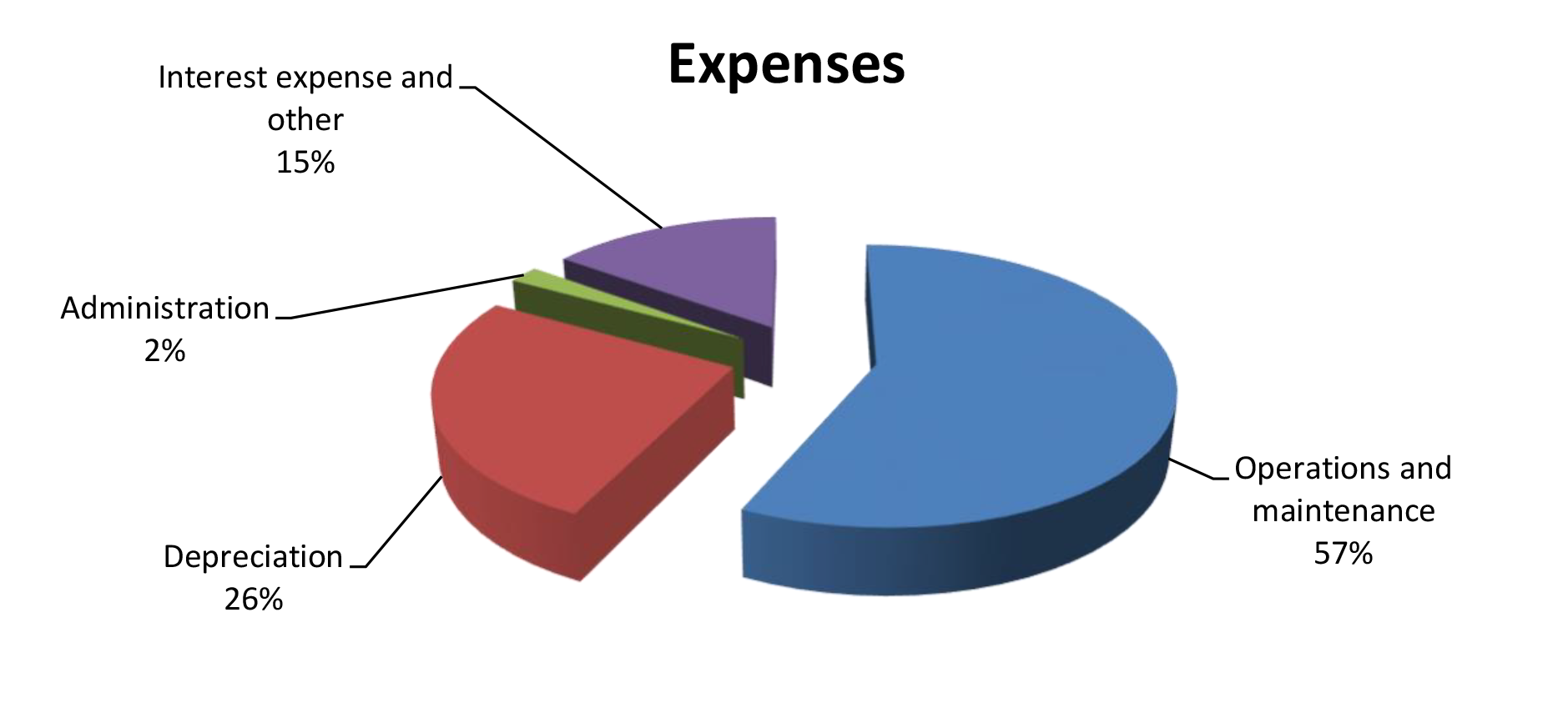

THE PRIMARY PURPOSE of the special-purpose audit was to form an opinion on the fairness of the presentation of the financial statements for the Hawai‘i Convention Center, as of and for the fiscal year ended June 30, 2024. The special-purpose financial statements have been prepared pursuant to the provisions of the management agreement between the Hawai‘i Tourism Authority and ASM Global (ASM), a private company contracted to operate the Hawai‘i Convention Center. The audit was conducted by Accuity LLP.

Financial Highlights

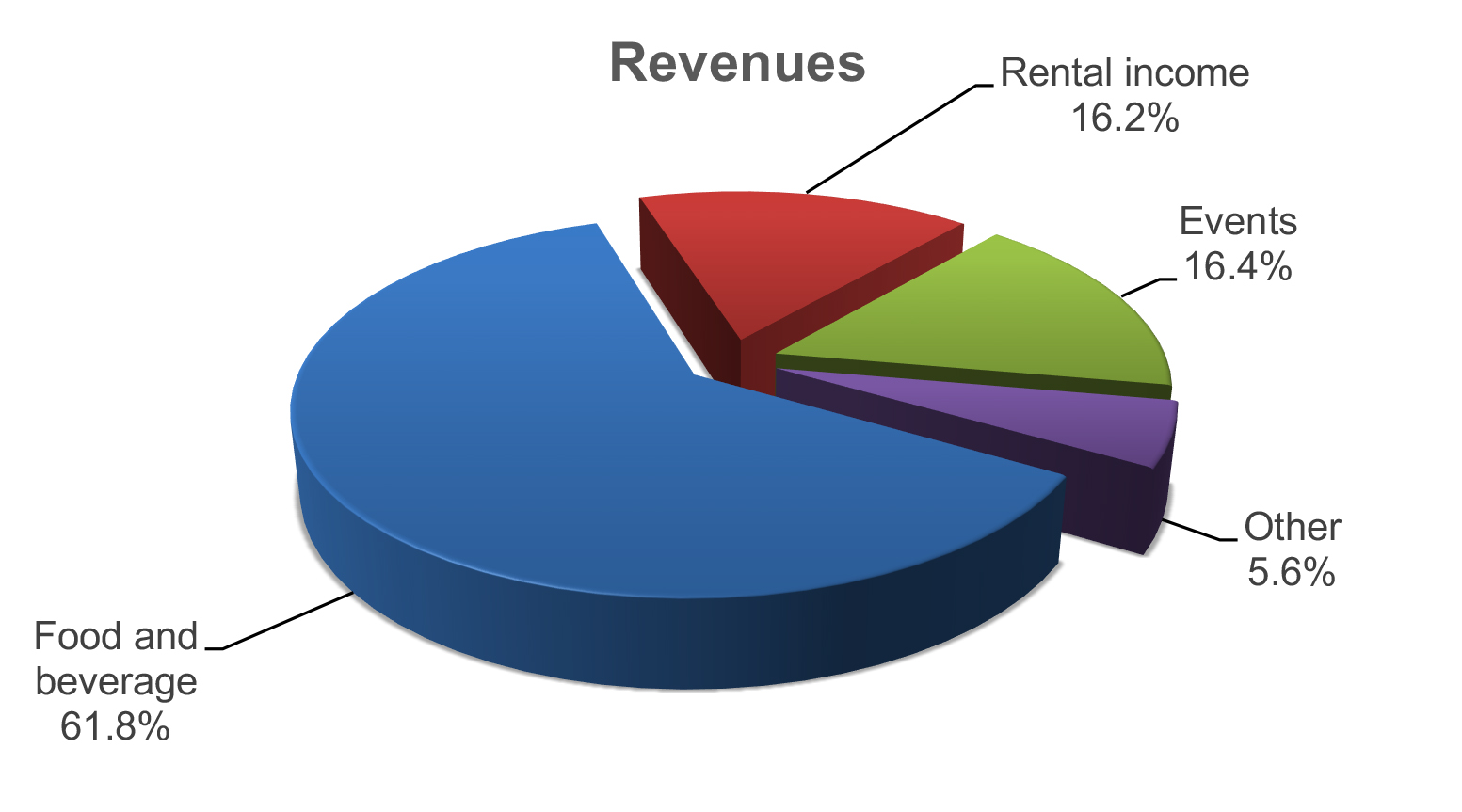

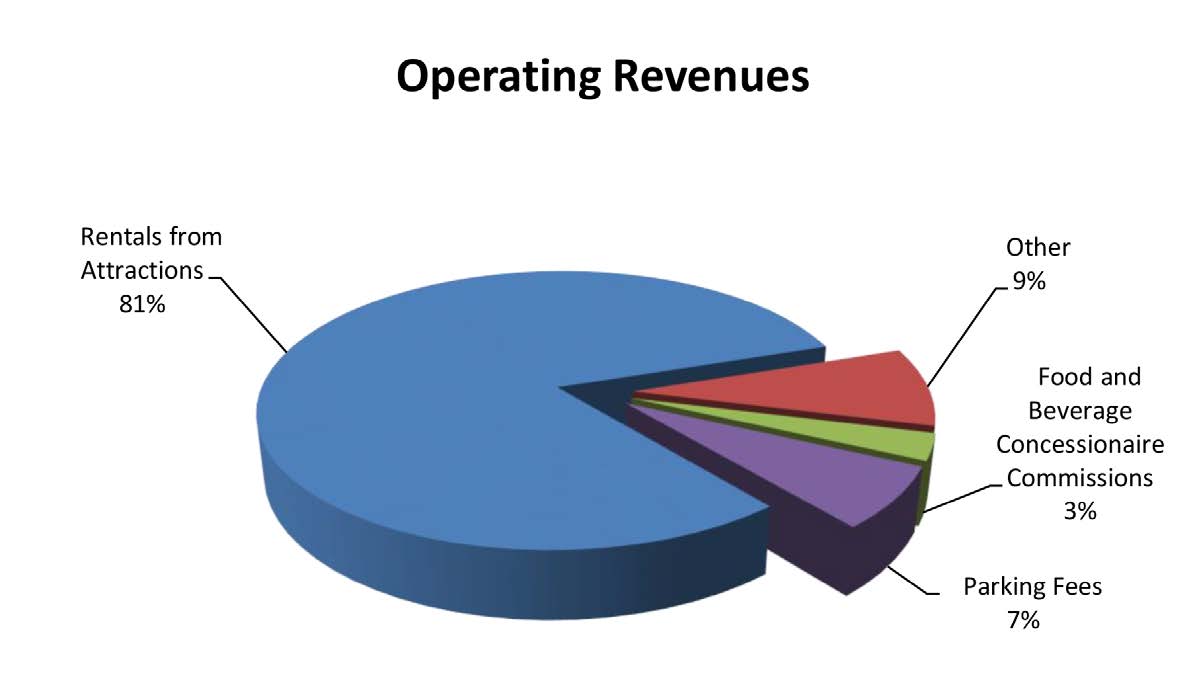

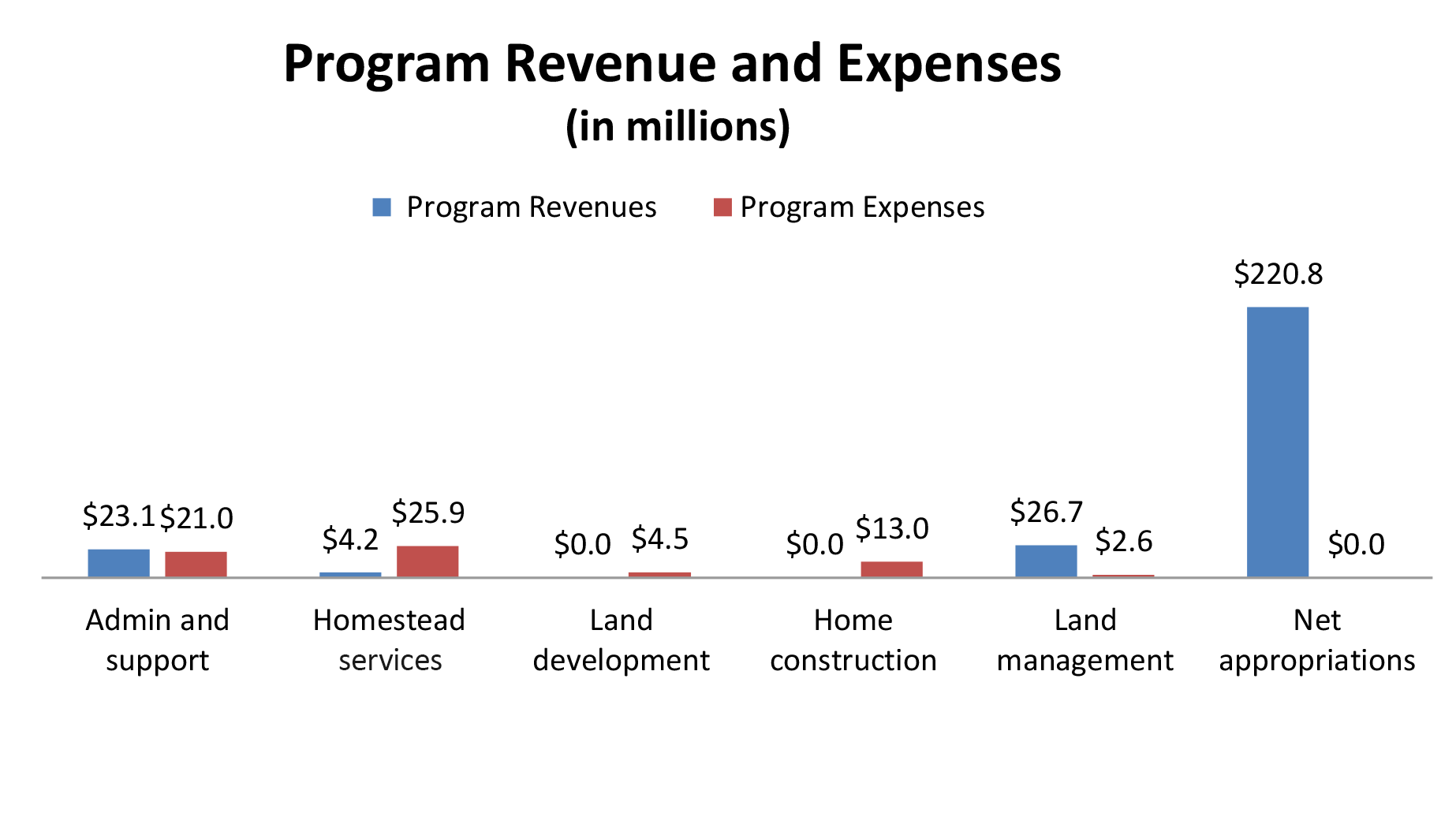

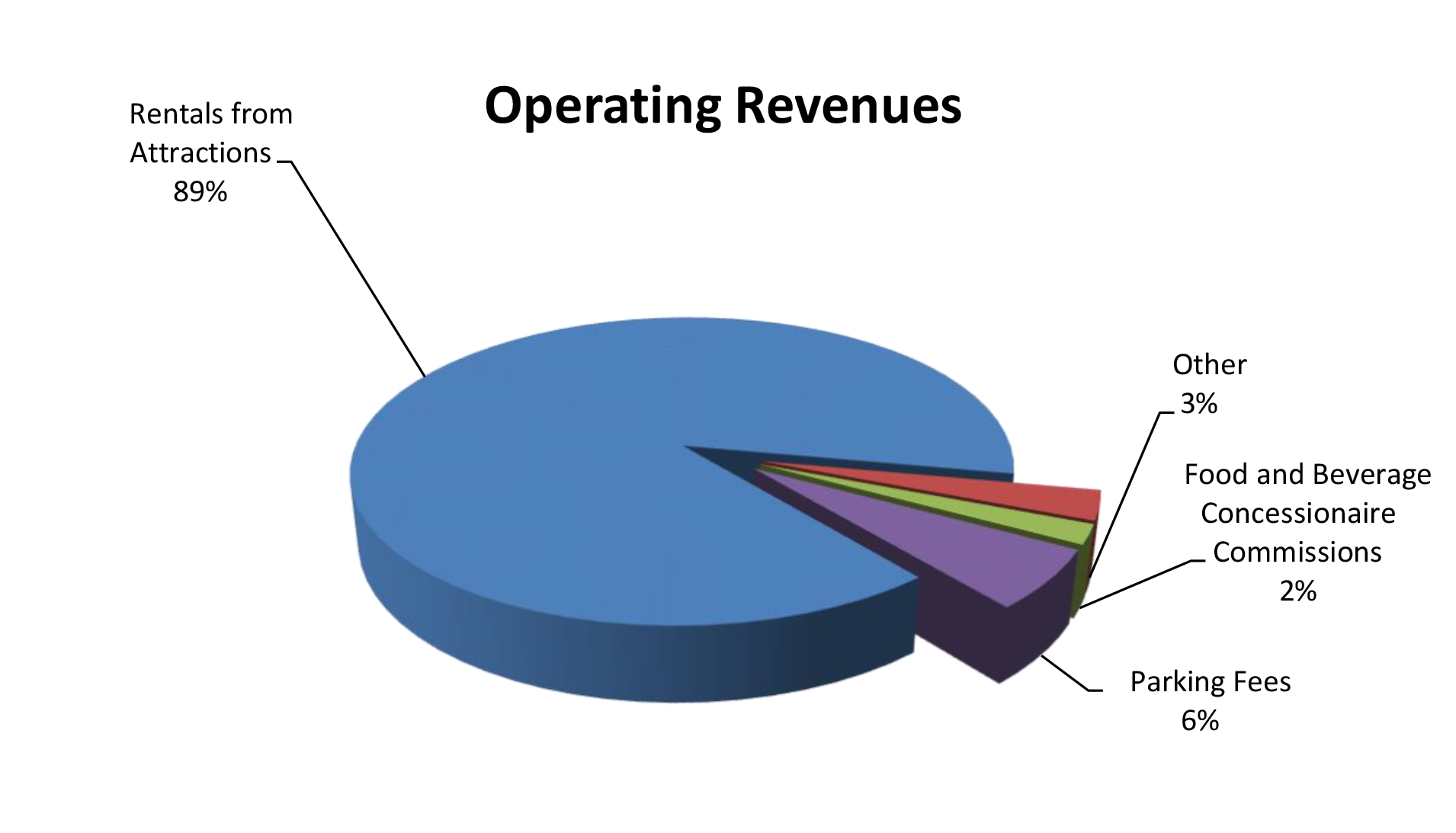

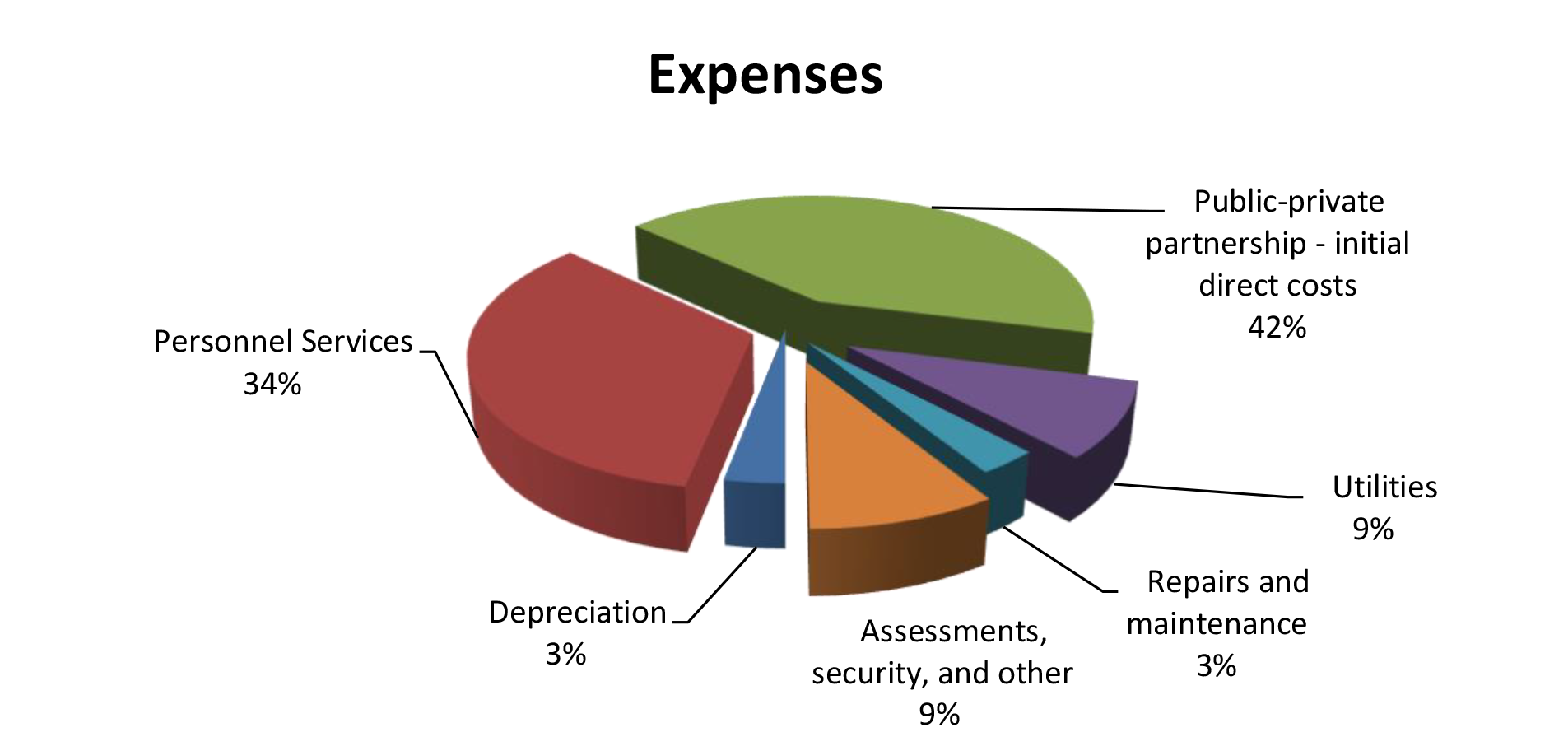

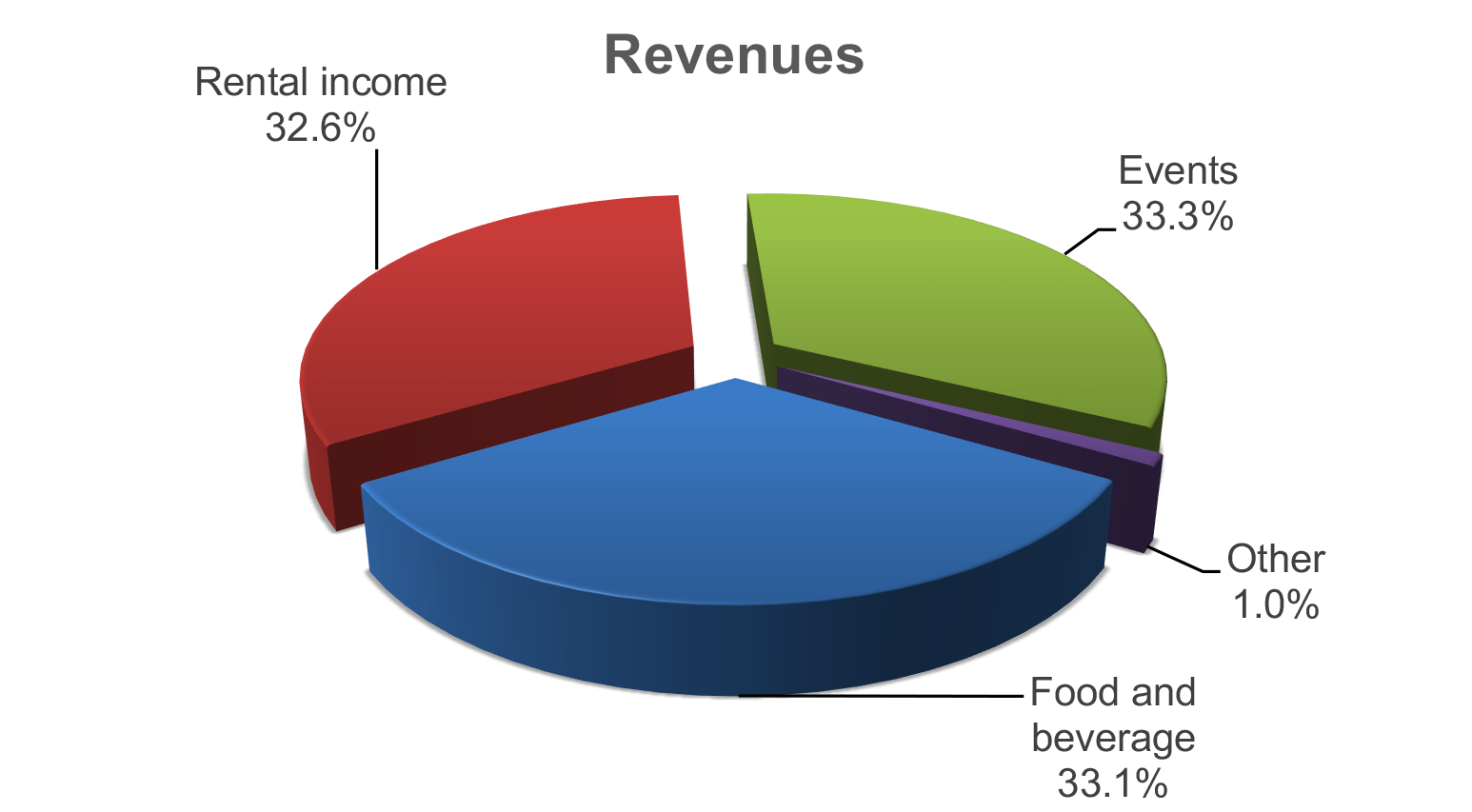

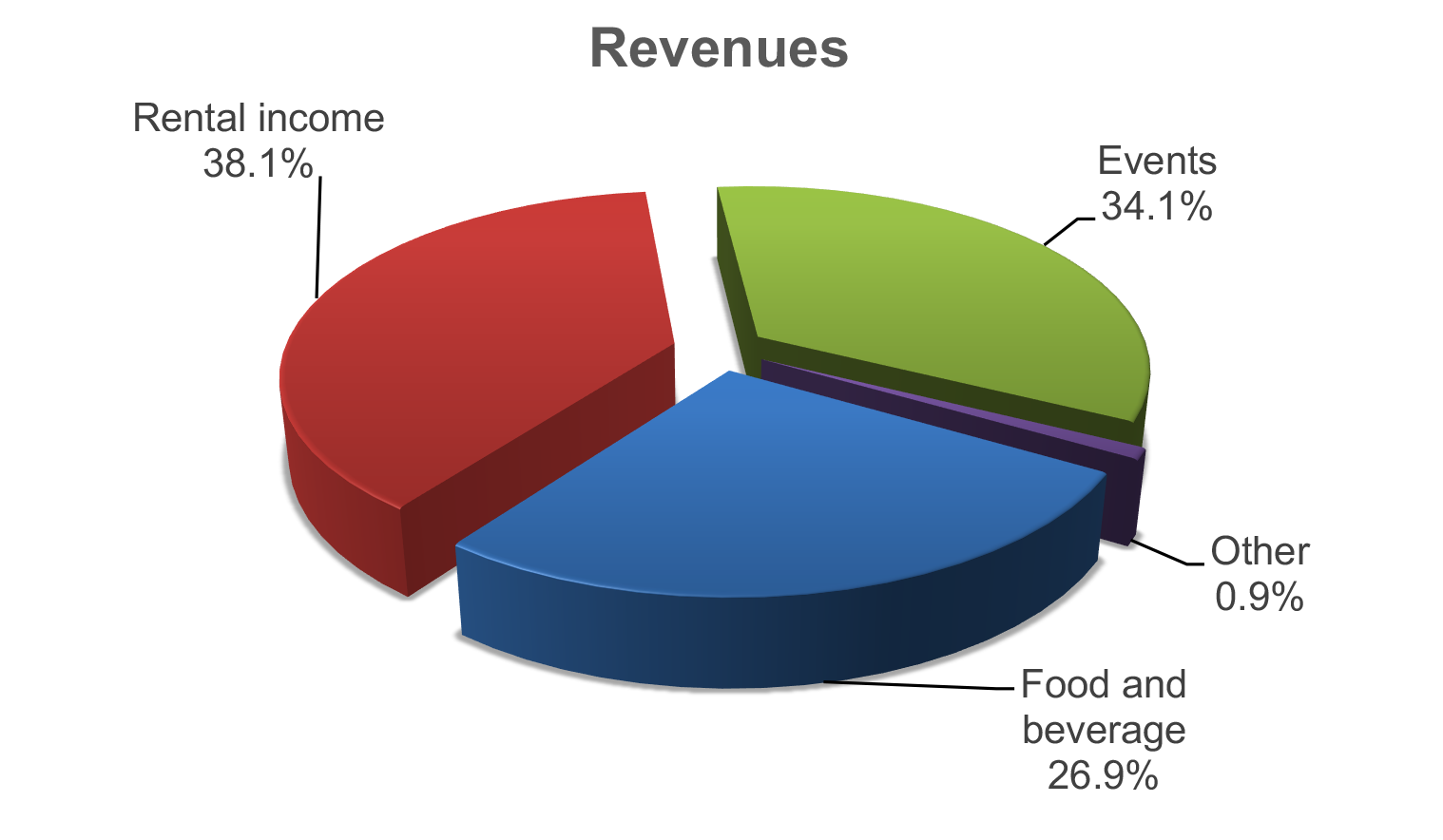

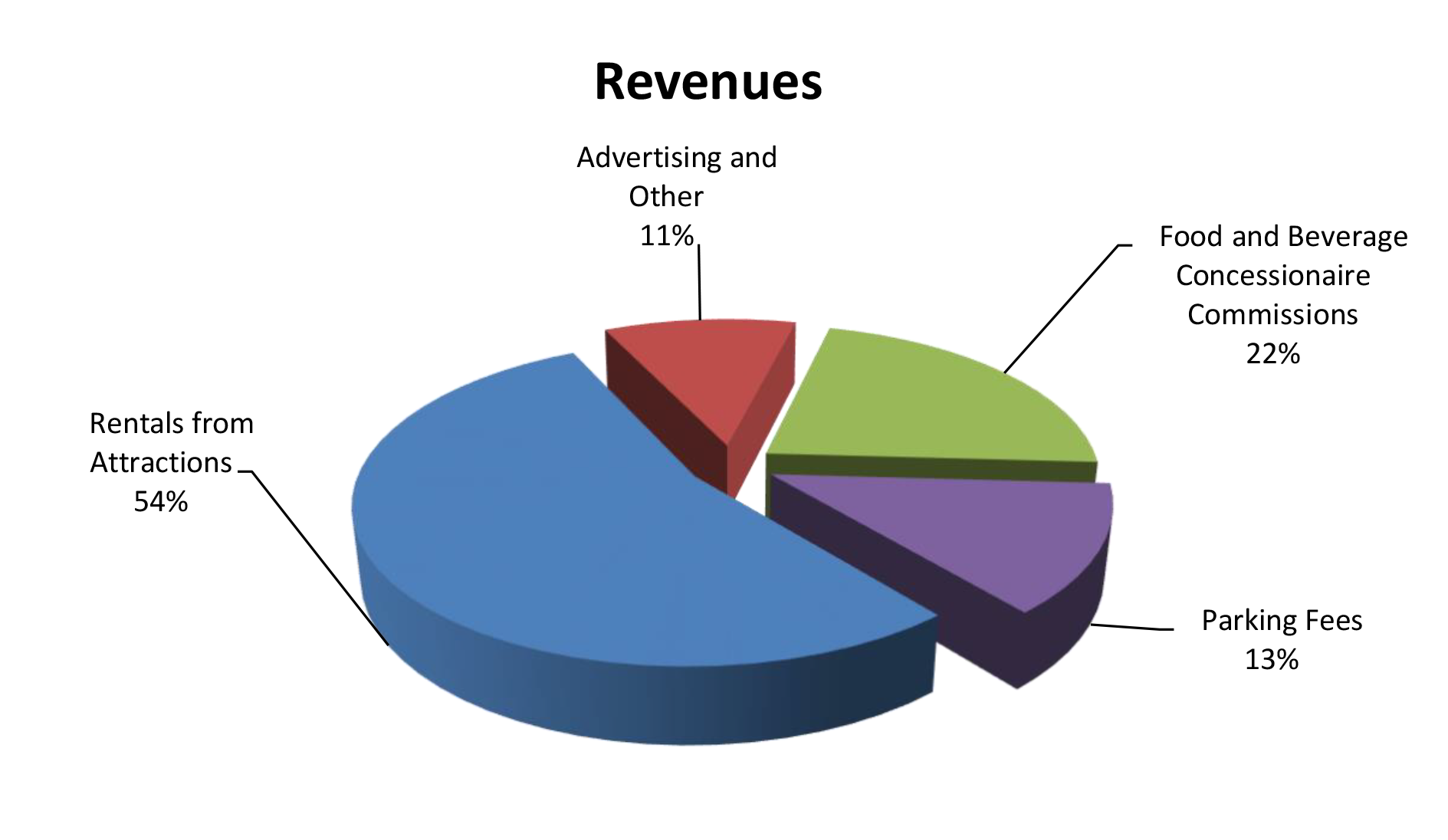

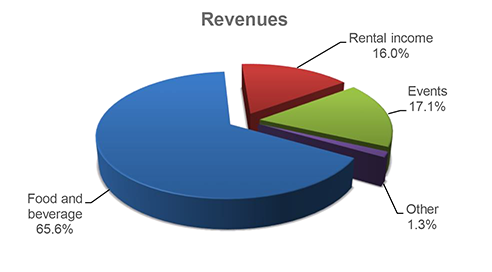

FOR THE FISCAL YEAR ENDED June 30, 2024, the Center reported total revenues of $28.9 million, total expenses of $26.2 million, and $12.3 million in net contributions from the Hawai‘i Tourism Authority, which resulted in a decrease in net assets of $600,000. Revenues consisted of (1) $17.9 million from food and beverage; (2) $4.7 million from rental income; (3) $4.7 million from events; and (4) $1.6 million from other revenues.

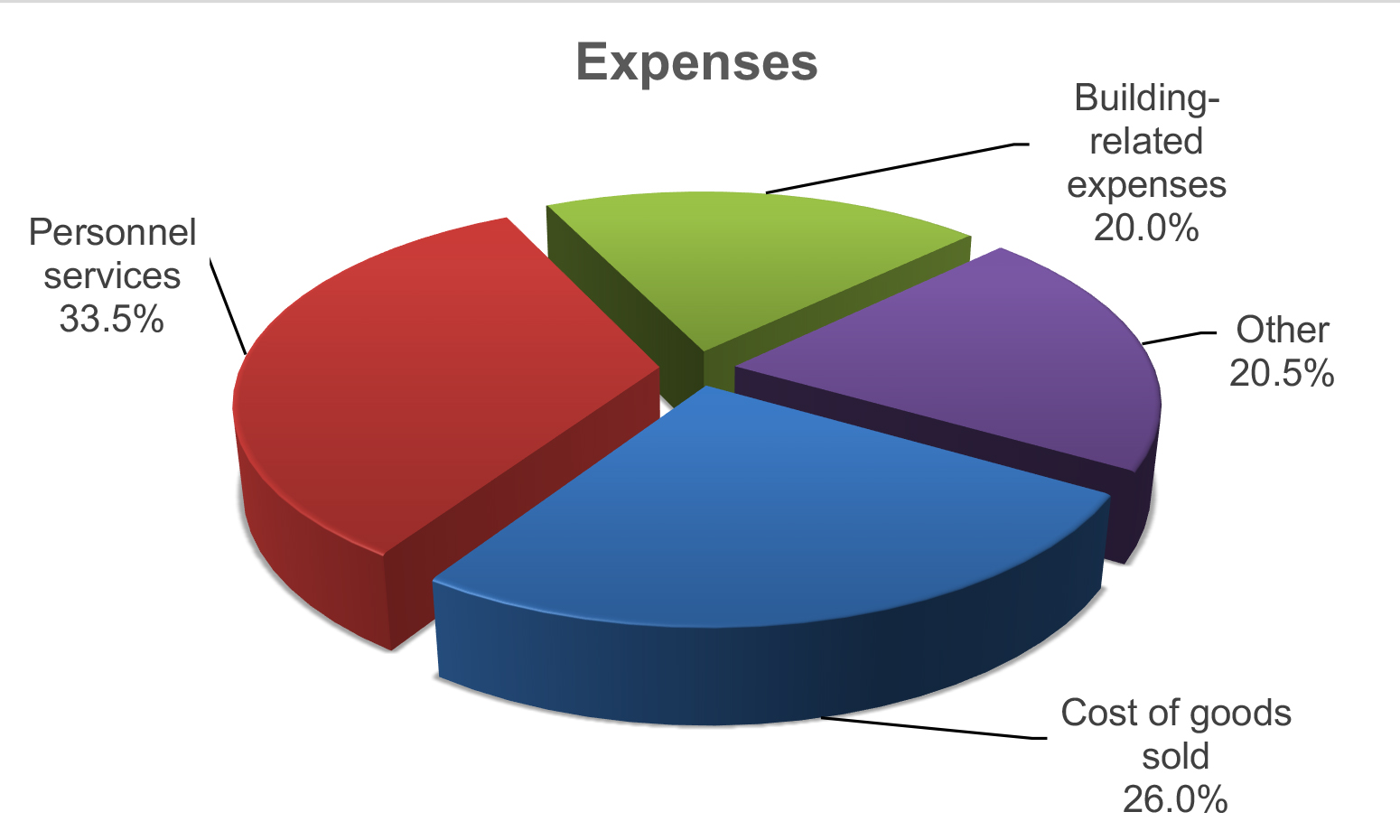

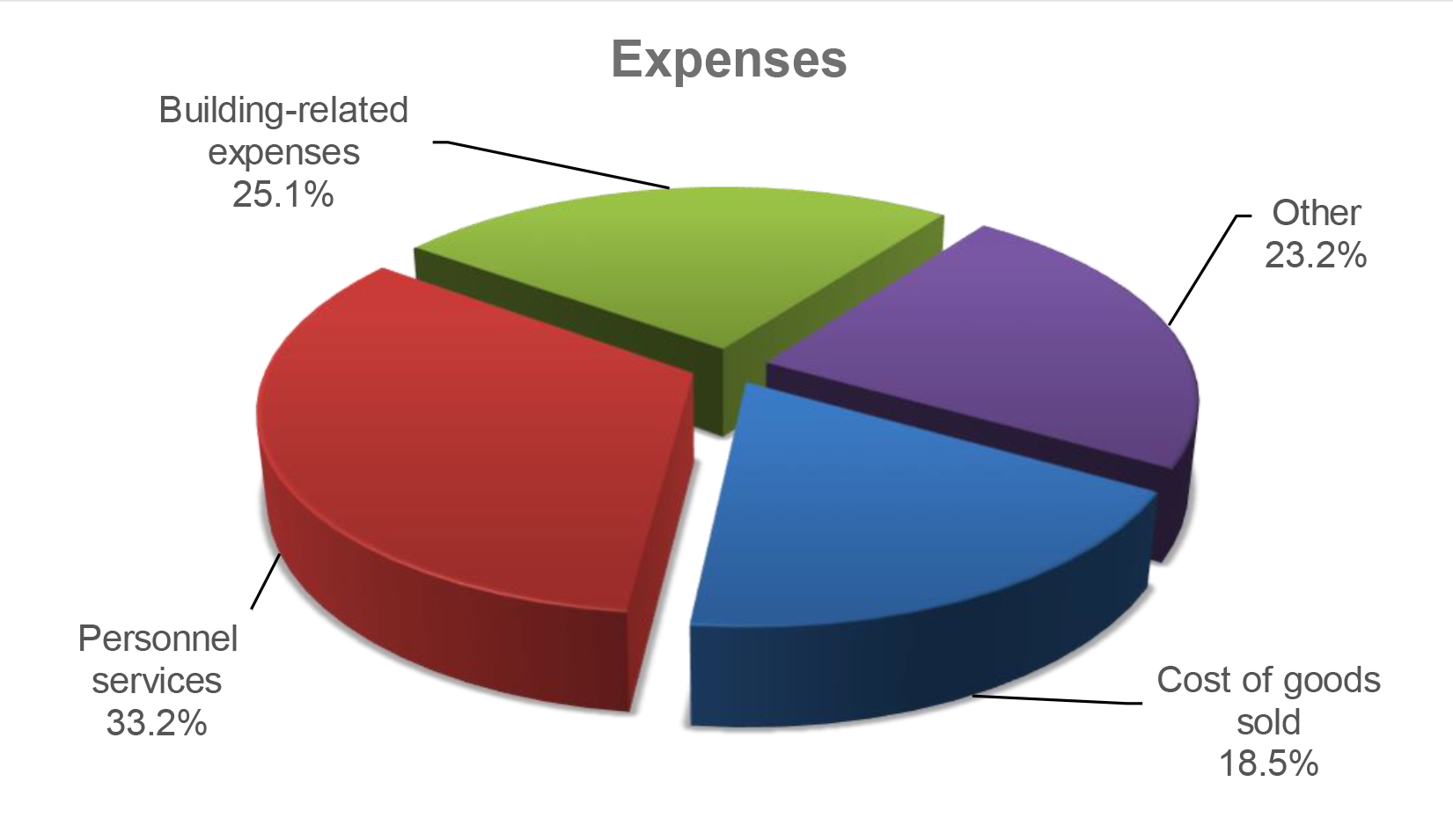

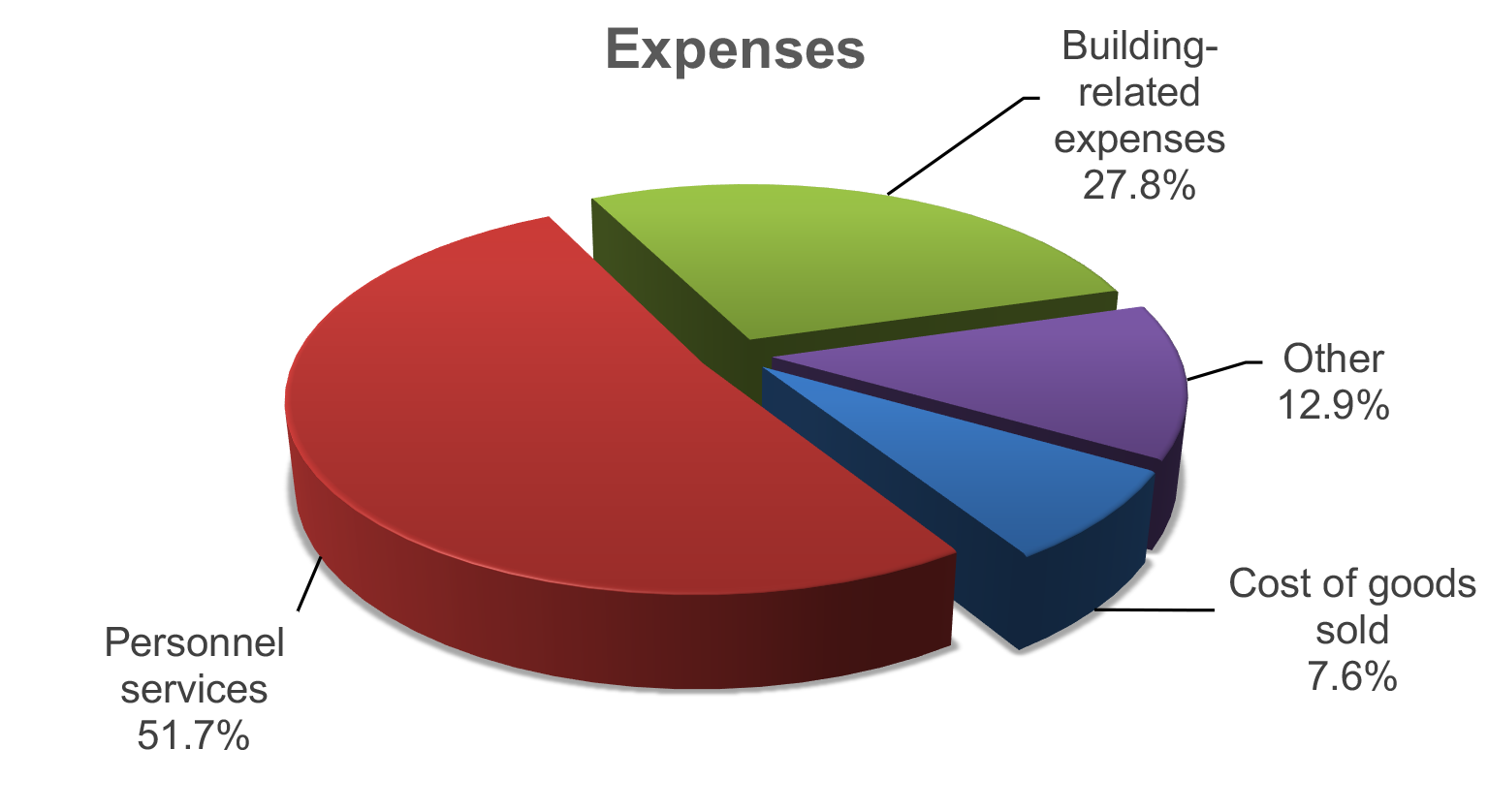

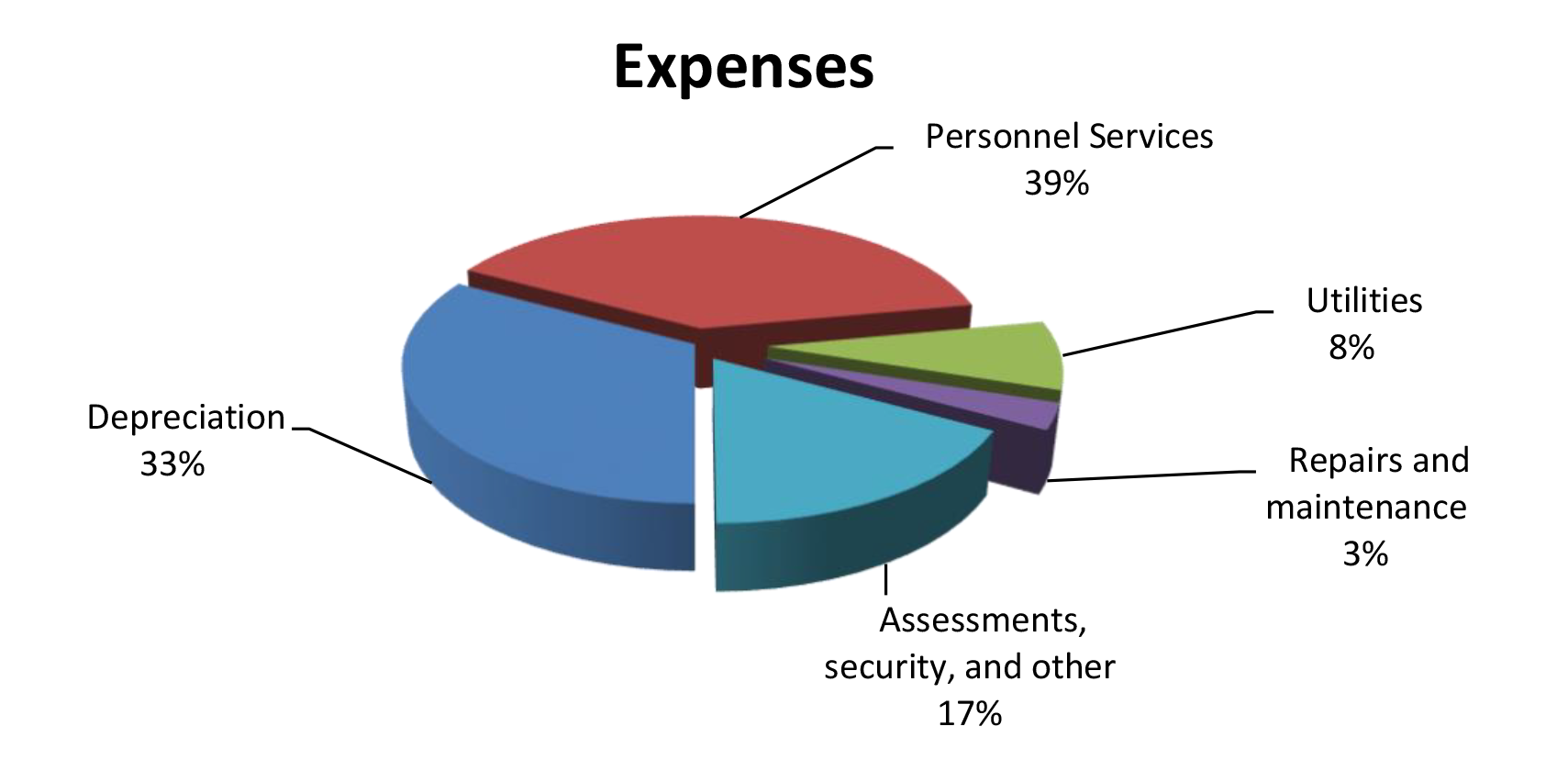

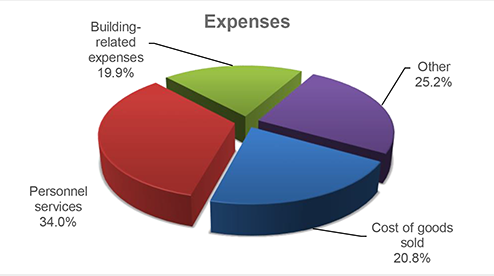

Expenses consisted of (1) $8.8 million for personnel services; (2) $5.2 million for building-related expenses; (3) $6.8 million for cost of goods sold; and (4) $5.4 million for other costs.

As of June 30, 2024, the Center’s total assets of $48.9 million were comprised of (1) cash of $38.7 million; (2) amounts due from Hawai‘i Tourism Authority of $6.1 million; (3) accounts receivable of $3.9 million; and (4) other assets of $200,000. Total liabilities of $9.7 million were comprised of (1) accounts payable of $8.4 million; (2) advance deposits of $800,000; and (3) other liabilities of $500,000.

Property, building, furniture, and equipment used in the Center’s operations, and related depreciation expense, as well as debt used to finance such capital assets and the related interest expense, are not reflected in the Center’s special-purpose financial statements. Those assets, liabilities, and related expenses are reflected on the financial statements of the Hawai‘i Tourism Authority.

Auditors’ Opinion THE CENTER RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with the management agreement between the Hawai‘i Tourism Authority and ASM, which is a basis of accounting other than accounting principles generally accepted in the United States of America.

About the Center

The Hawai‘i Convention Center (Center), which opened to the general public in June 1998, is used for a variety of events, including conventions and trade shows, public shows, and spectator events. The Center offers approximately 350,000 square feet of rentable space, including 51 meeting rooms. The Hawai‘i Tourism Authority assumed responsibility for the operation, management, and maintenance of the Center in July 2000. The Center is reported as a special revenue fund of the Hawai‘i Tourism Authority.

Financial Statements, Fiscal Year Ended June 30, 2024

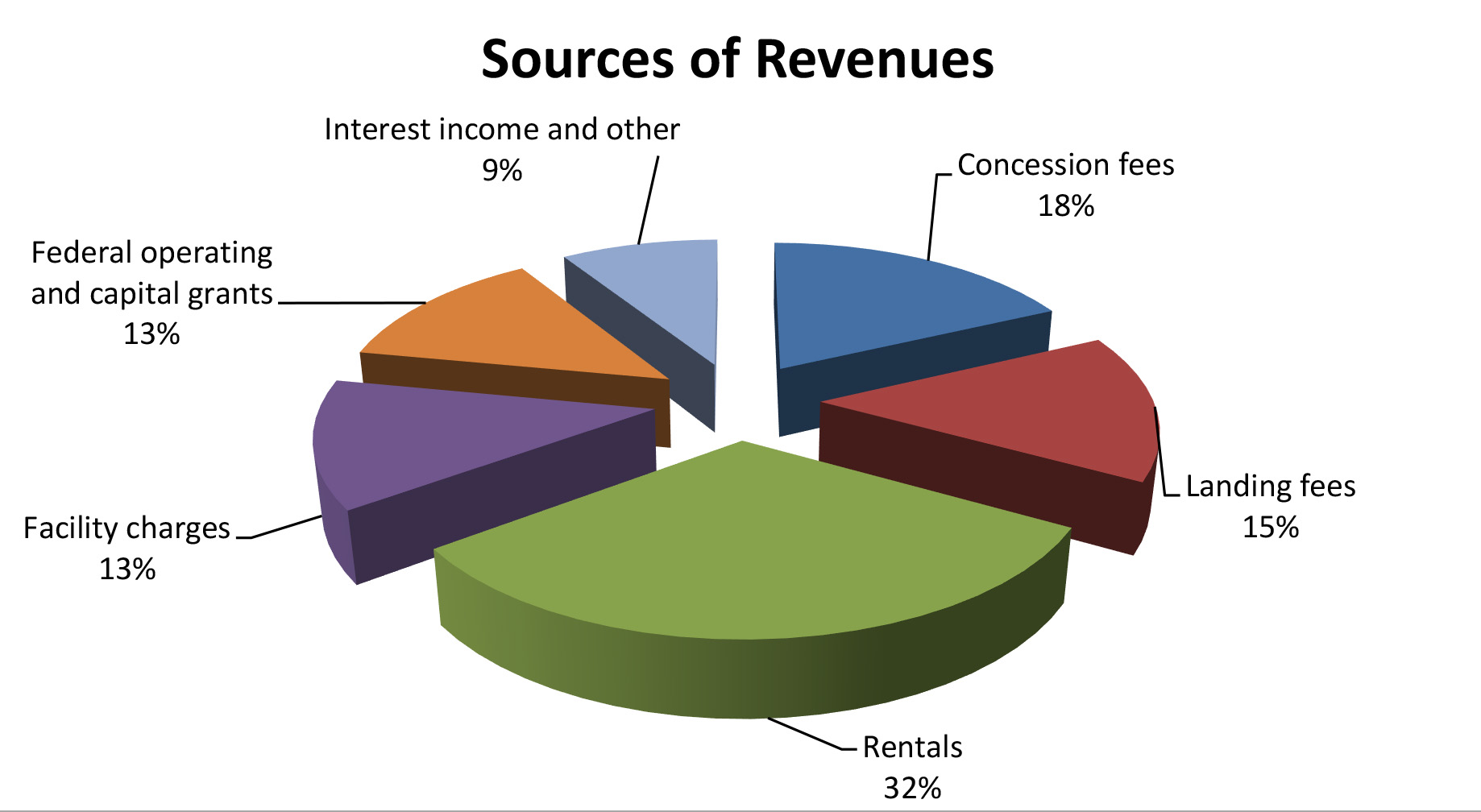

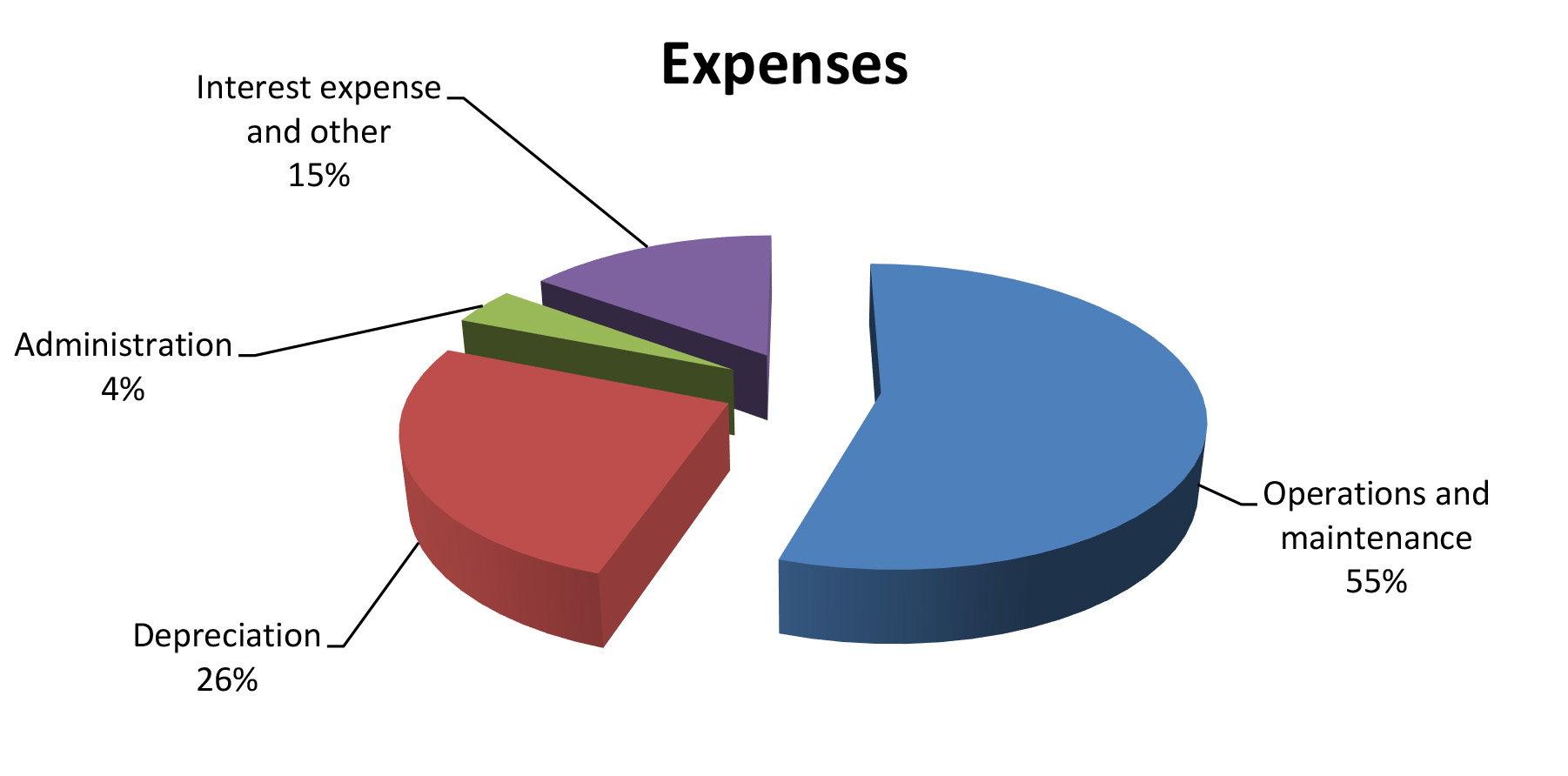

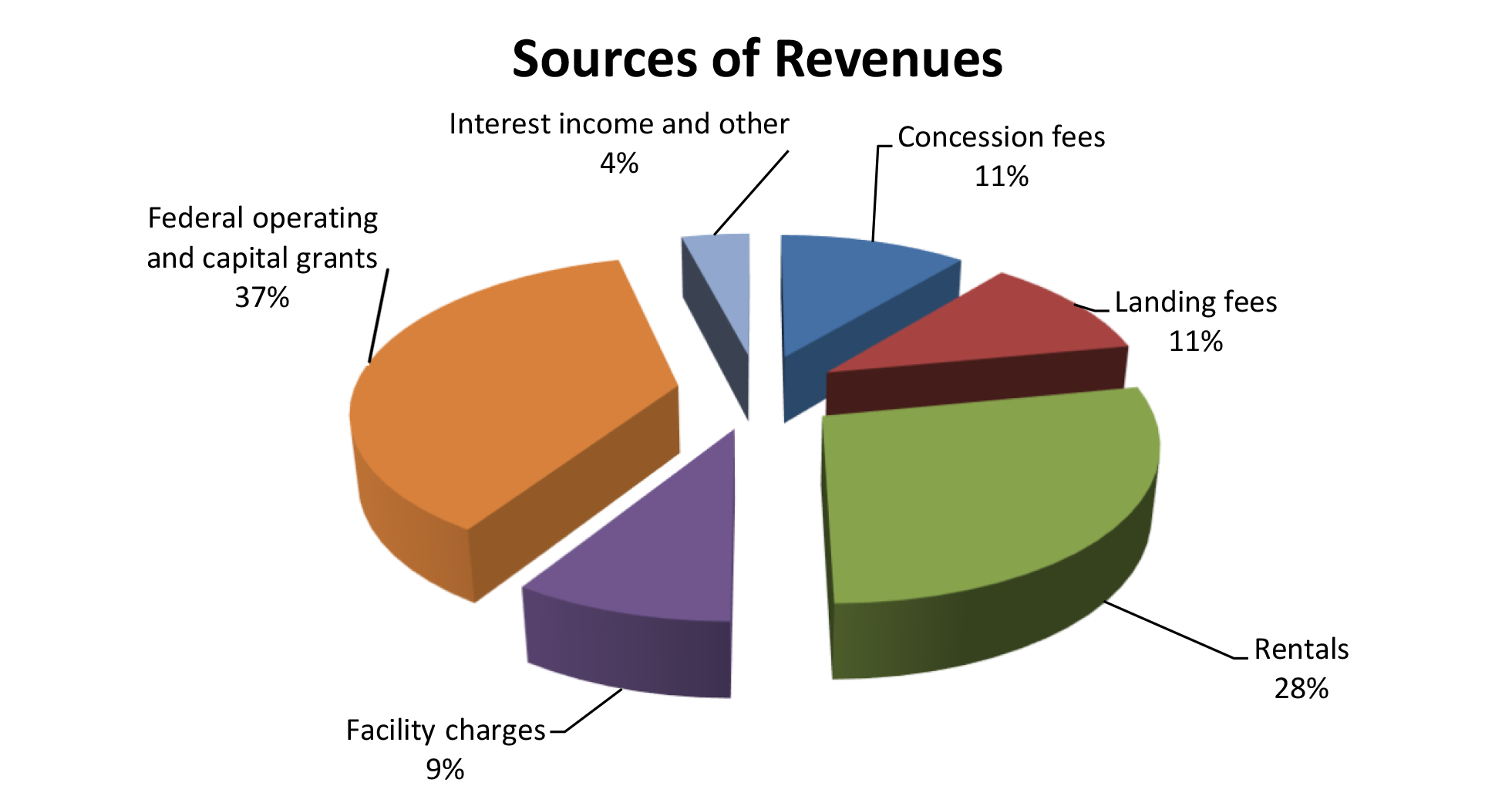

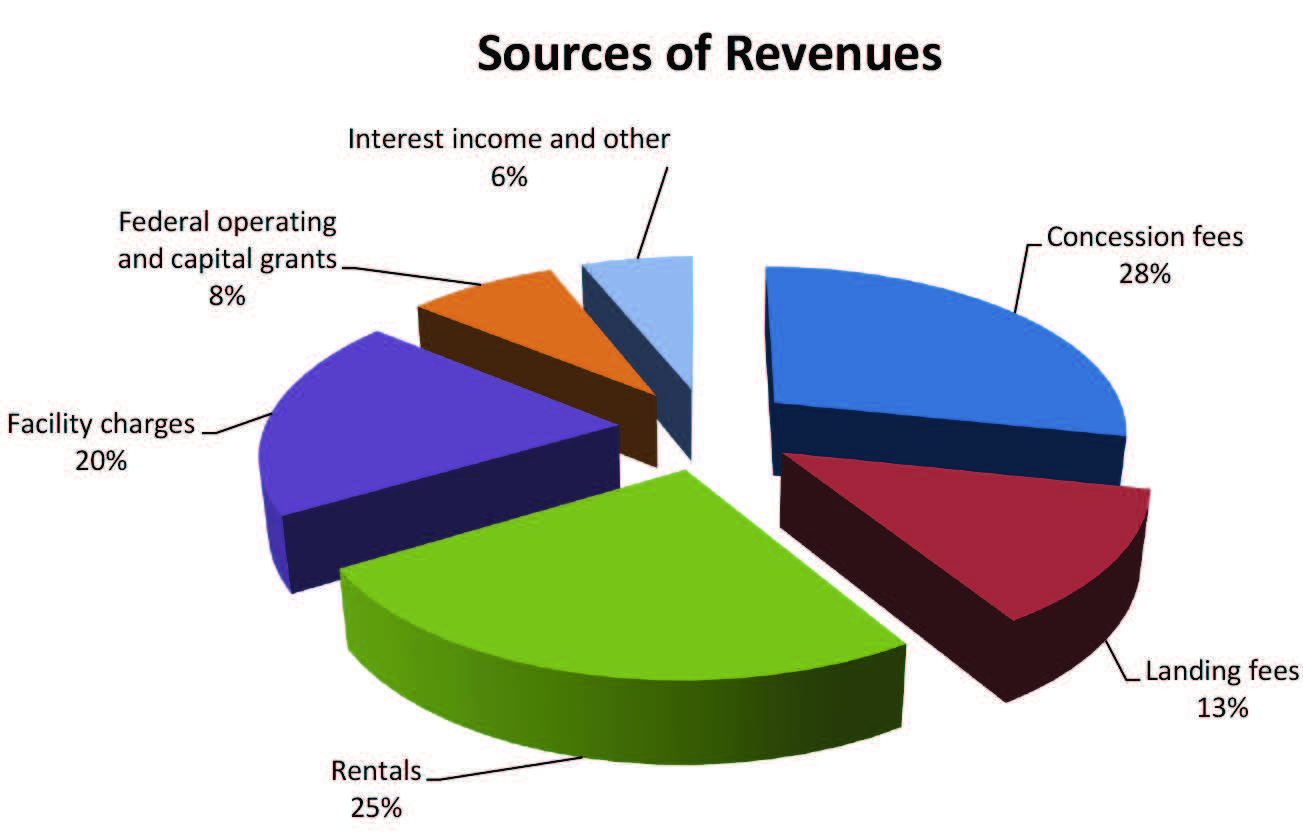

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the Hawai‘i Tourism Authority, as of and for the fiscal year ended June 30, 2024, and to comply with the requirements of Title 2, U.S. Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by Accuity LLP.

Financial Highlights

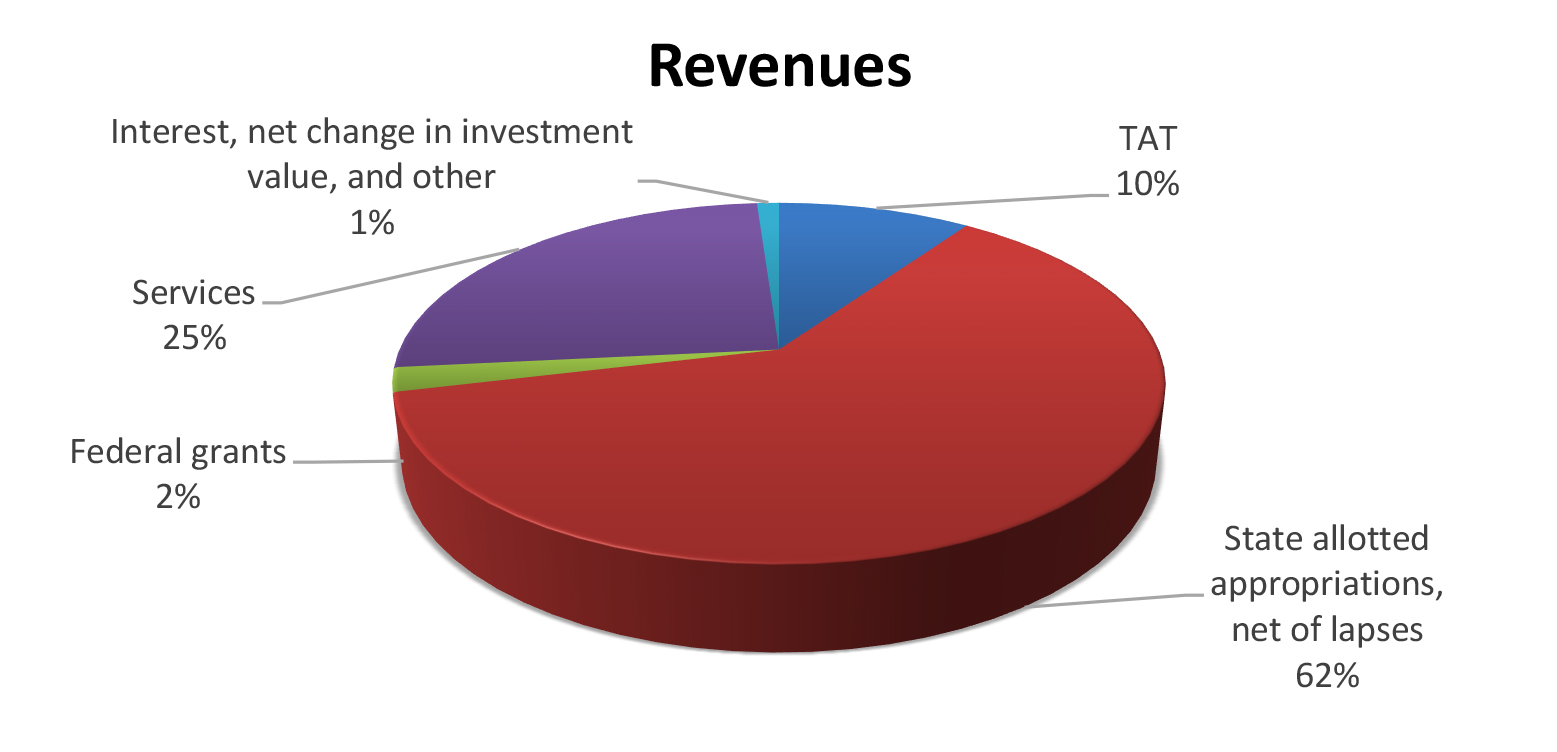

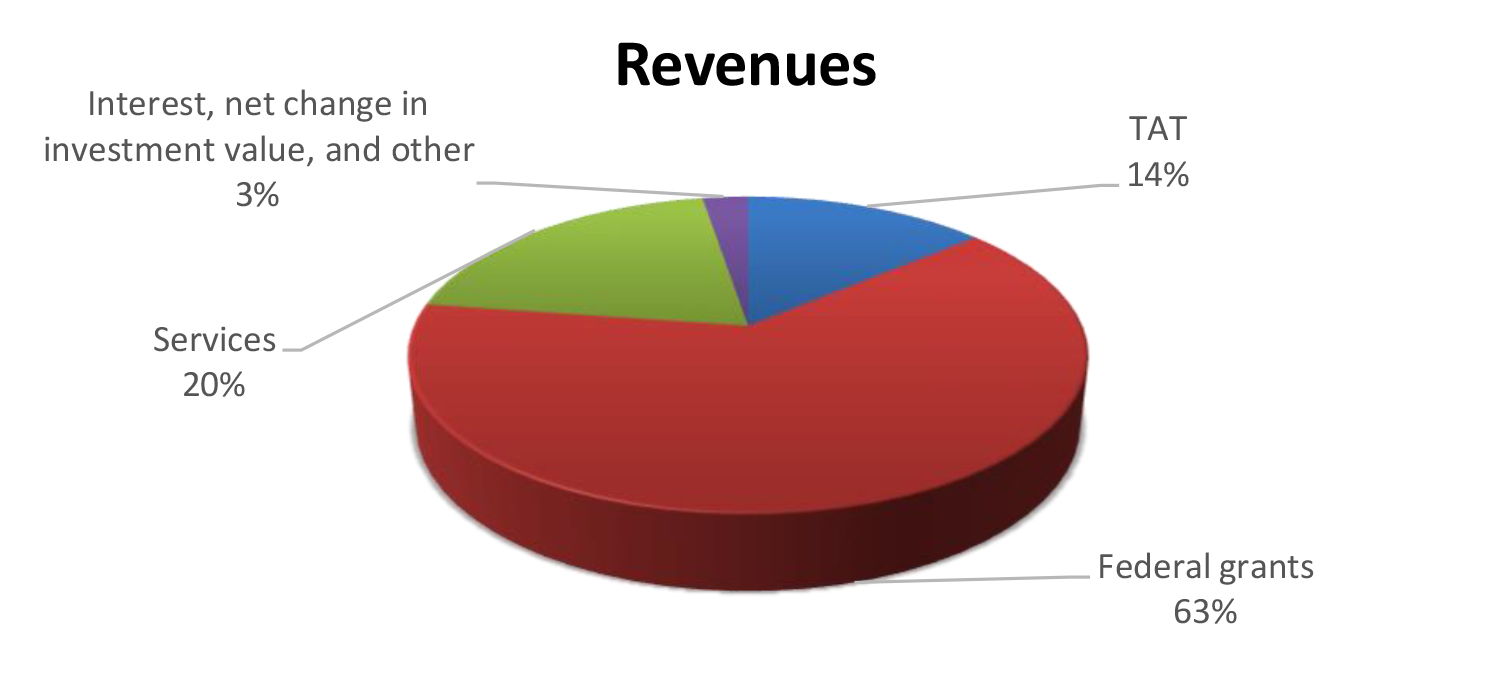

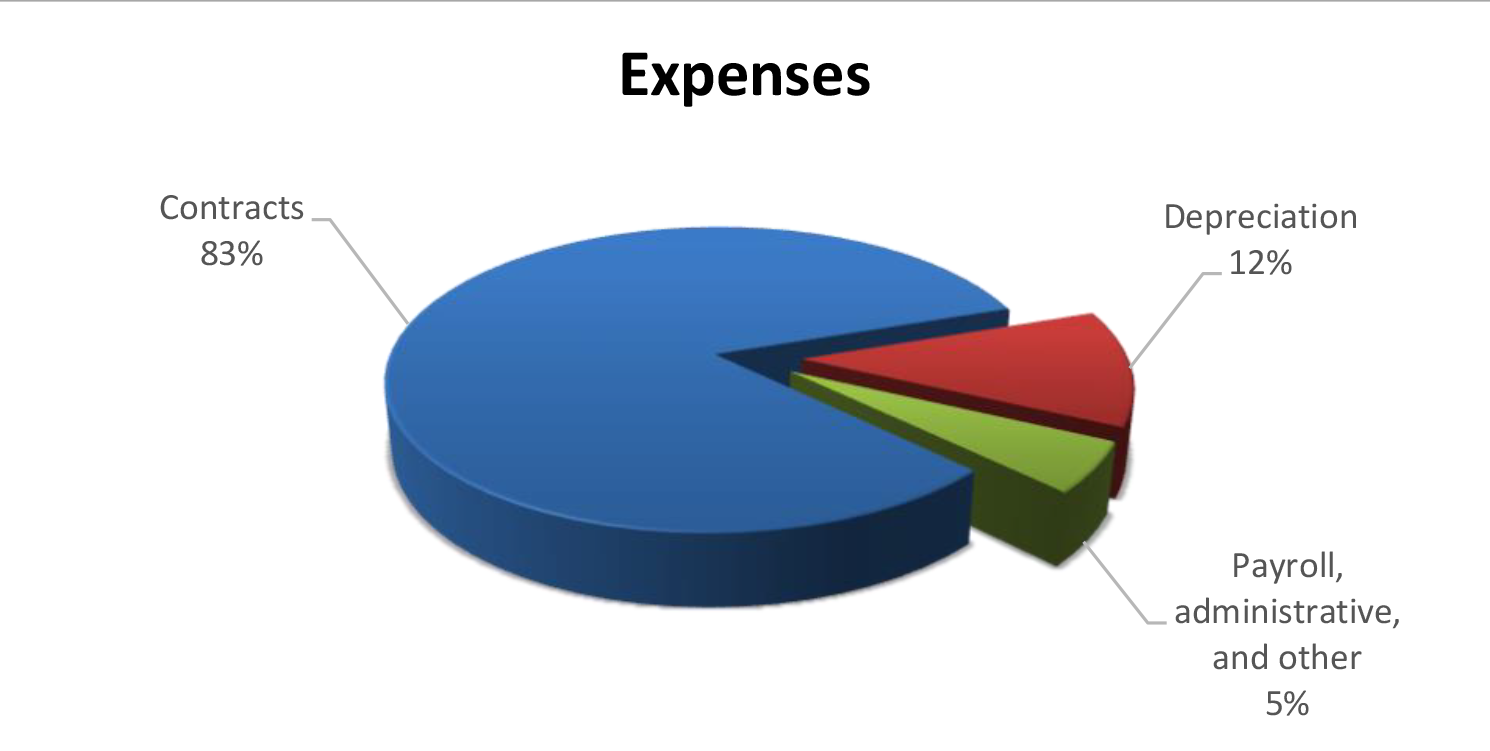

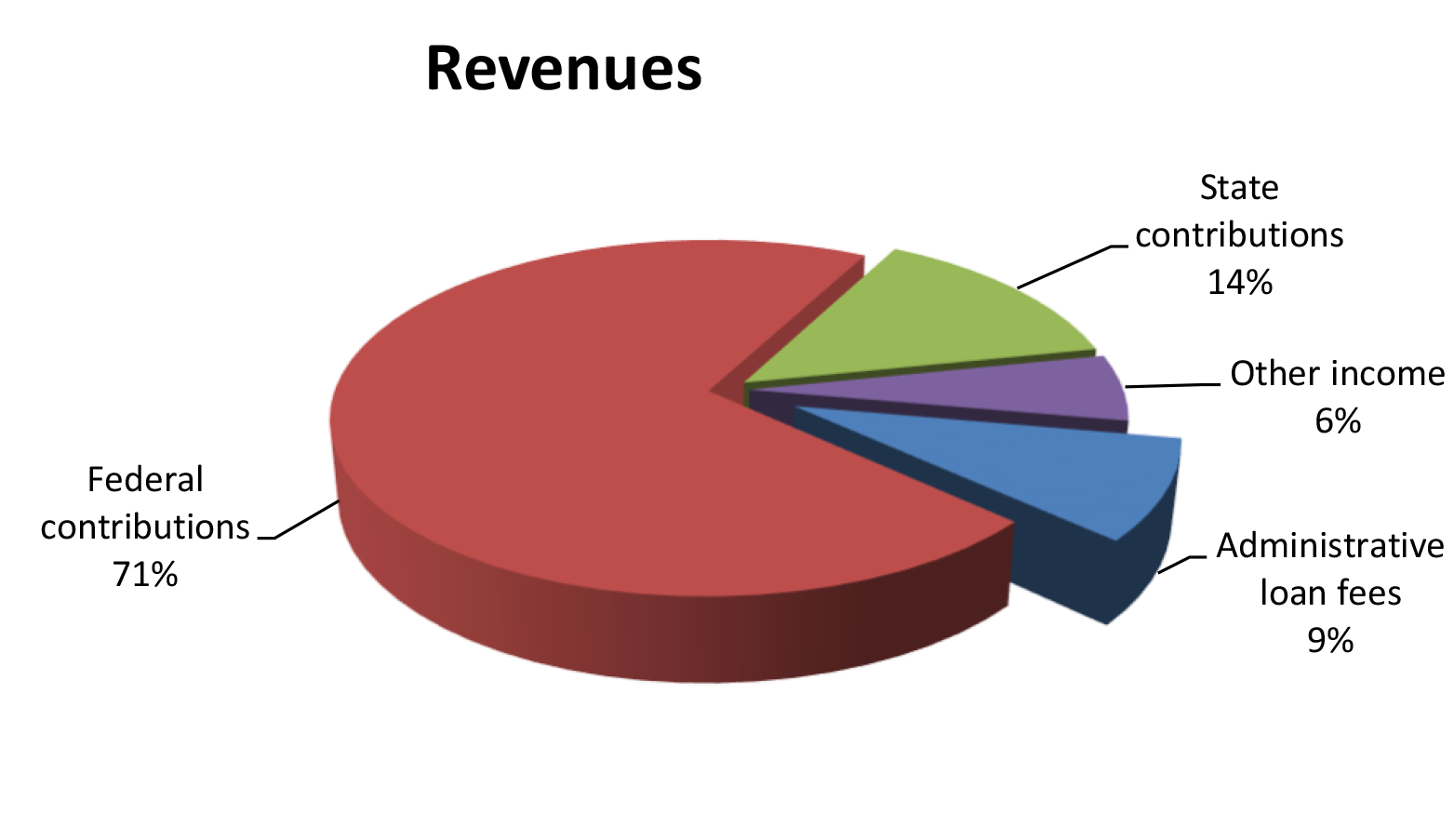

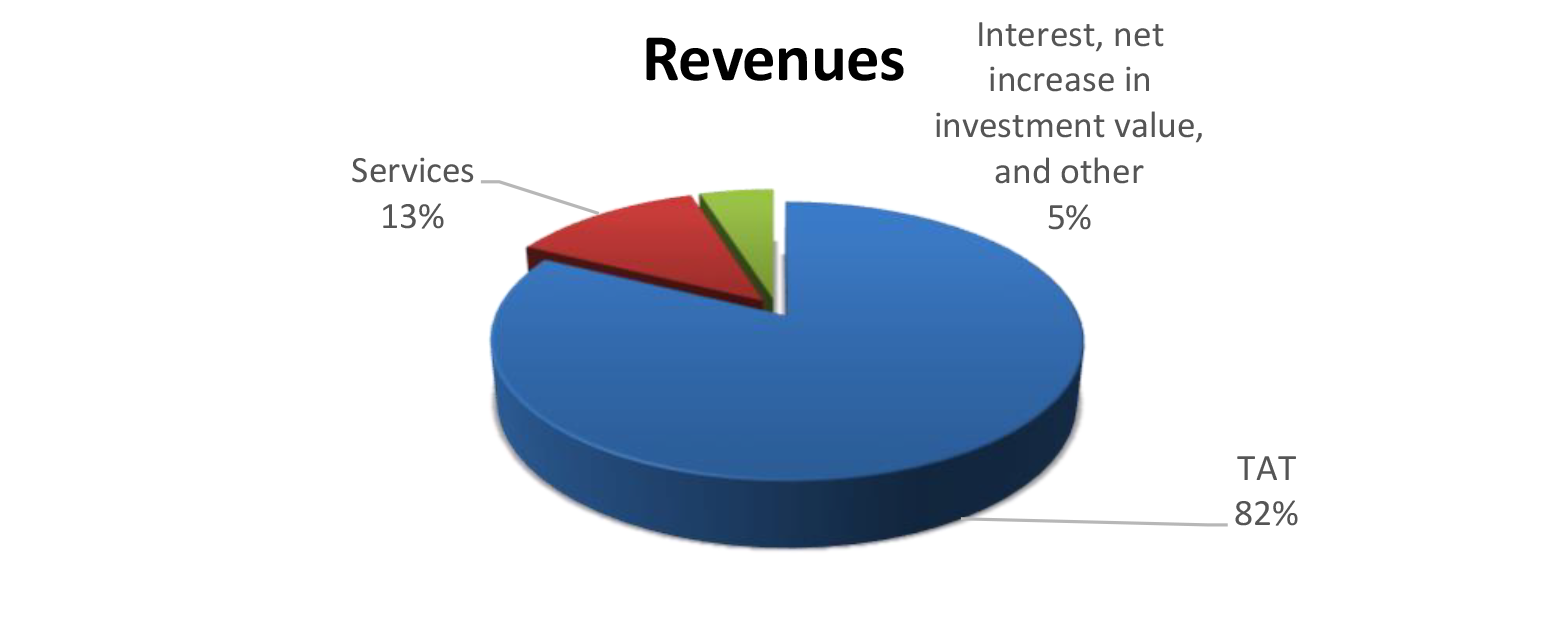

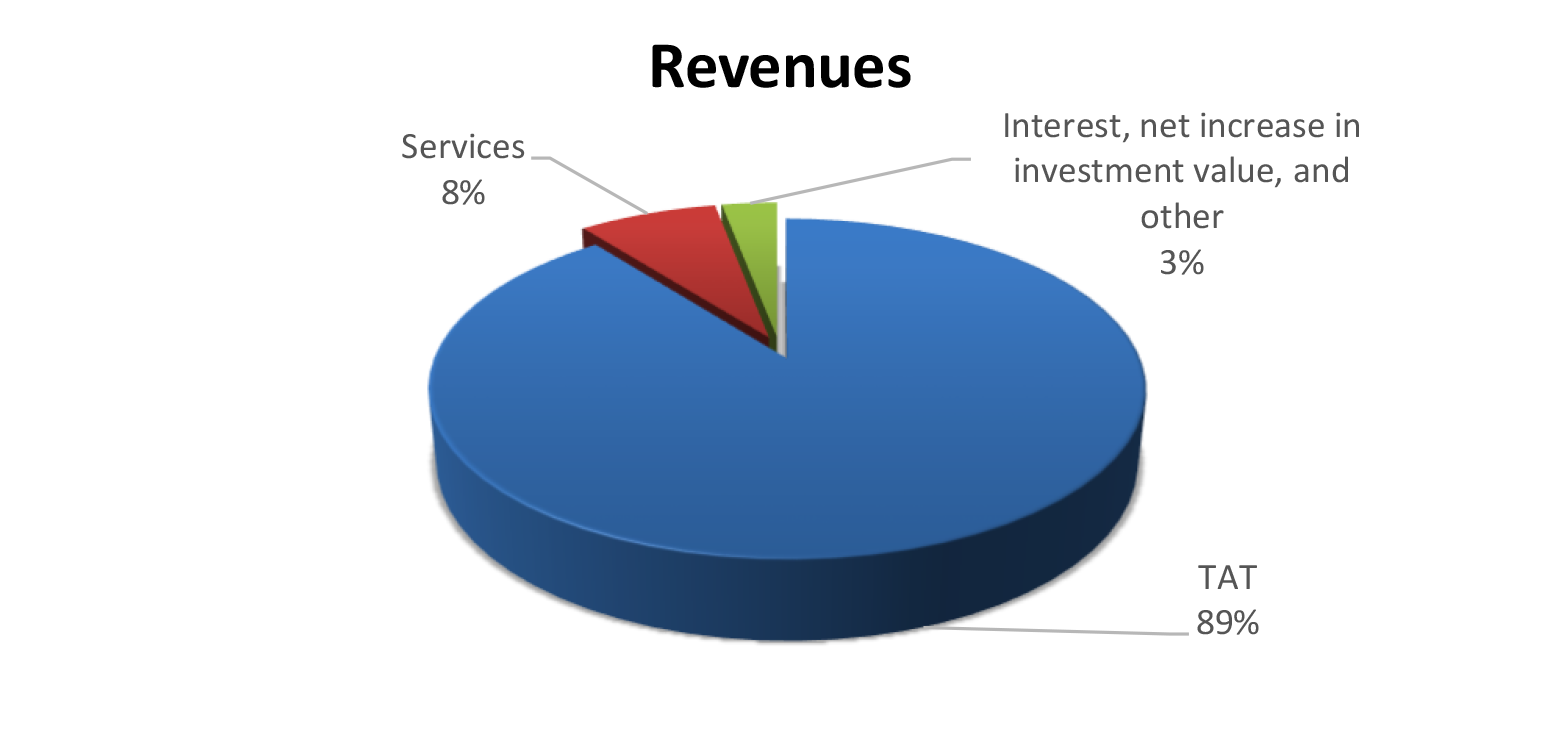

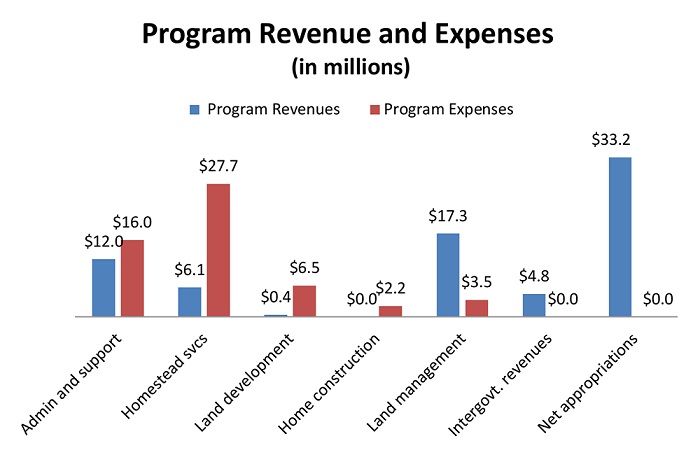

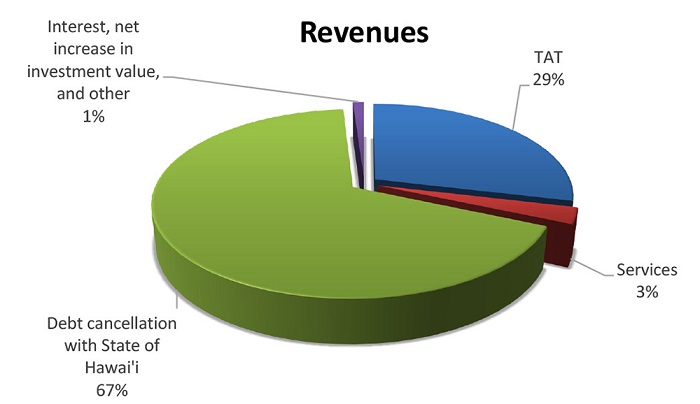

FOR THE FISCAL YEAR ended June 30, 2024, HTA reported total revenues of $113.9 million, along with $5 million in transfers from other state departments, and total expenses of $114.8 million. Revenues consisted of $70.1 million from state allotted appropriations, net of lapses; $2.5 million from federal grants; $11 million from TAT; $29 million from charges for services; and $1.3 million from interest and other revenues.

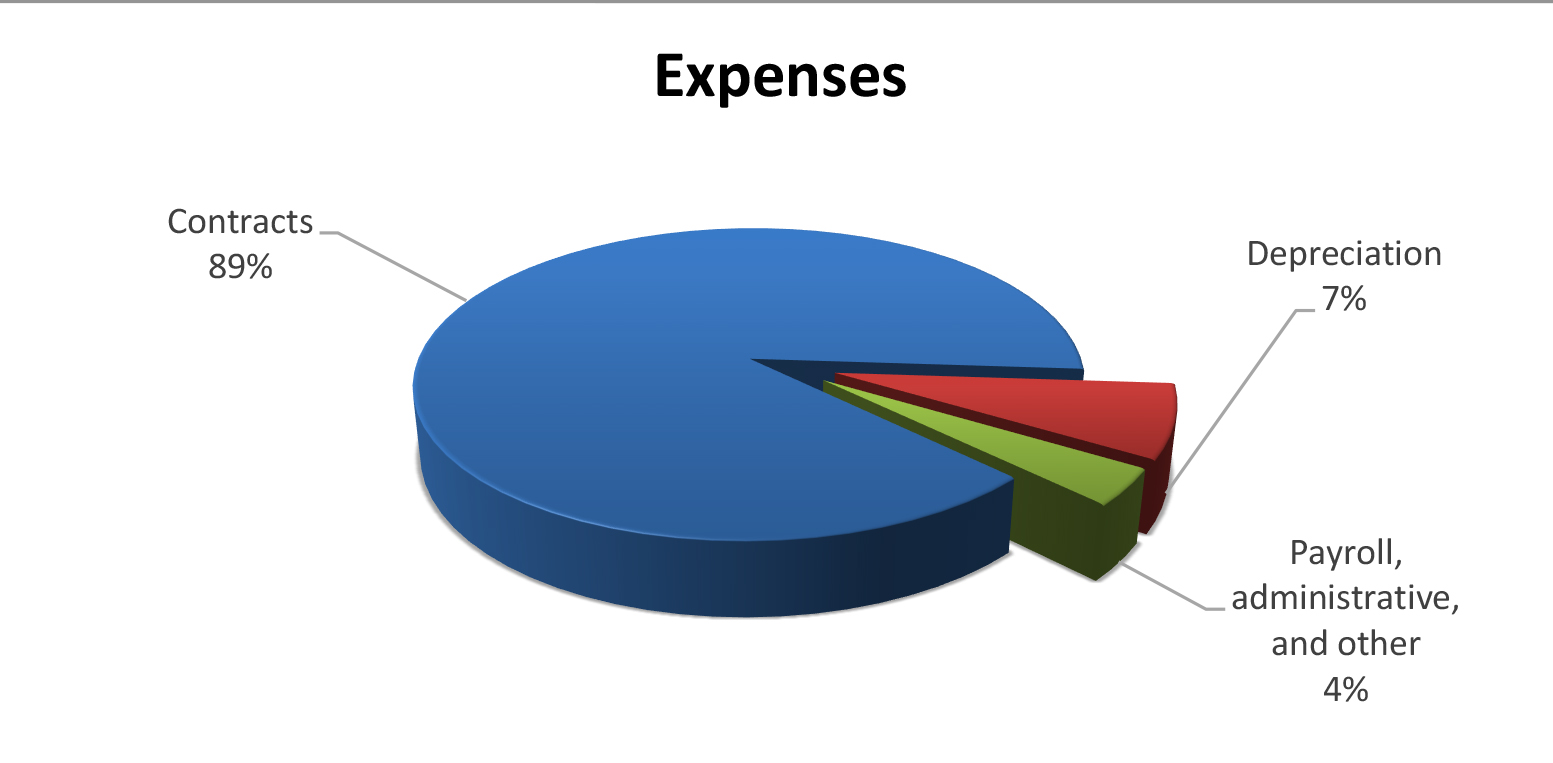

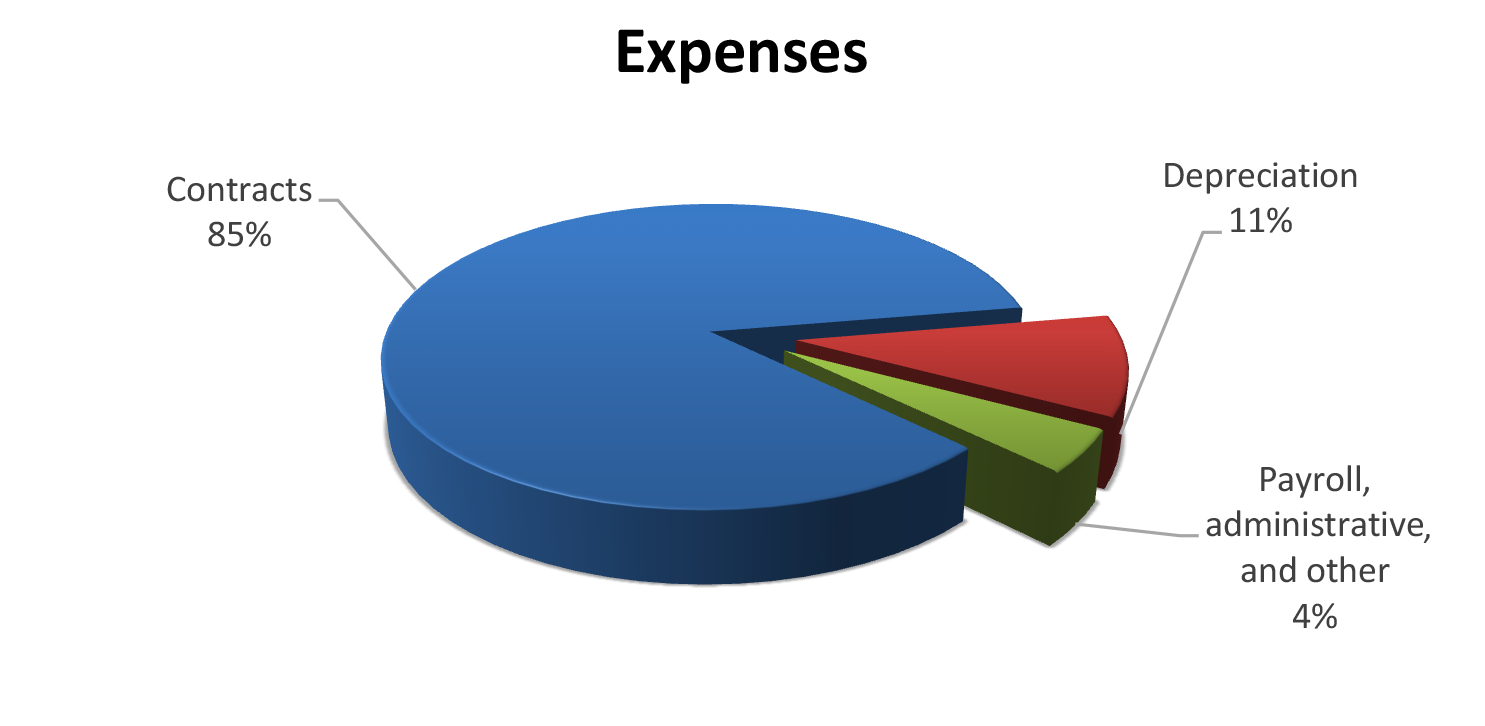

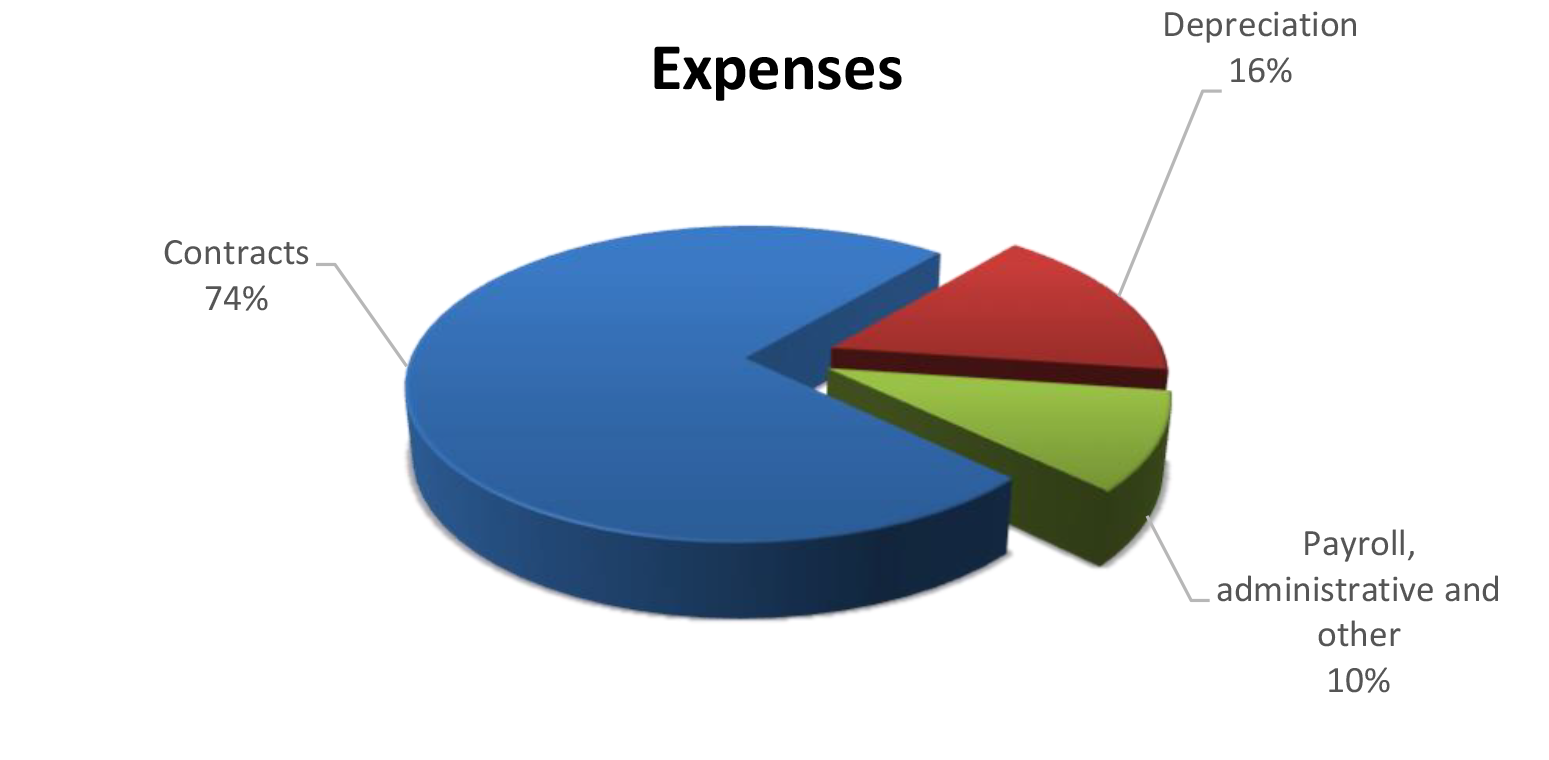

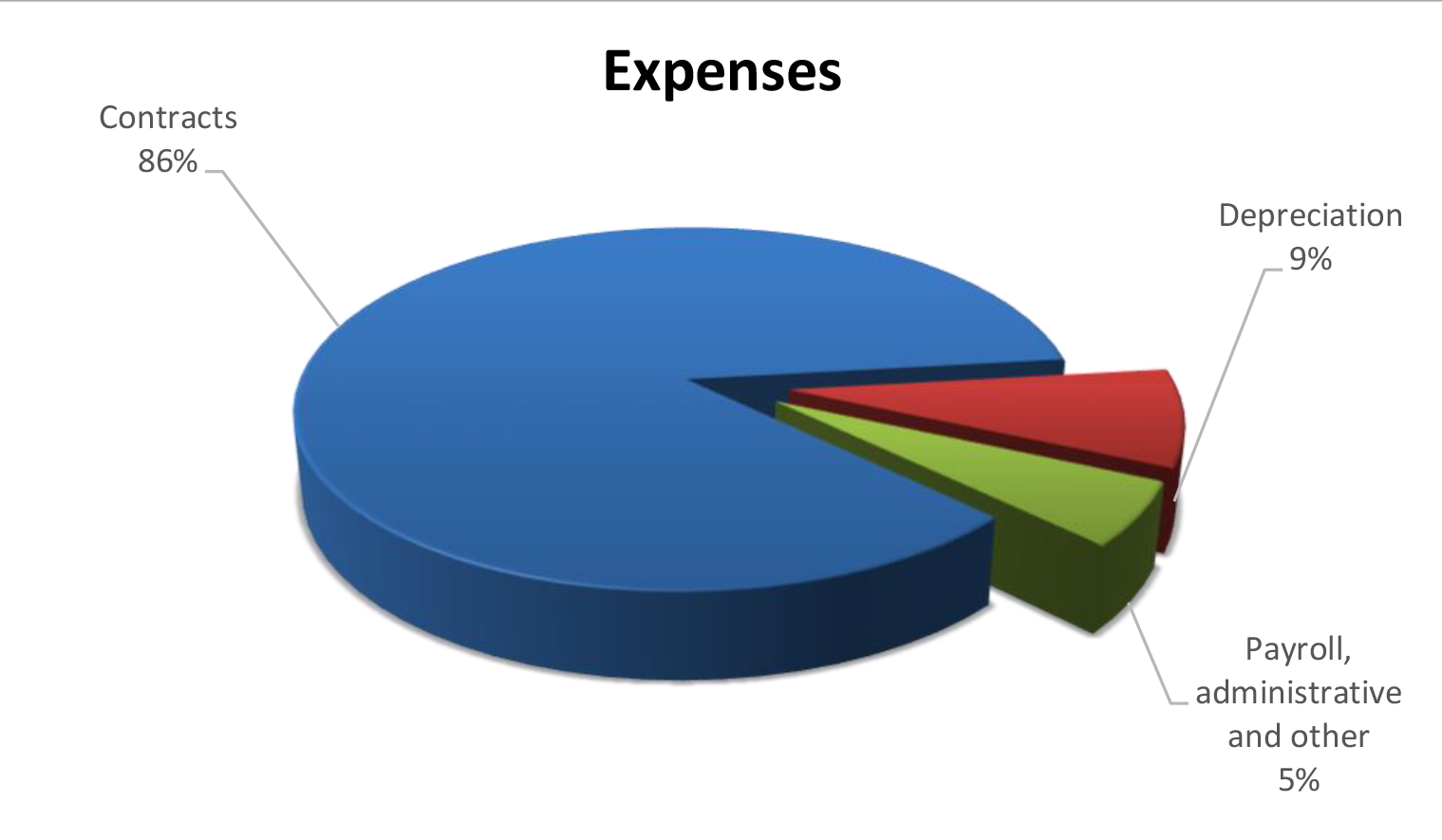

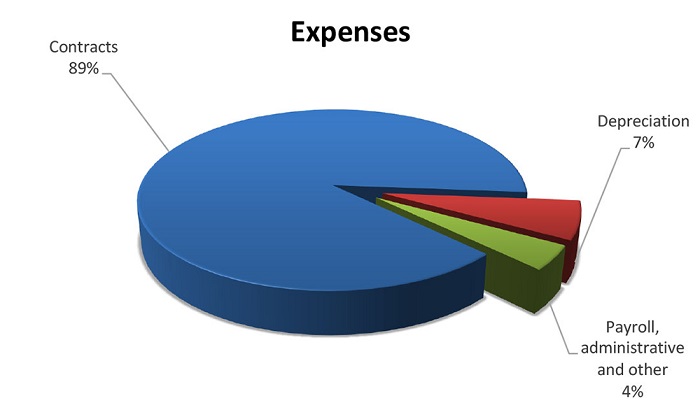

Total expenses of $114.8 million consisted of $102 million for contracts, $8.6 million for depreciation, and $4.2 million for payroll, administrative, and other expenses.

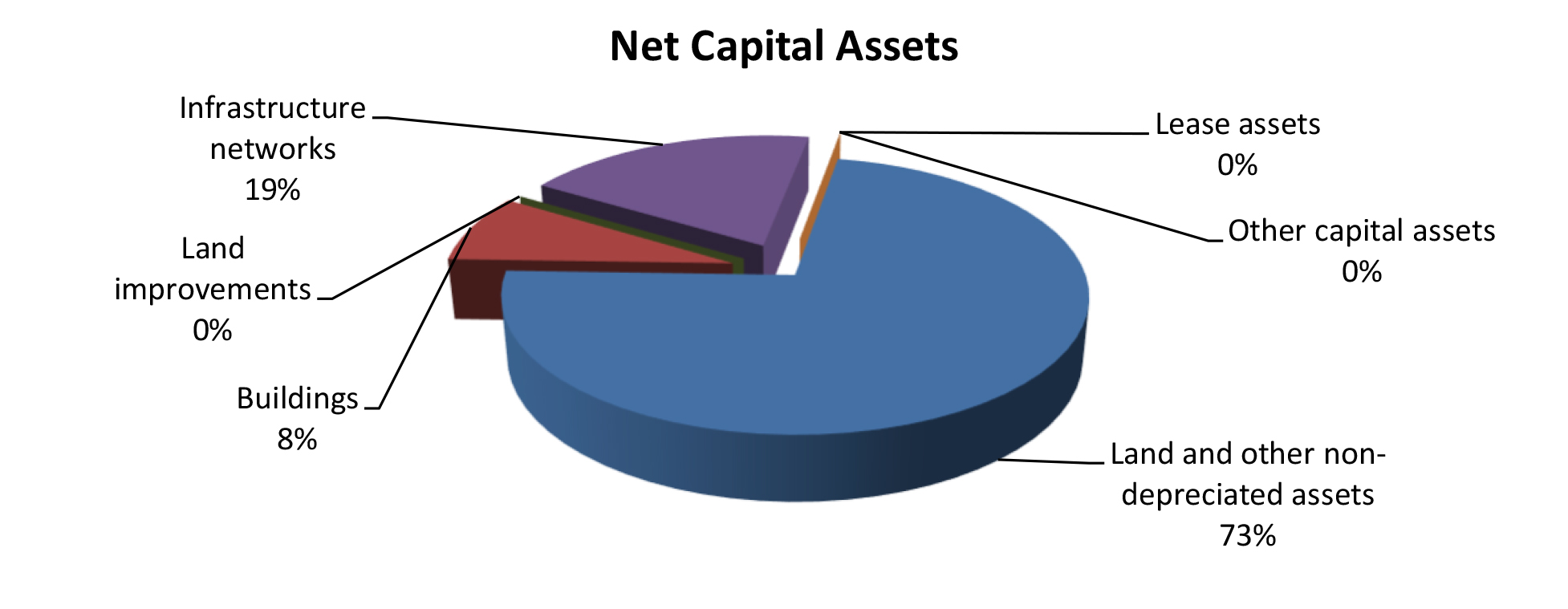

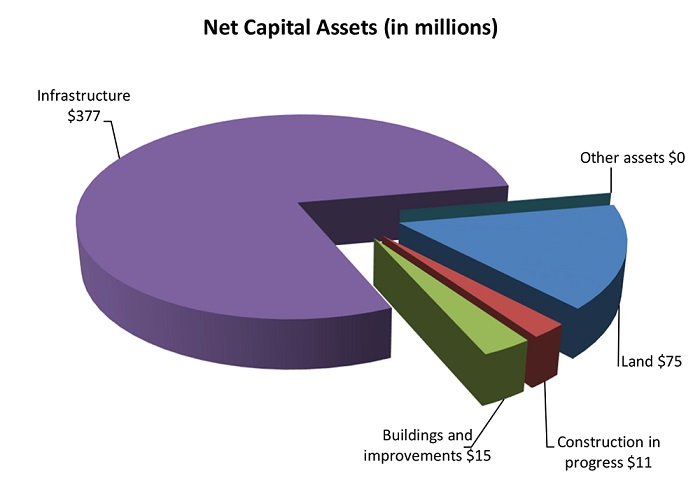

As of June 30, 2024, total assets and deferred outflows of resources of $309.1 million exceeded total liabilities and deferred inflows of resources of $24.4 million, resulting in a net position of $284.7 million. Total assets and deferred outflows of resources included (1) cash of $73.2 million, (2) land and net capital assets of $189.5 million, and (3) other assets and deferred outflows of resources of $46.4 million.

Auditors’ Opinion HTA RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles. HTA received a qualified opinion on its compliance with major federal programs in accordance with the Uniform Guidance.

Findings THERE WERE NOREPORTED DEFICIENCIES in internal control over financial reporting that were considered to be material weaknesses and no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

There were two material weaknesses in internal control over compliance that were required to be reported in accordance with the Uniform Guidance. A material weakness in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented or detected and corrected on a timely basis. The material weaknesses are described on pages 52-54 of the report.

About the Authority

The Hawai‘i Tourism Authority (HTA) was established by the 1998 Legislature to serve as the State’s lead agency for strategically managing tourism in Hawai‘i. State law requires HTA to develop a tourism marketing plan that includes statewide promotional efforts and programs, targeted markets, and other marketing efforts with measures of effectiveness and documentation of HTA’s progress toward strategic plan goals. HTA is also responsible for the Hawai‘i Convention Center. The primary source of funding for HTA’s operations is the General Fund. HTA is headed by a board of directors comprised of 12 voting

members, each of whom is appointed by the Governor, and is an agency of the Department of Business, Economic Development and Tourism.

Financial Statements, Fiscal Year Ended June 30, 2024

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the Department of Transportation, Highways Division, as of and for the fiscal year ended June 30, 2024, and to comply with the requirements of Title 2, U.S. Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by Accuity LLP.

Financial Highlights

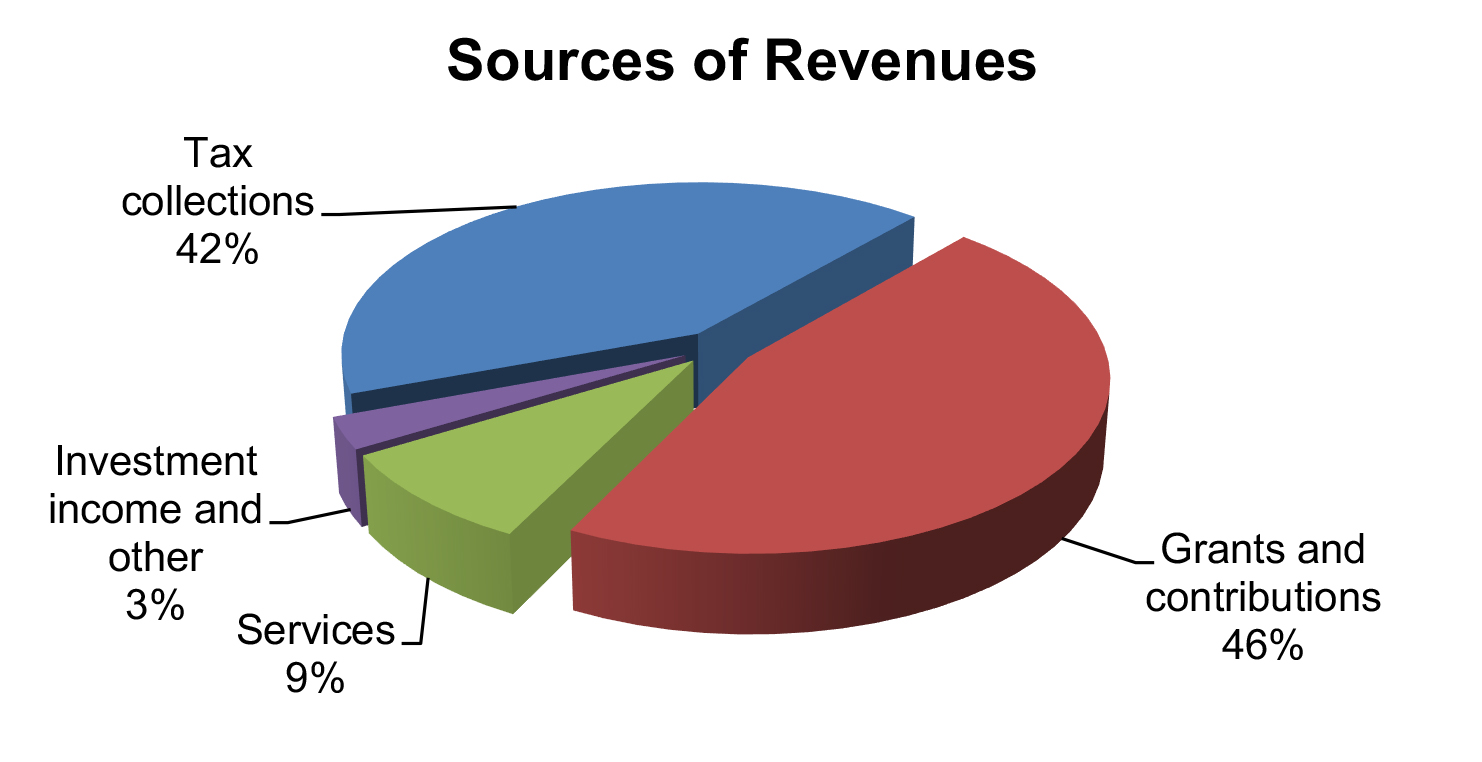

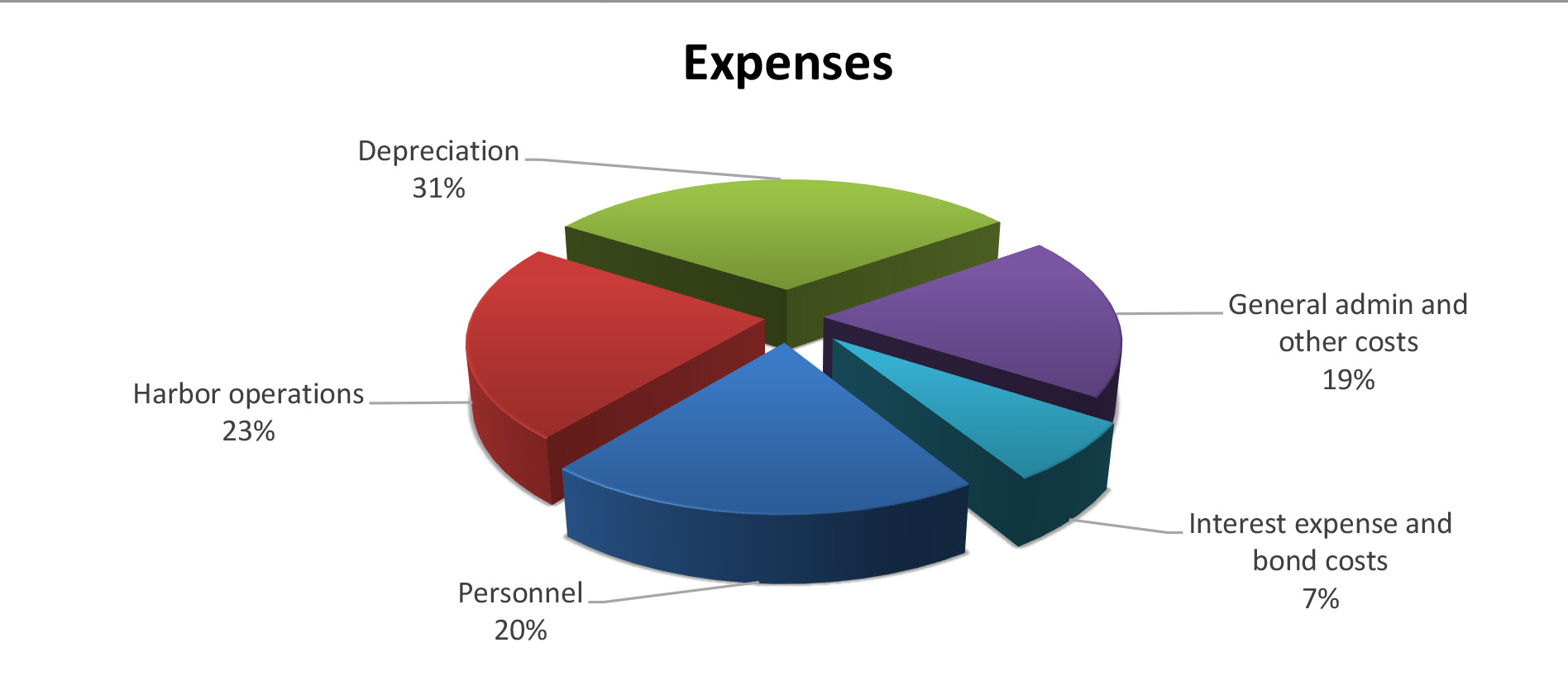

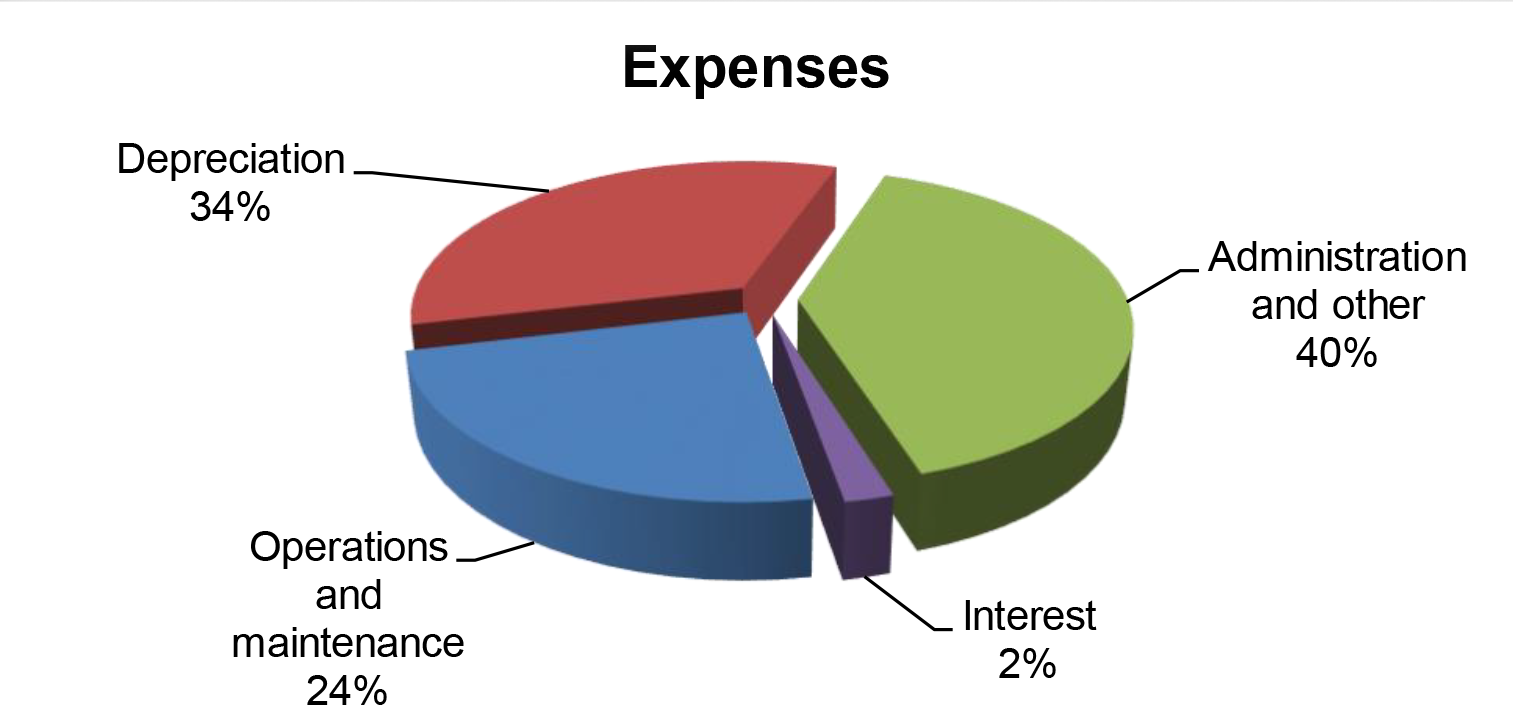

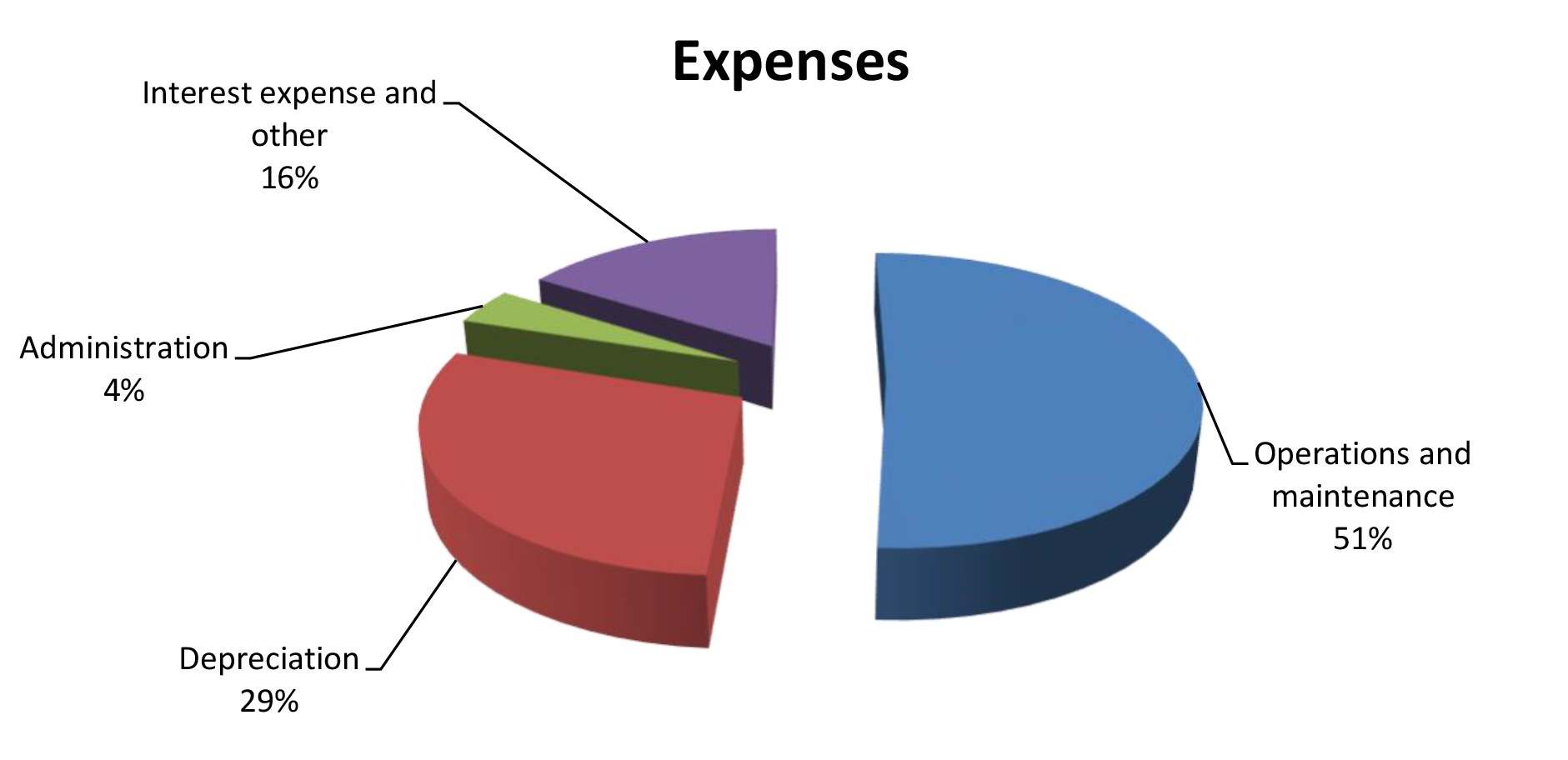

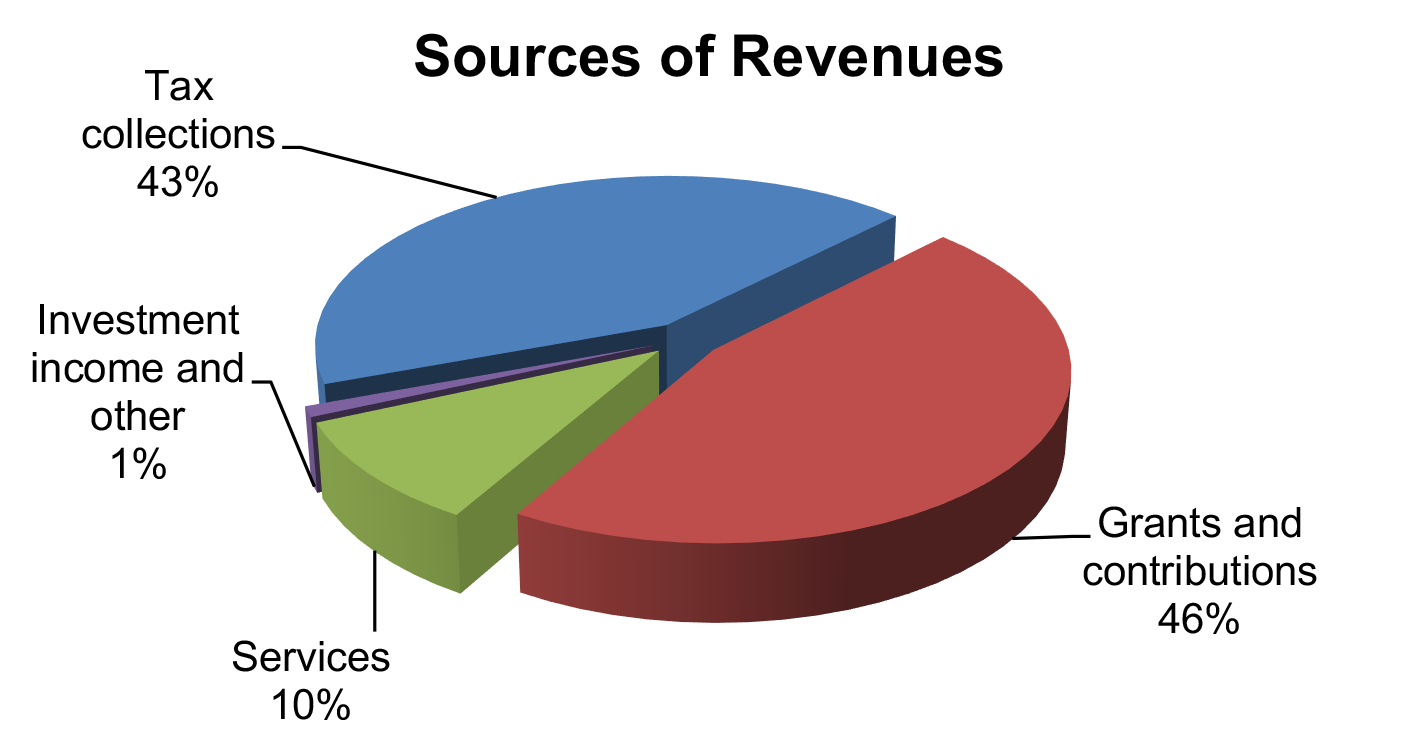

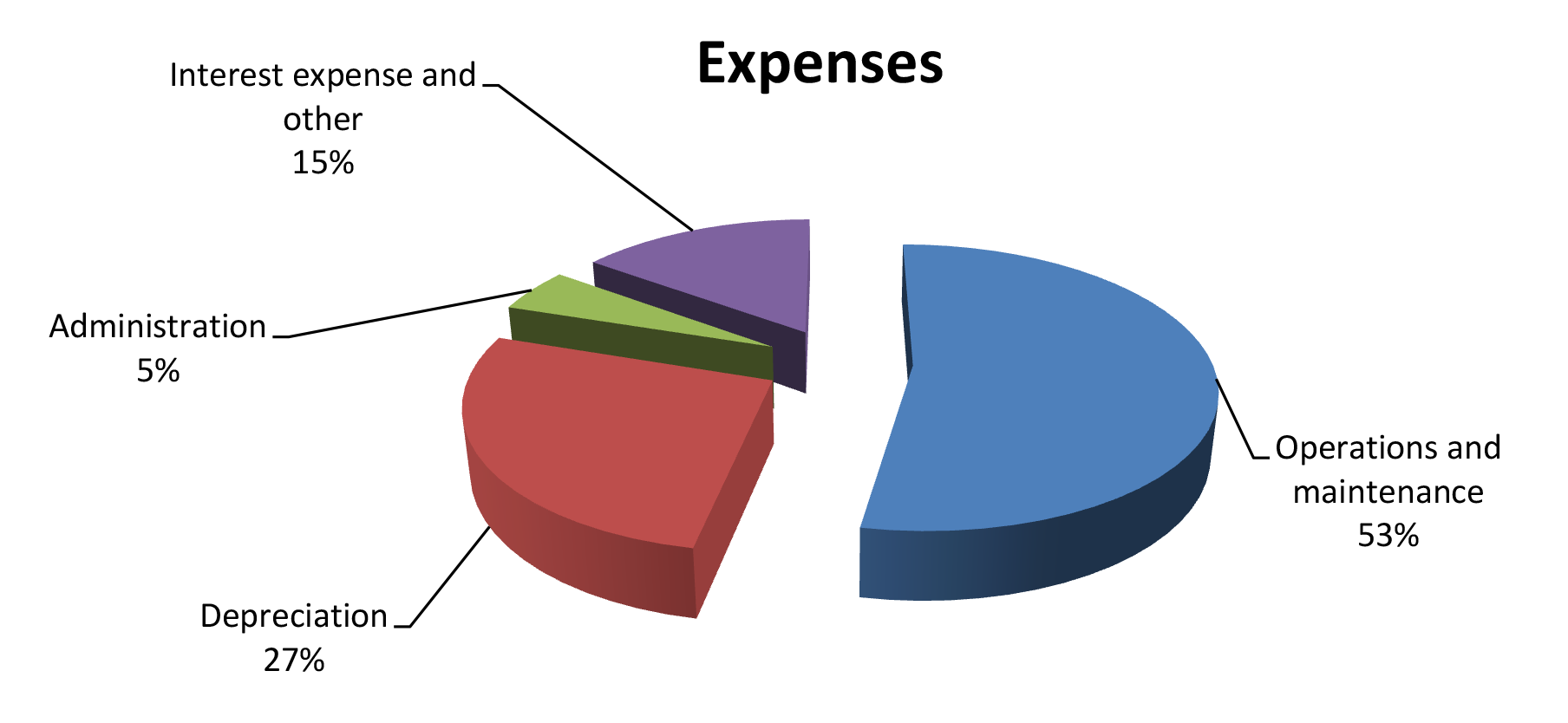

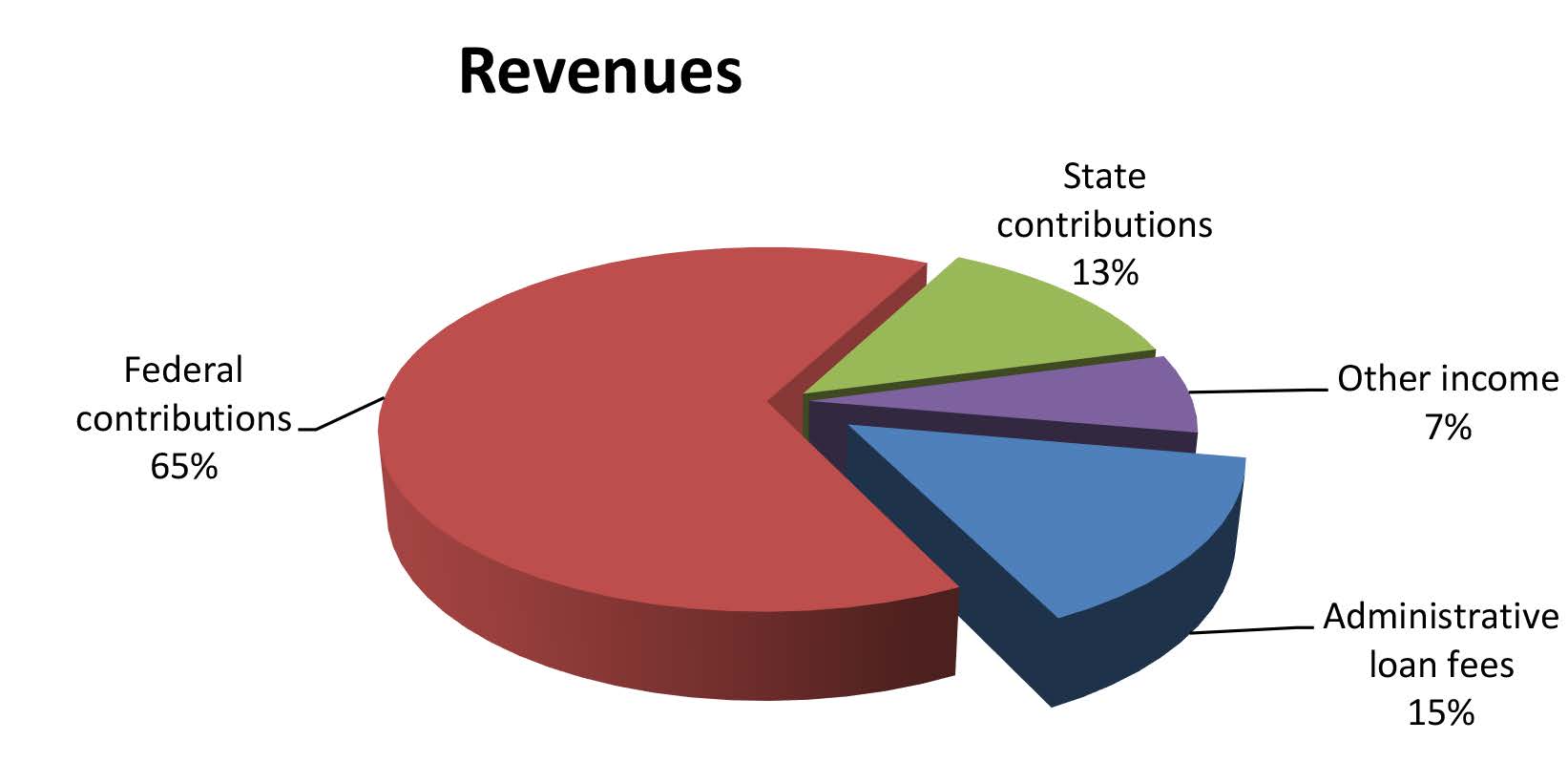

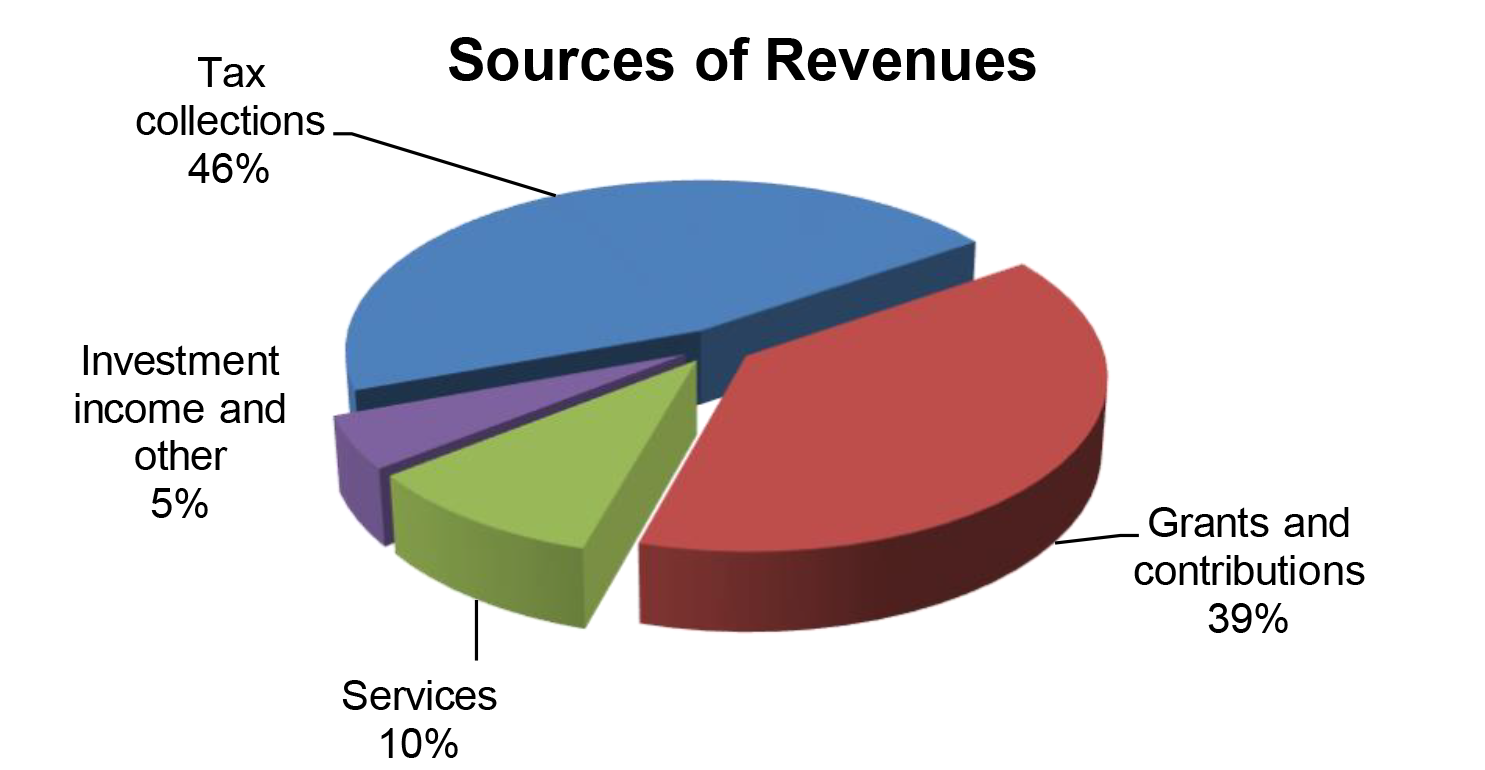

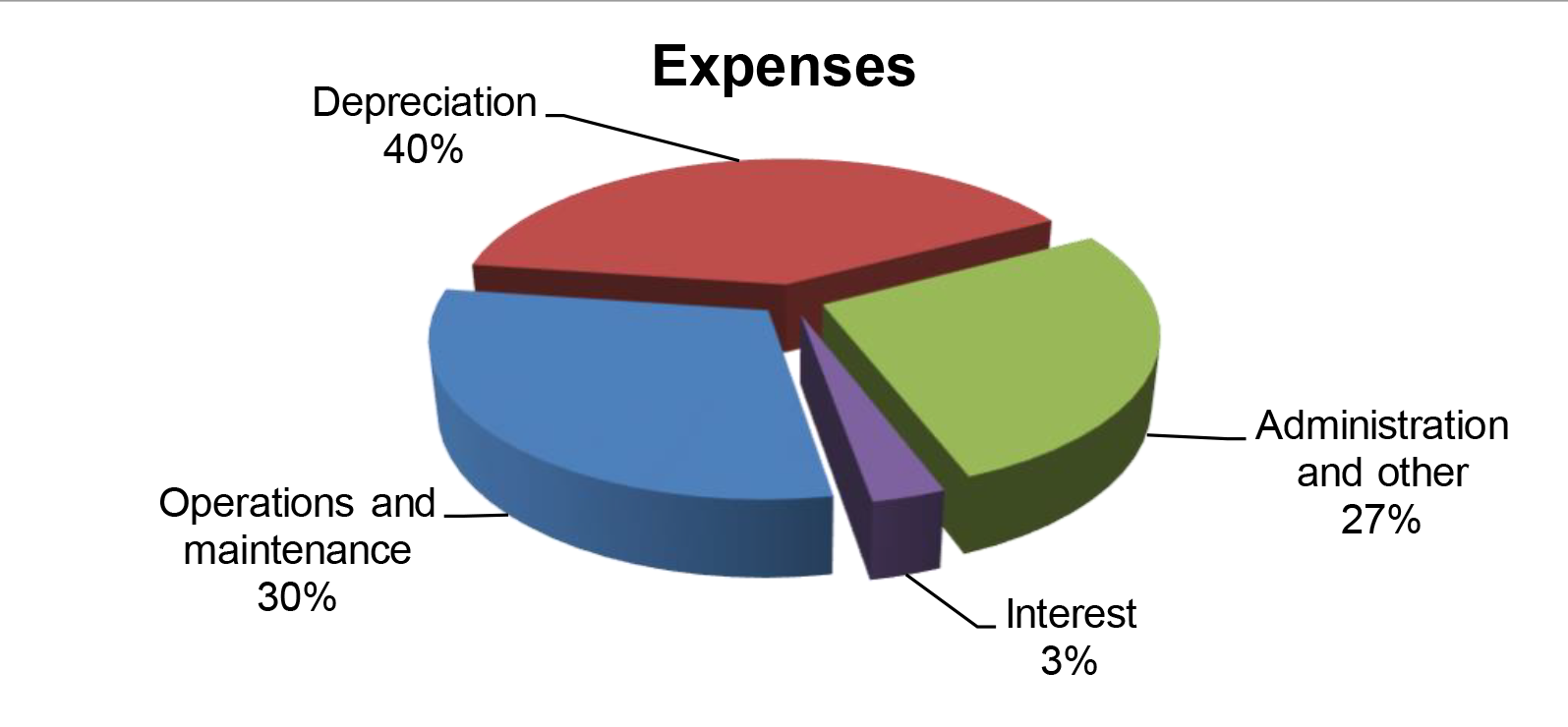

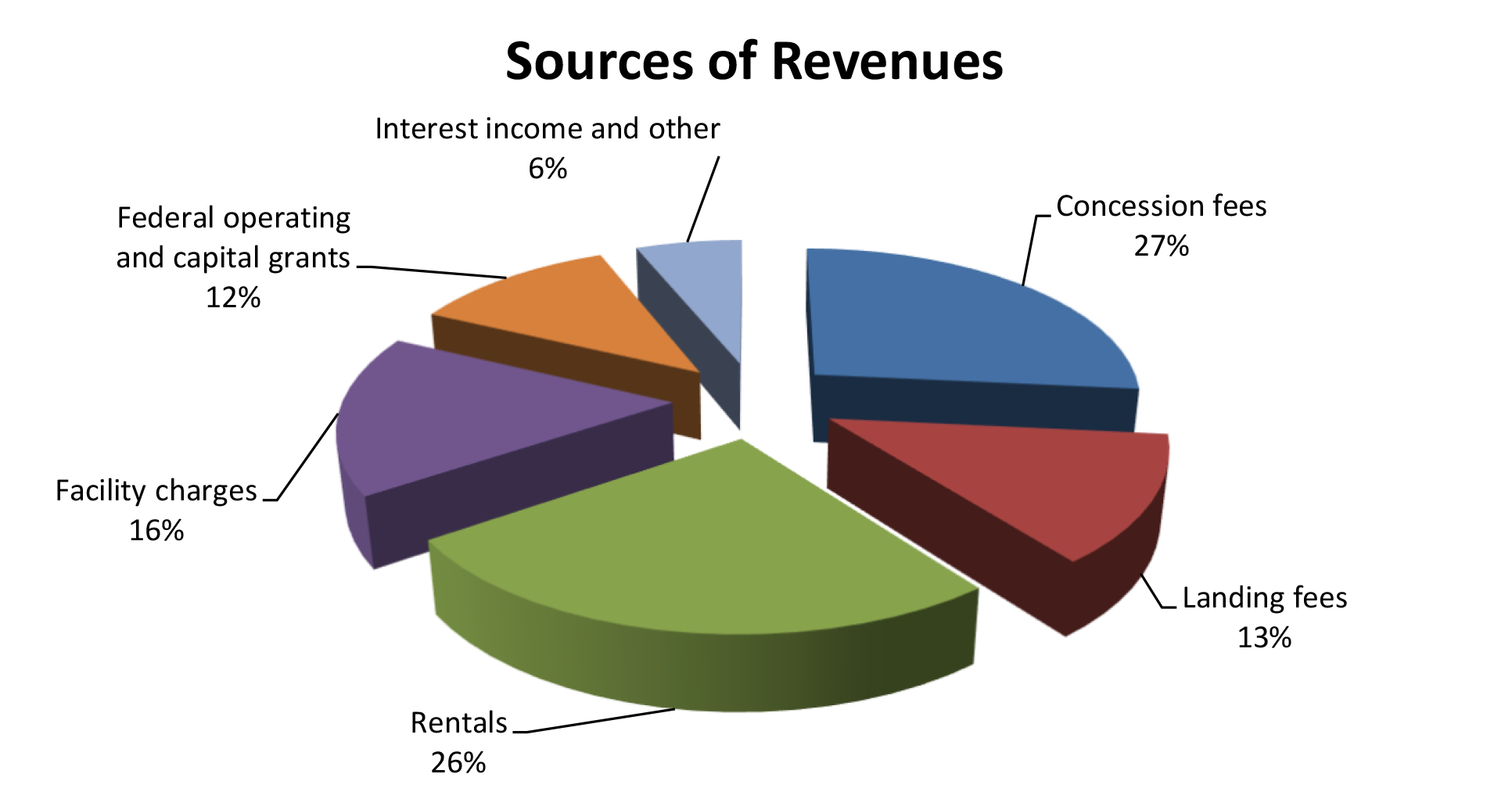

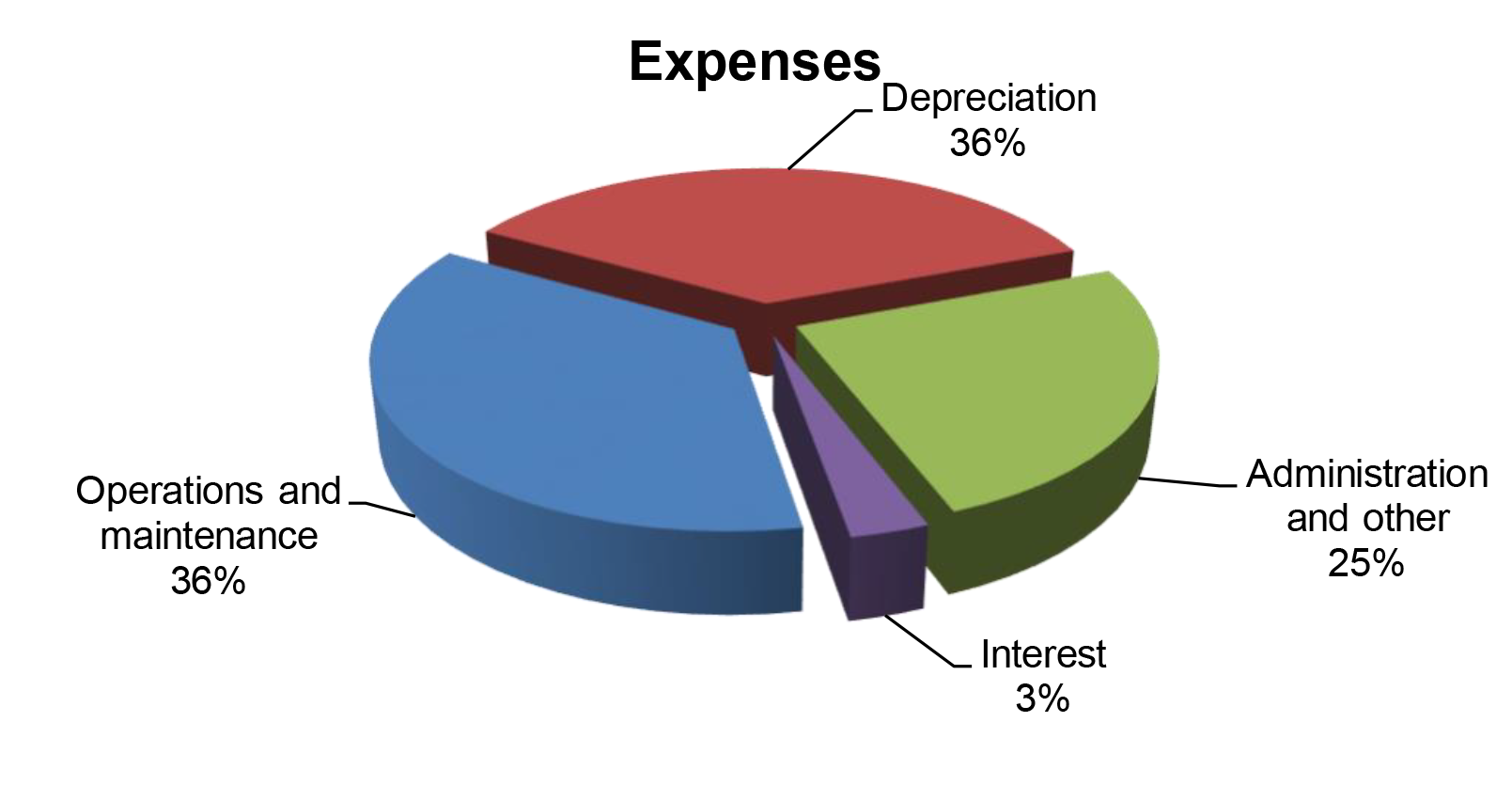

FOR THE FISCAL YEAR ended June 30, 2024, DOT–Highways reported total revenues of $634.6 million and total expenses of $628.8 million, resulting in an increase in net position of $5.8 million. Revenues consisted of (1) $269.2 million in tax collections; (2) $289.5 million in grants and contributions primarily from the Federal Highway Administration; (3) $56.1 million in charges for services; and (4) $19.8 million in investment income and other revenues.

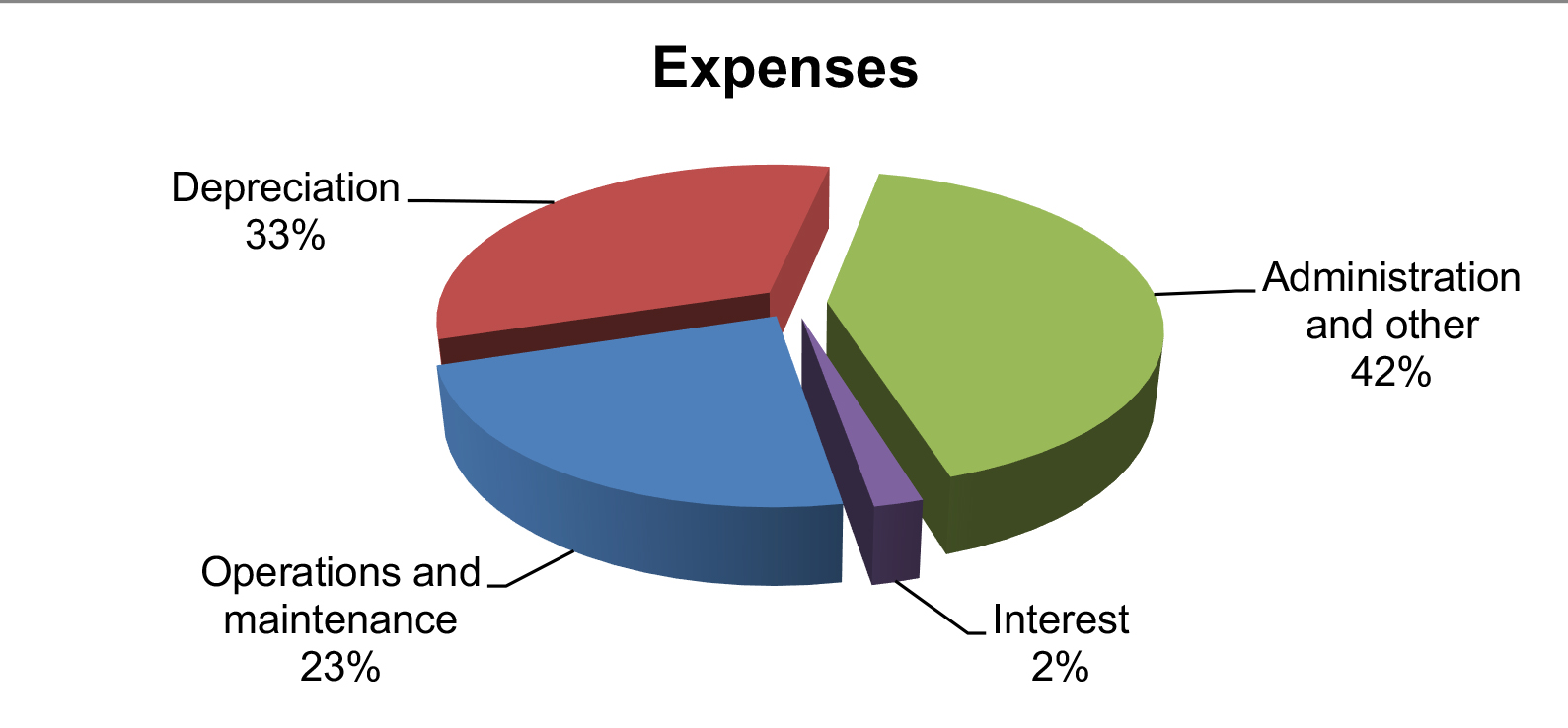

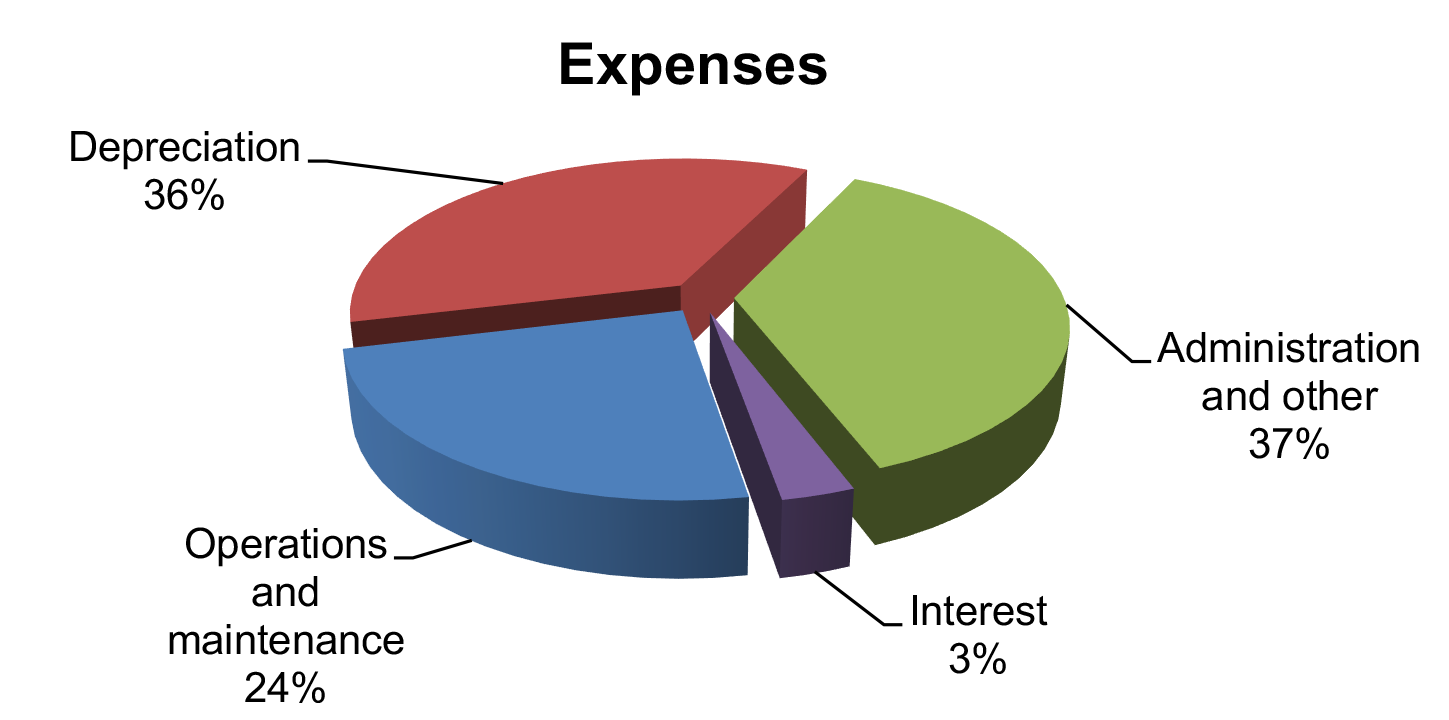

Expenses consisted of (1) $143.7 million for operations and maintenance; (2) $206 million in depreciation; (3) $268.1 million for administration and other expenses; and (4) $11 million in interest.

As of June 30, 2024, total assets and deferred outflows of resources of $5.5 billion were comprised of (1) cash and investments of $415.2 million; (2) net capital assets of $5 billion; and (3) $75.5 million in other assets and deferred outflows of resources. Total liabilities of $765.9 million included $534.2 million in revenue bonds and $231.7 million in other liabilities.

DOT–Highways has numerous capital projects ongoing statewide; construction-in-progress totaled $353.3 million at the end of the fiscal year.

Auditors’ Opinion DOT-HIGHWAYS RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles. DOT–Highways also received an unmodified opinion on its compliance with major federal programs in accordance with the Uniform Guidance.

Findings THERE WERE NO REPORTED DEFICIENCIES in internal control over financial reporting that were considered to be material weaknesses and no instances of noncompliance or other matters that were required to be reported under Government Auditing Standards. There were no findings that were considered material weaknesses in internal control over compliance in accordance with the Uniform Guidance.

About the Division

The mission of the Department of Transportation, Highways Division (DOT–Highways) is to provide a safe, efficient, and sustainable State Highway System that ensures the mobility of people and goods within the State. The division is charged with maximizing available resources to provide, maintain, and operate ground transportation facilities and support services that promote economic vitality and livability in Hawai‘i. DOT–Highways also works with the Statewide Transportation Planning Office on innovative and diverse approaches to congestion management.

Financial Statements, Fiscal Year Ended June 30, 2024

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements of the Department of Transportation, Administration Division, as of and for the fiscal year ended June 30, 2024, and to comply with the requirements of Title 2, U.S. Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by KKDLY LLC.

Financial Highlights

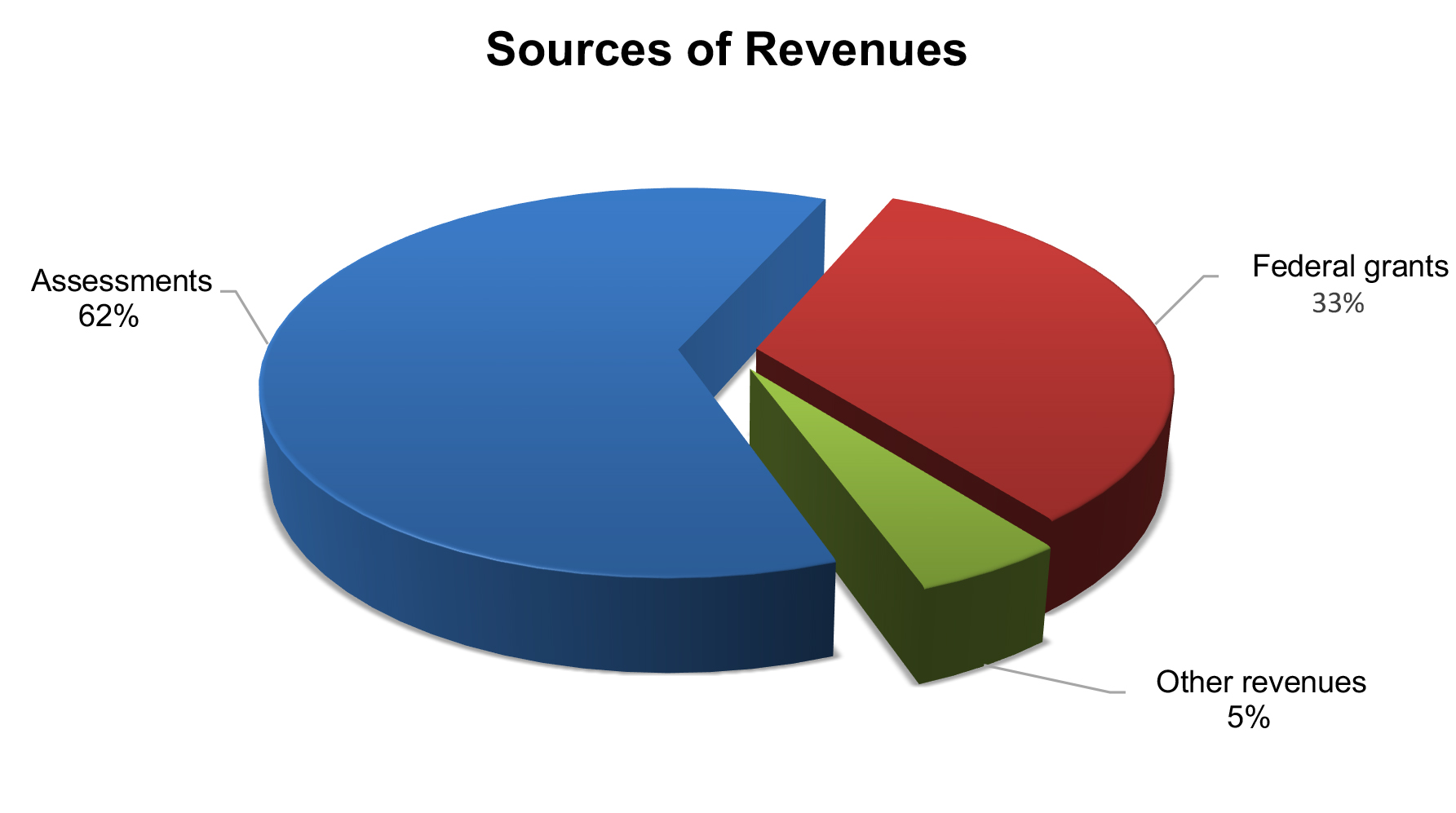

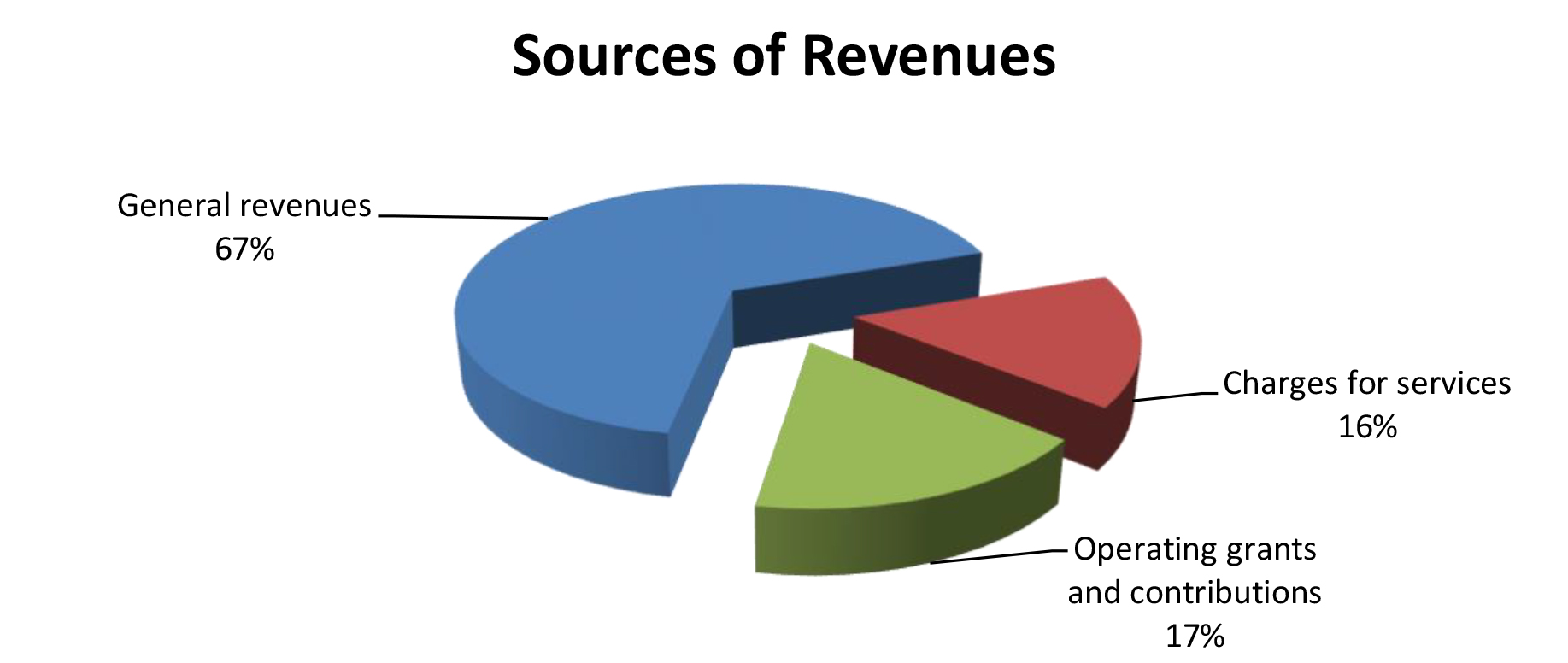

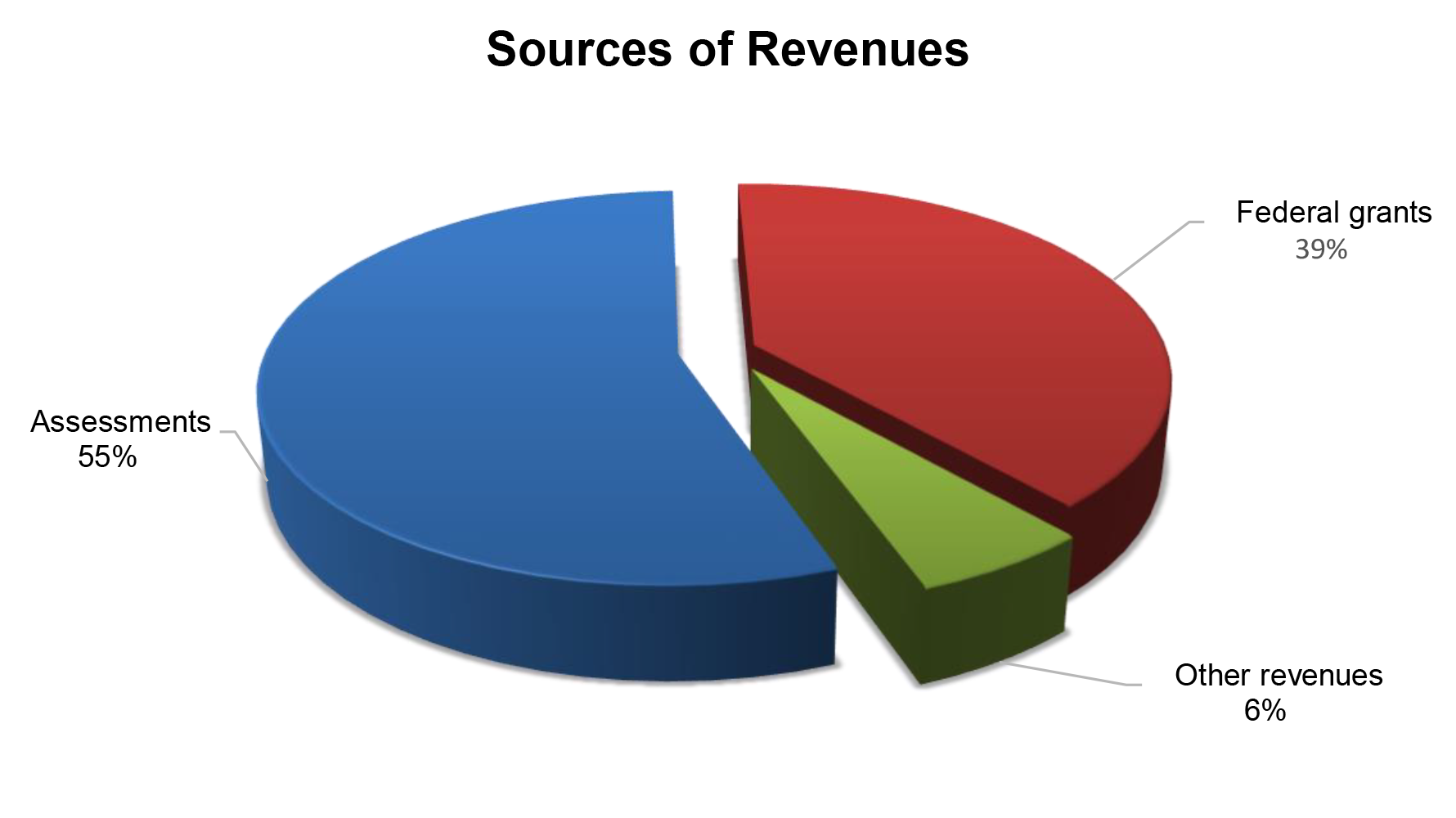

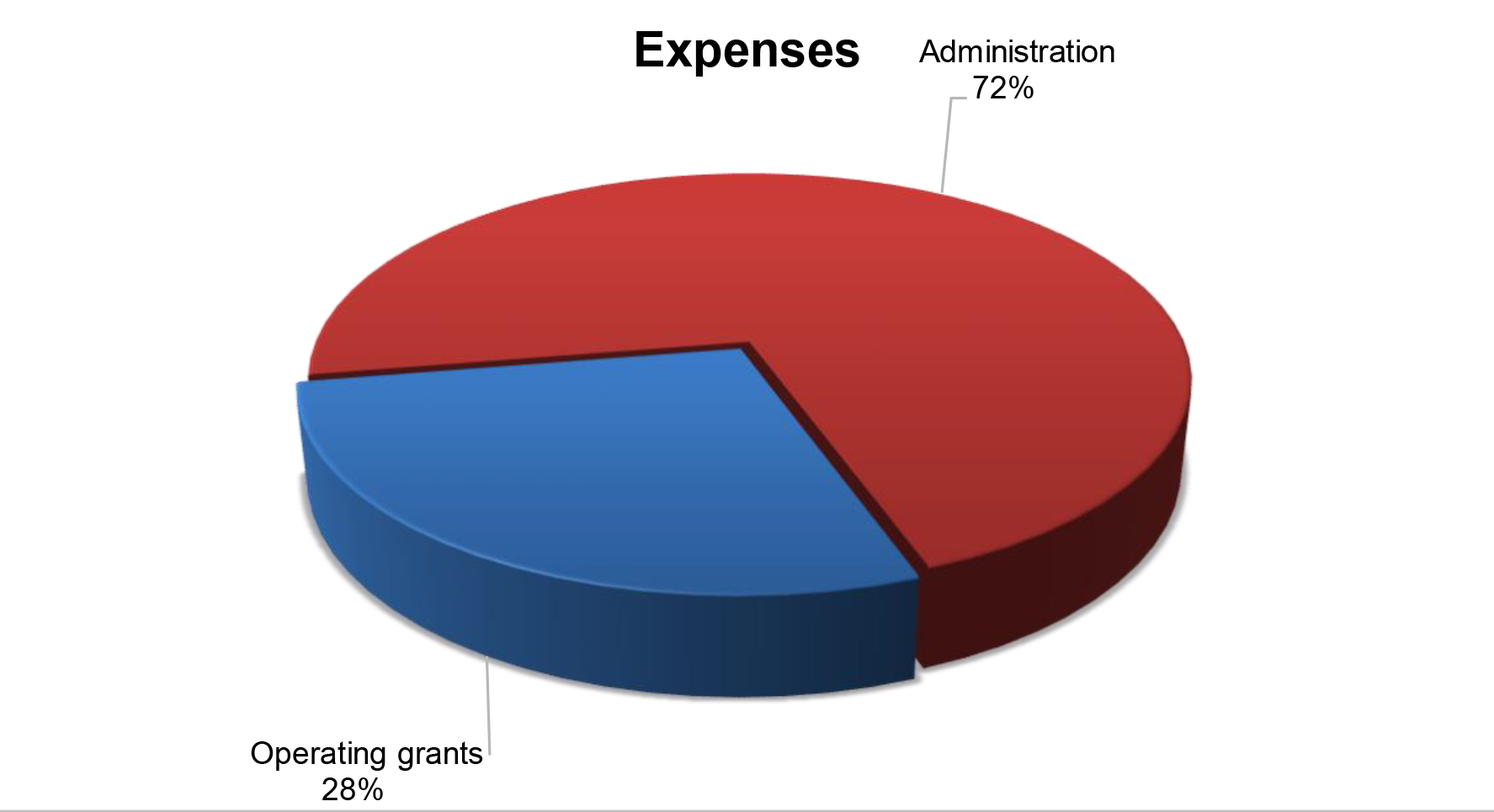

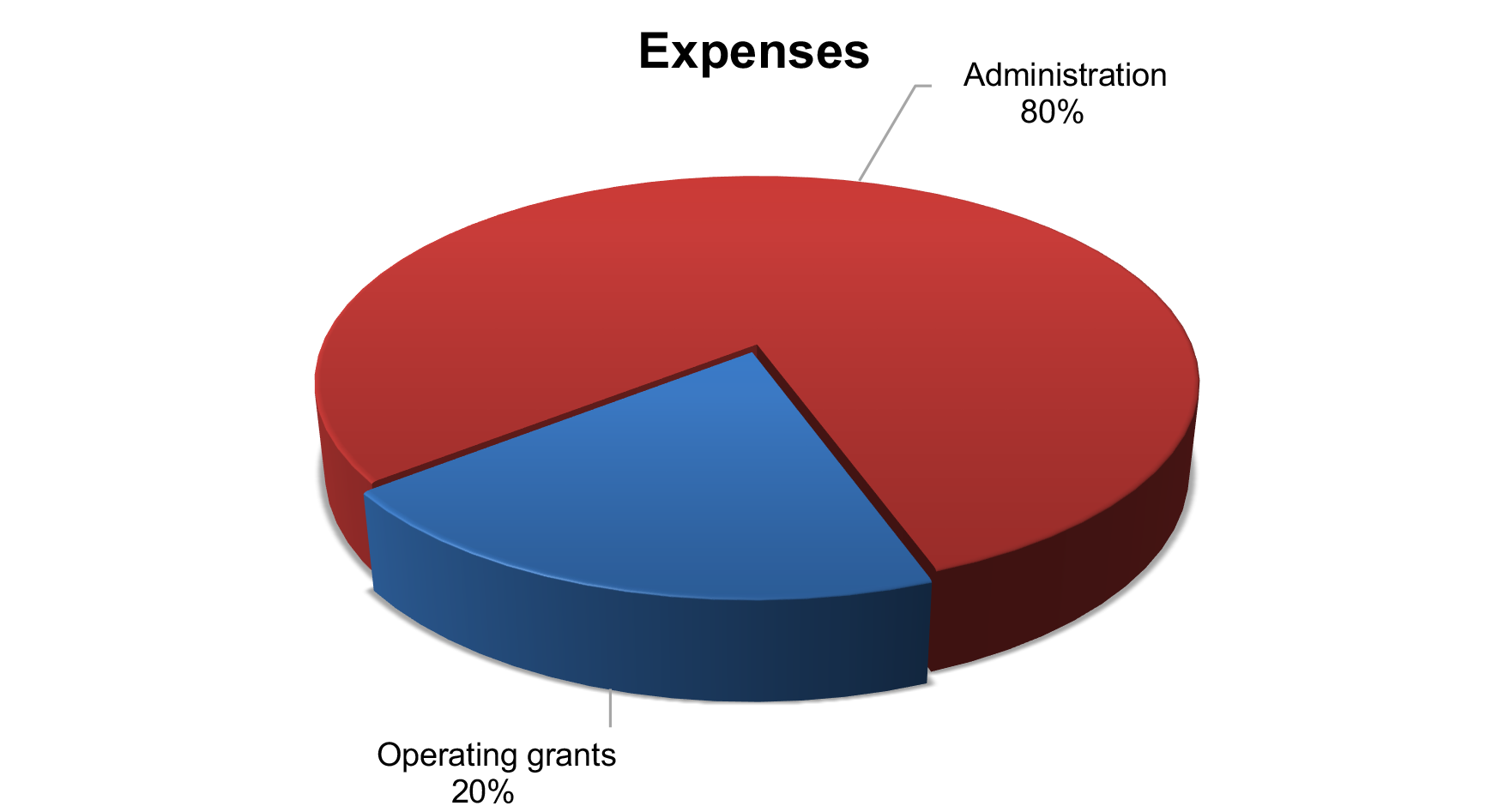

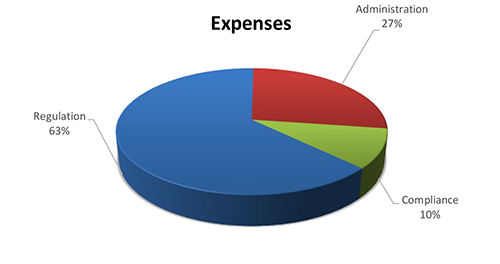

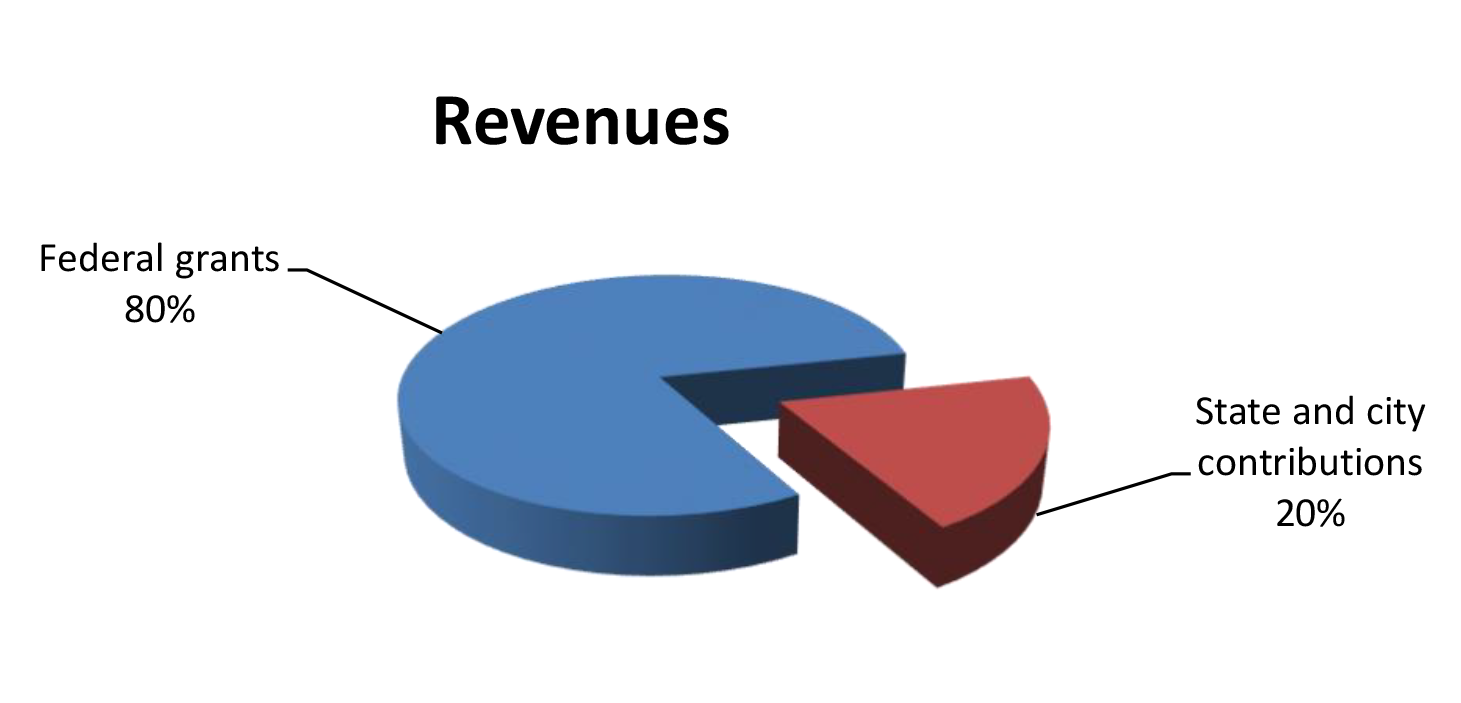

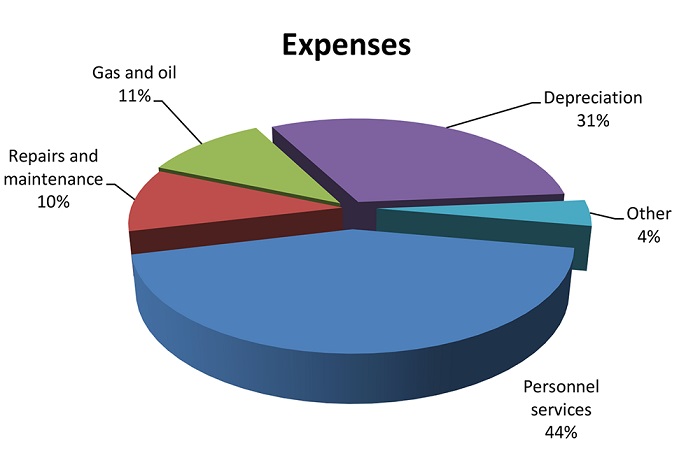

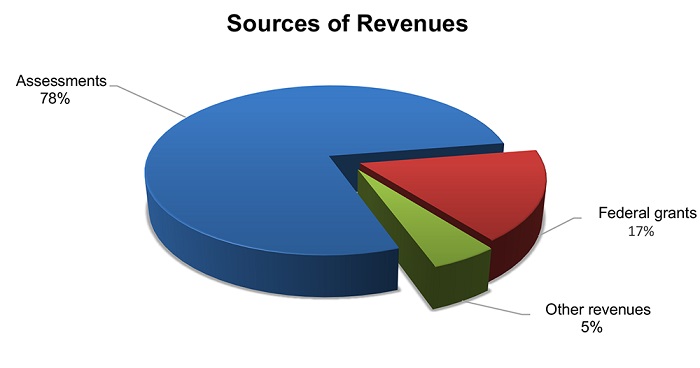

FOR THE FISCAL YEAR ended June 30, 2024, DOT–Administration reported total revenues of $42.6 million, total expenses of $38.3 million, and net transfers of $8.1 million, resulting in a decrease in net position of $3.8 million. Revenues consisted of $26.4 million from assessments, $14.2 million from federal grants, and $2 million from other revenue sources.

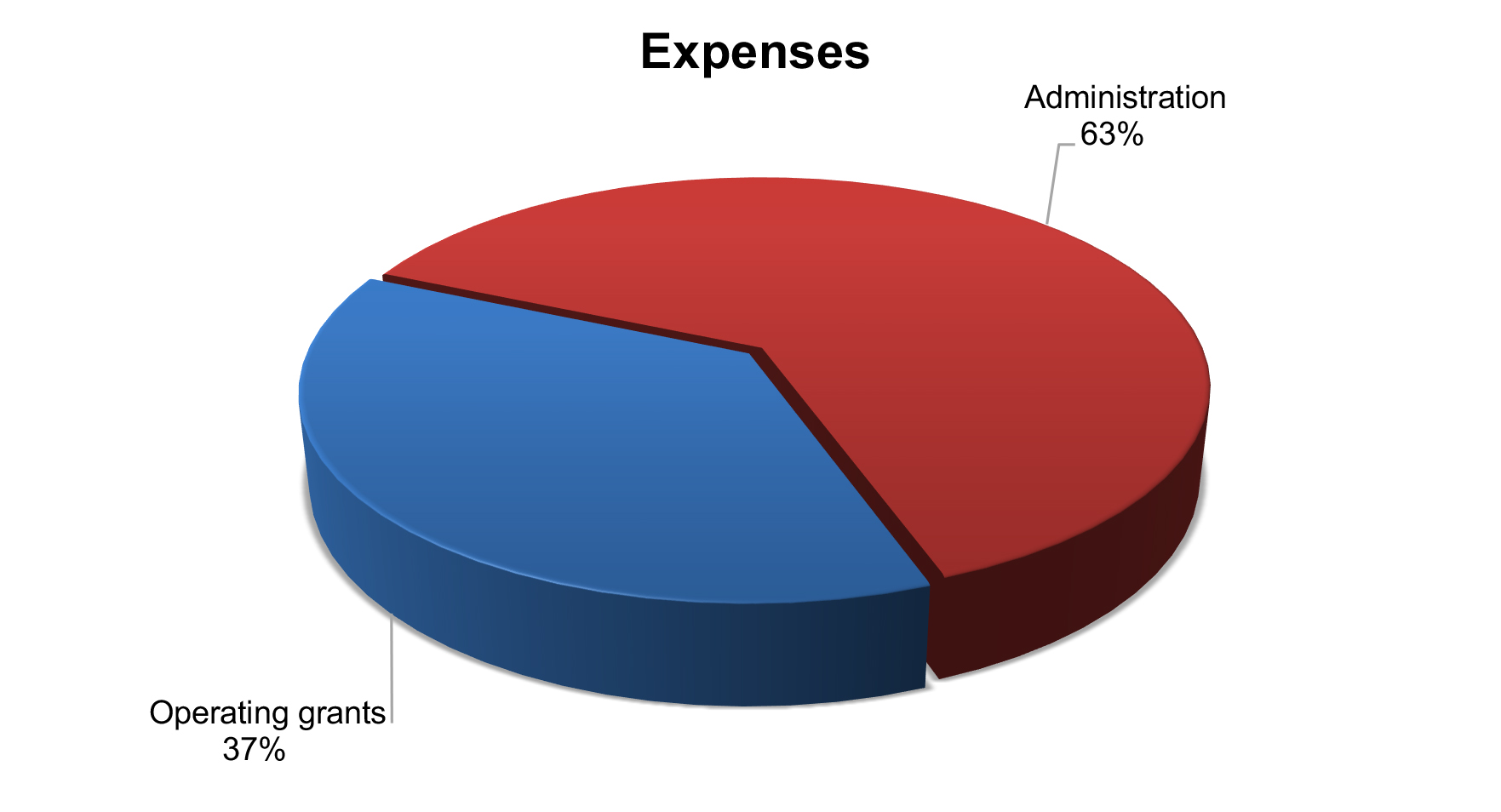

Total expenses of $38.3 million consisted of $14.2 million for operating grants and $24.1 million for administration.

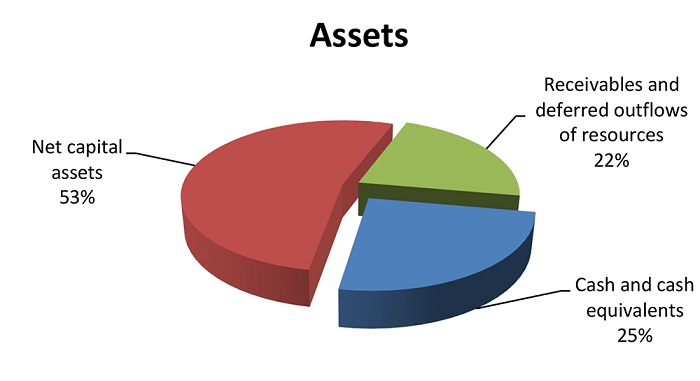

As of June 30, 2024, total assets of $49.2 million were comprised of (1) cash of $17.8 million,

(2) accounts receivable of $25.5 million, and (3) net capital assets of $5.9 million. Liabilities totaled $43 million, including a $1 million Aloha Tower Development Corporation note payable to the Harbors Division.

Auditors’ Opinions

DOT—ADMINISTRATION RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles. DOT–Administration also received an unmodified opinion on its compliance with major federal programs in accordance with the Uniform Guidance.

Findings

THERE WERE NO REPORTED DEFICIENCIES in internal control over financial reporting that were considered to be material weaknesses and no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. There were no findings that were considered material weaknesses in internal control over compliance in accordance with the Uniform Guidance. However, the auditors identified one significant deficiency in internal controls over compliance that was required to be reported under the Uniform Guidance. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. The significant deficiency is described on pages 63-64 of the report.

Audit reports for the Department’s Airports Division, Harbors Division, and Highways Division are available on our website.

About the Division

The State Department of Transportation is comprised of four divisions (Airports, Harbors, Highways, and Administration). The Administration Division (DOT–Administration) includes the Office of the Director of Transportation, the Statewide Transportation Planning Office, and Departmental Staff Services Offices. Collectively, these offices provide overall administrative support for the Department of Transportation. The financial statements for the Division reflect the financial activities of DOT–Administration and the Aloha Tower Development Corporation, which is attached to the Department for administrative purposes. DOT–Administration receives a percentage of the Airports, Harbors, and Highways Divisions’ state-allotted appropriations to cover general administration expenses. The Department’s Statewide Transportation Planning Office administers certain Federal Transit Administration and Federal Highway Administration grants.

Financial Statements, Fiscal Year Ended June 30, 2024

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the Department of Commerce and Consumer Affairs, as of and for the fiscal year ended June 30, 2024. The audit was conducted by KMH LLP.

Financial Highlights

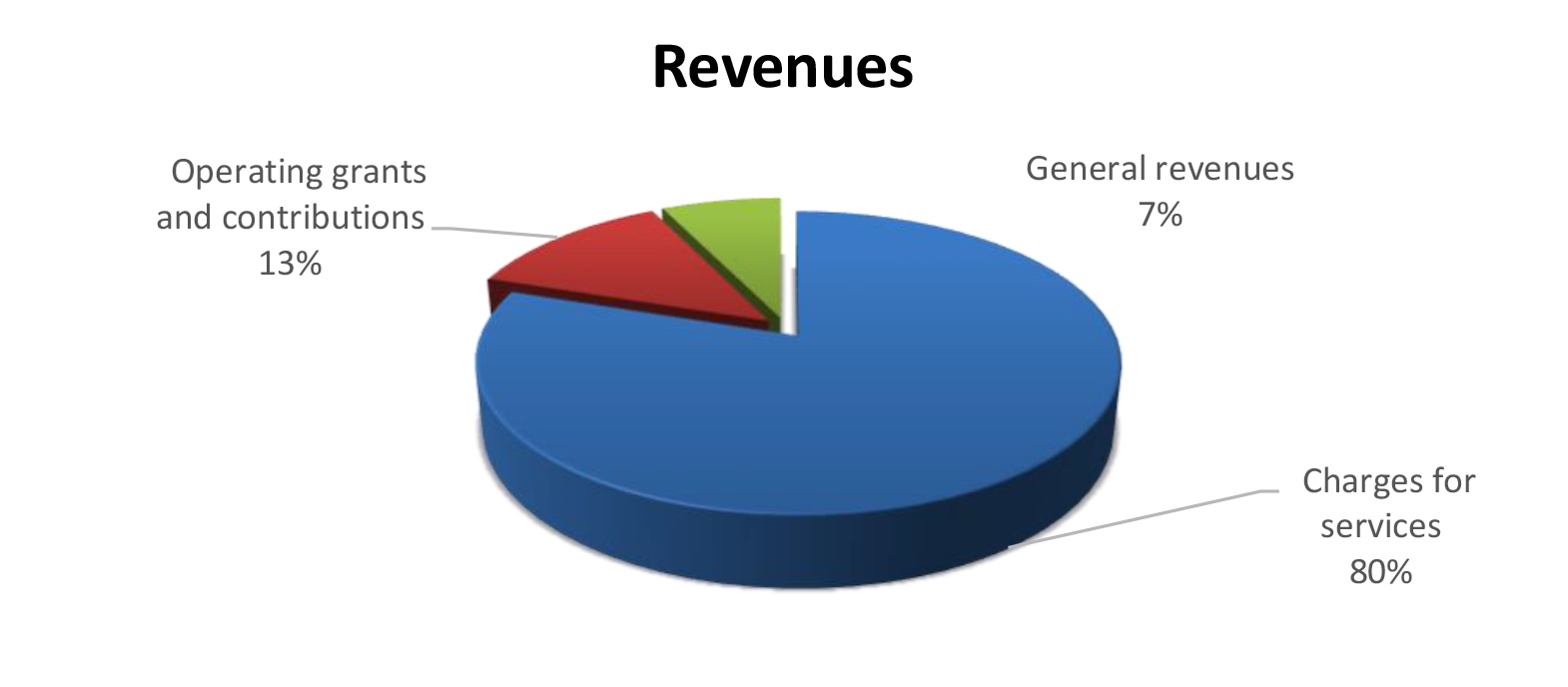

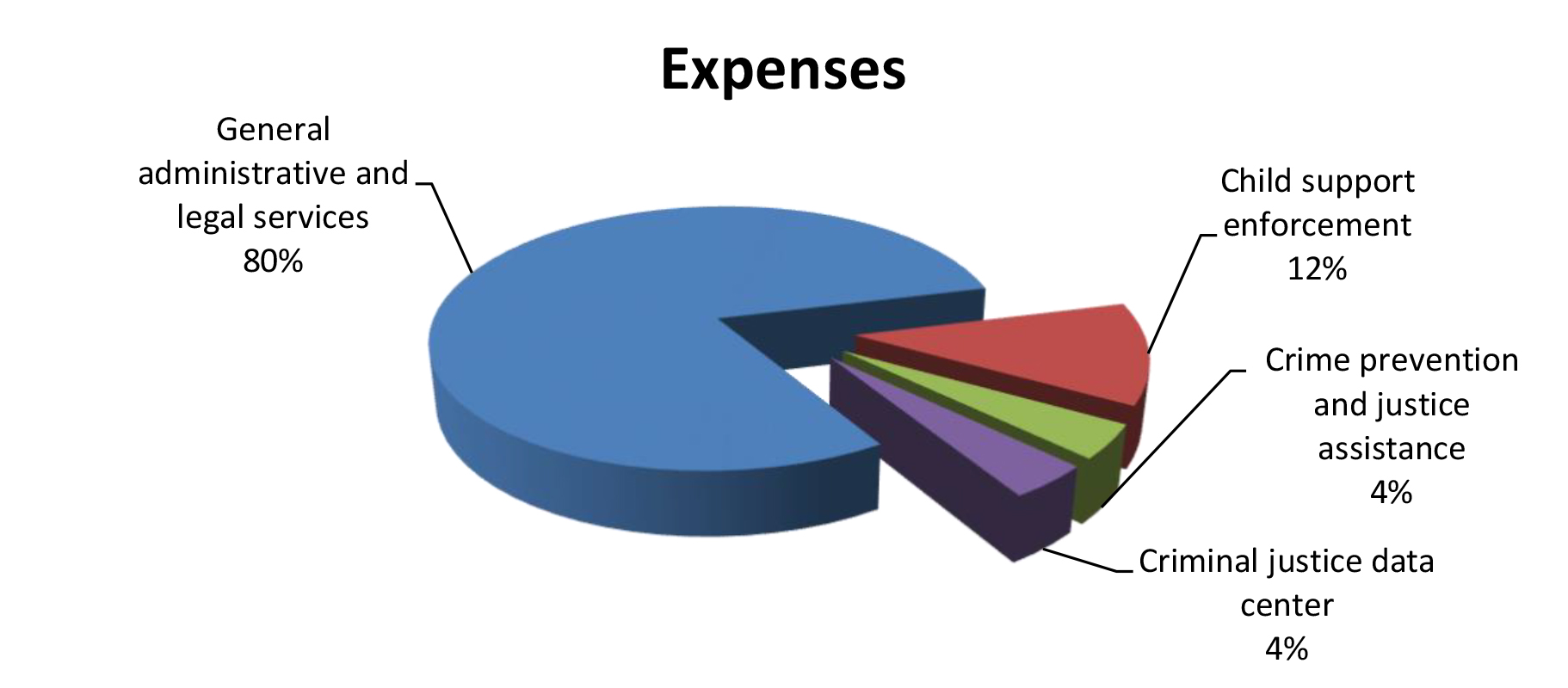

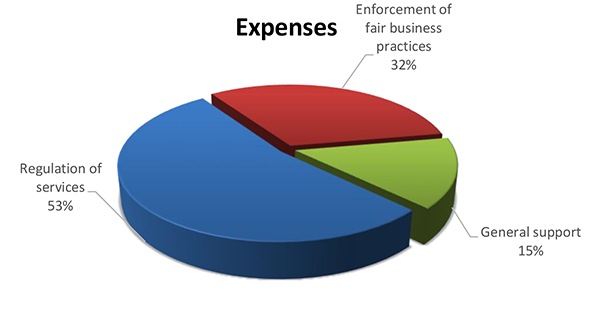

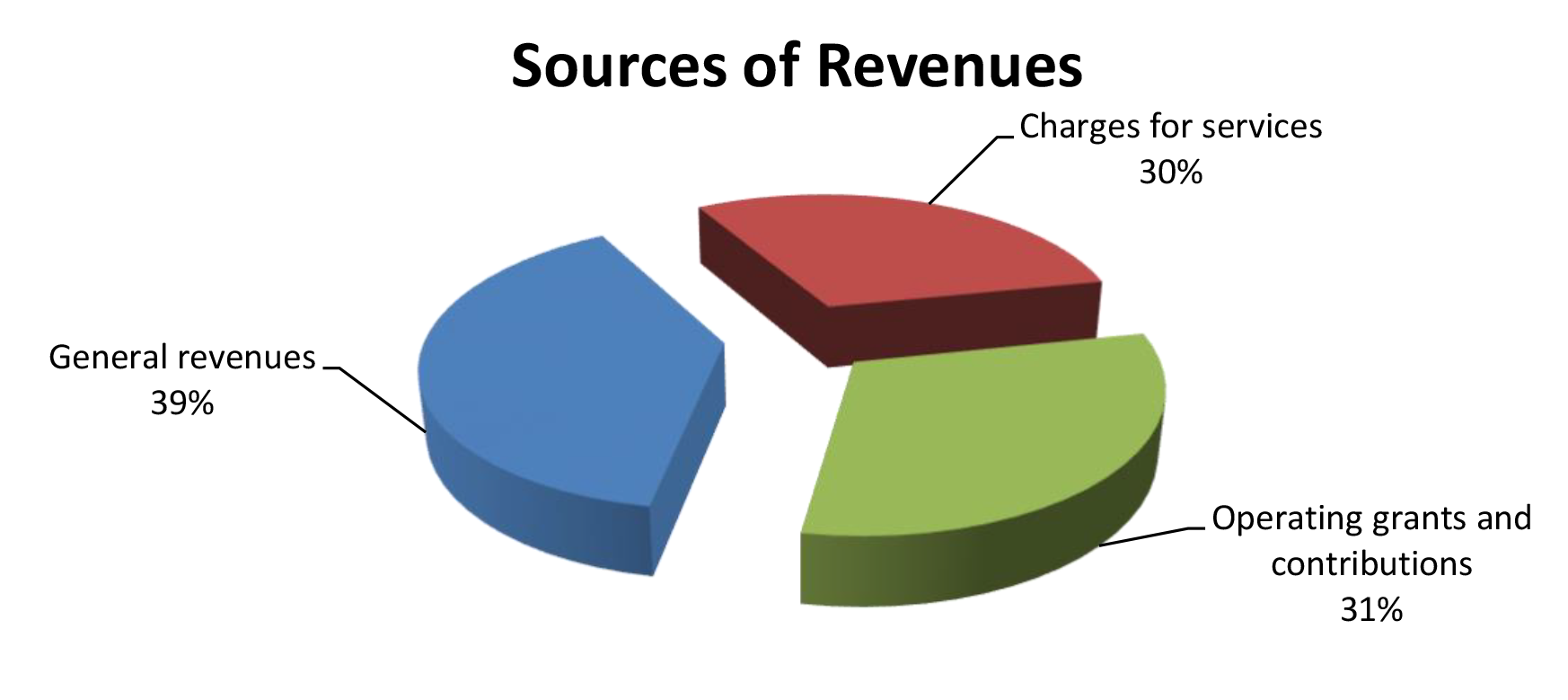

FOR THE FISCAL YEAR ended June 30, 2024, the DCCA reported total revenues of $76.6 million and total expenses of $79.4 million resulting in a decrease in net position of $2.8 million. Revenues consisted of (1) charges for services of $61.4 million, (2) operating grants and contributions of $9.7 million, and (3) general revenues of $5.5 million.

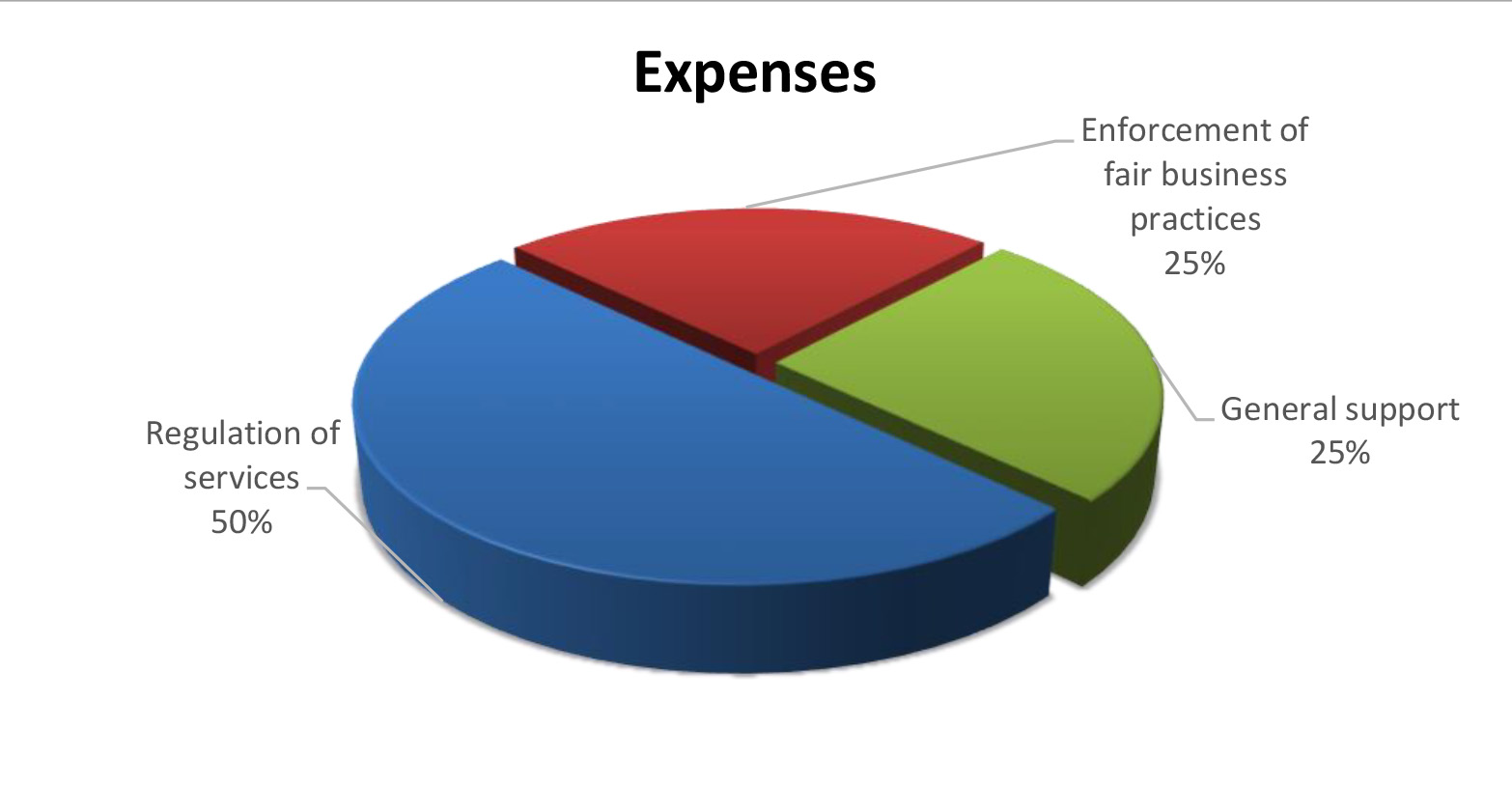

Total Expense of $79.4 million consisted of (1) $39.8 million for regulation of services, (2) $19.4 million for enforcement of fair business practices, and (3) $20.2 million for general support.

As of June 30, 2024, total assets of $175.8 million exceeded total liabilities of $14.8 million, resulting in a net position of $161 million. Total assets included (1) cash of $159.4 million, (2) interest receivable of $500,000, (3) net capital assets of $11.8 million, and (4) other assets of $4.1 million.

Auditors’ Opinion

DCCA RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles.

Findings

THERE WERE NO REPORTED DEFICIENCIES in internal control over financial reporting that were considered to be material weaknesses and no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

About the Organization

The Department of Commerce and Consumer Affairs (DCCA) serves the public through a variety of functions, including regulating and licensing more than 140,000 professionals, monitoring the financial solvency of local banks and insurance companies, and investigating complaints of fraudulent and unfair business practices. The DCCA is made up of nine divisions: Business Registration Division, Cable Television Division, Division of Consumer Advocacy, Division of Financial Institutions, Insurance Division, Office of Administrative Hearings, Office of Consumer Protection, Professional and Vocational Licensing Division, and Regulated Industries Complaints Office.

Financial Statements, Fiscal Year Ended June 30, 2024

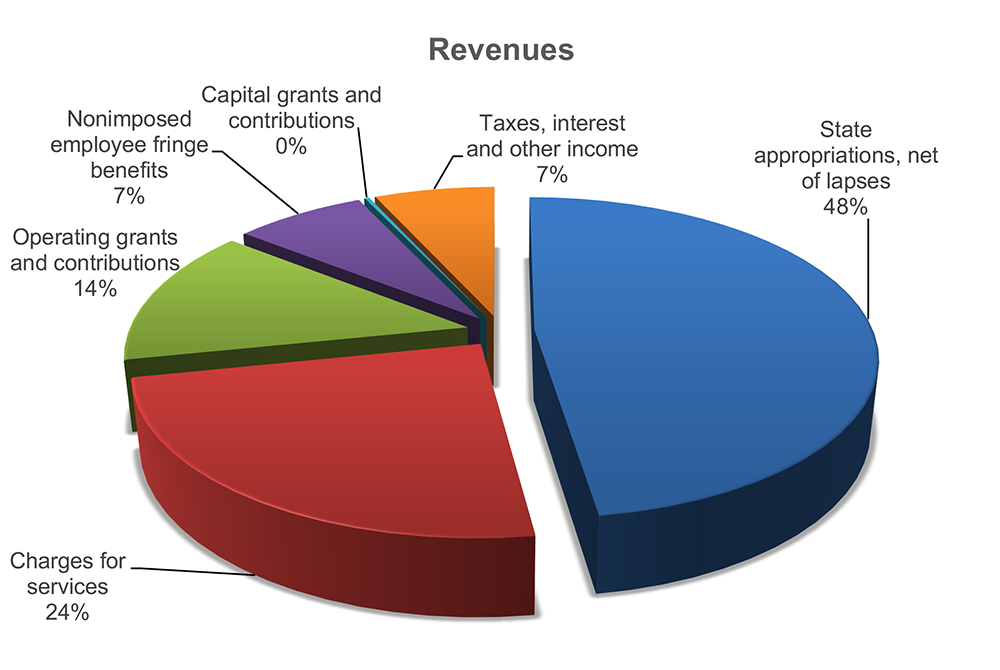

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the financial statements for the O‘ahu Metropolitan Planning Organization, as of and for the fiscal year ended June 30, 2024, and to comply with the requirements of Title 2, U.S. Code of Federal Regulations, Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by N&K CPAs, Inc.

Financial Highlights

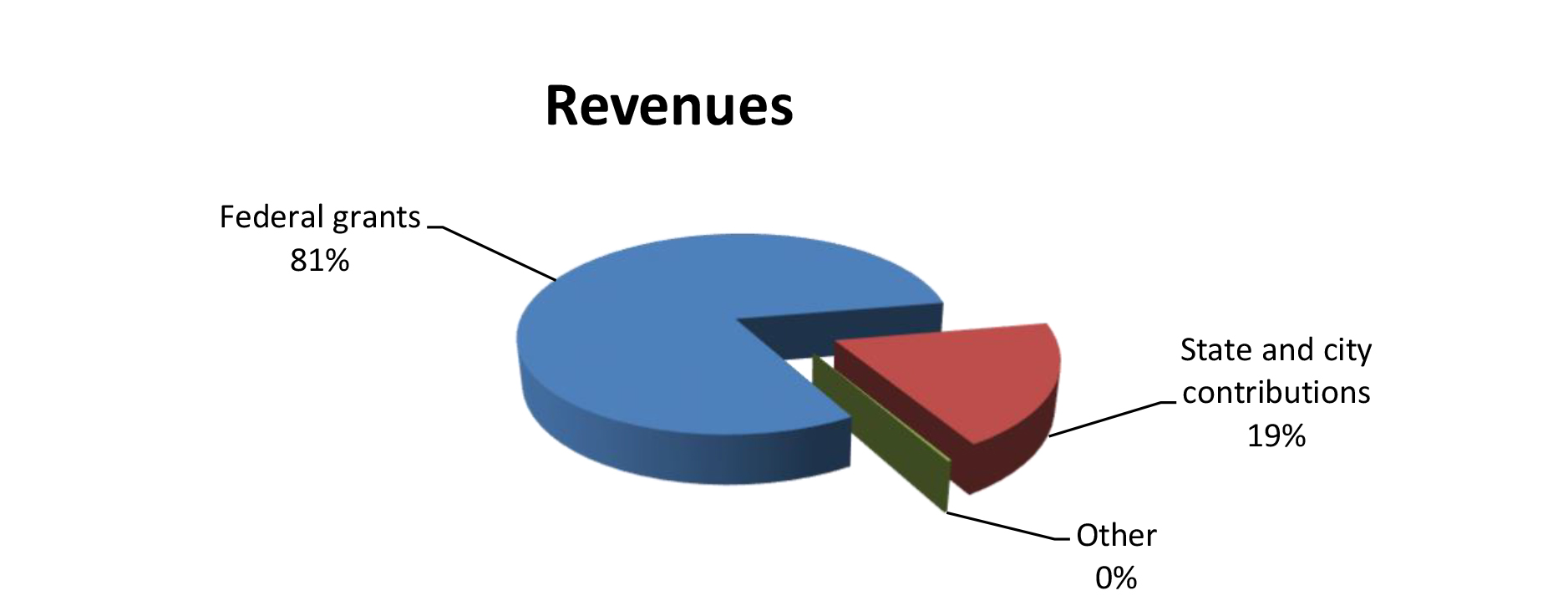

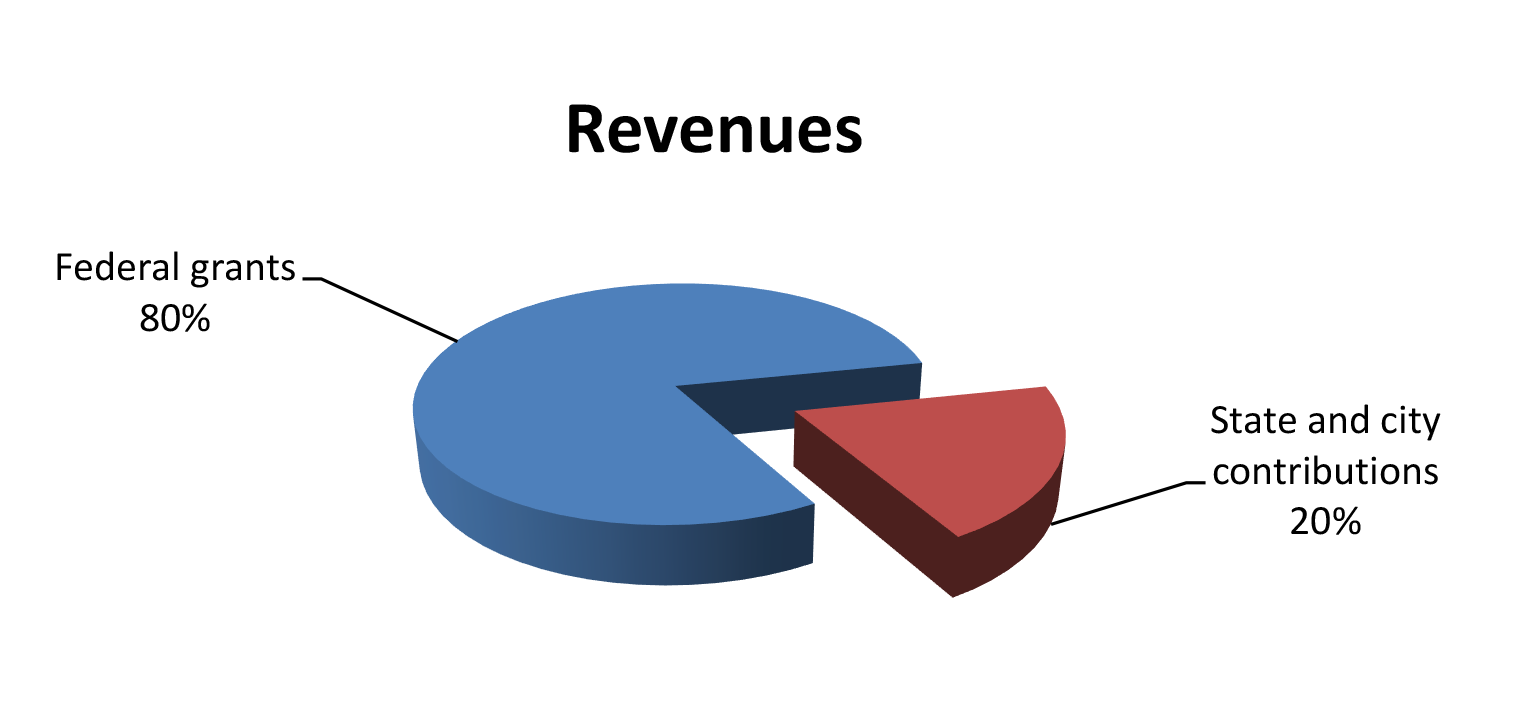

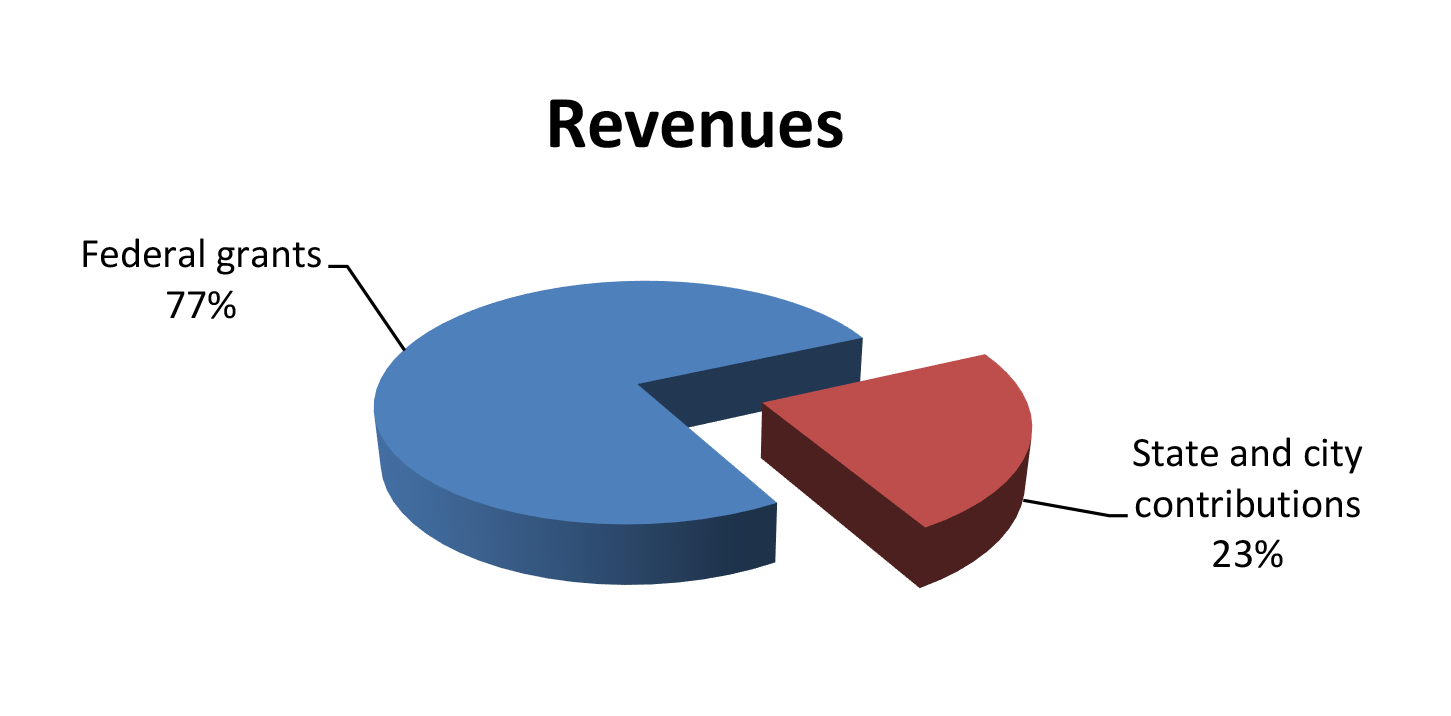

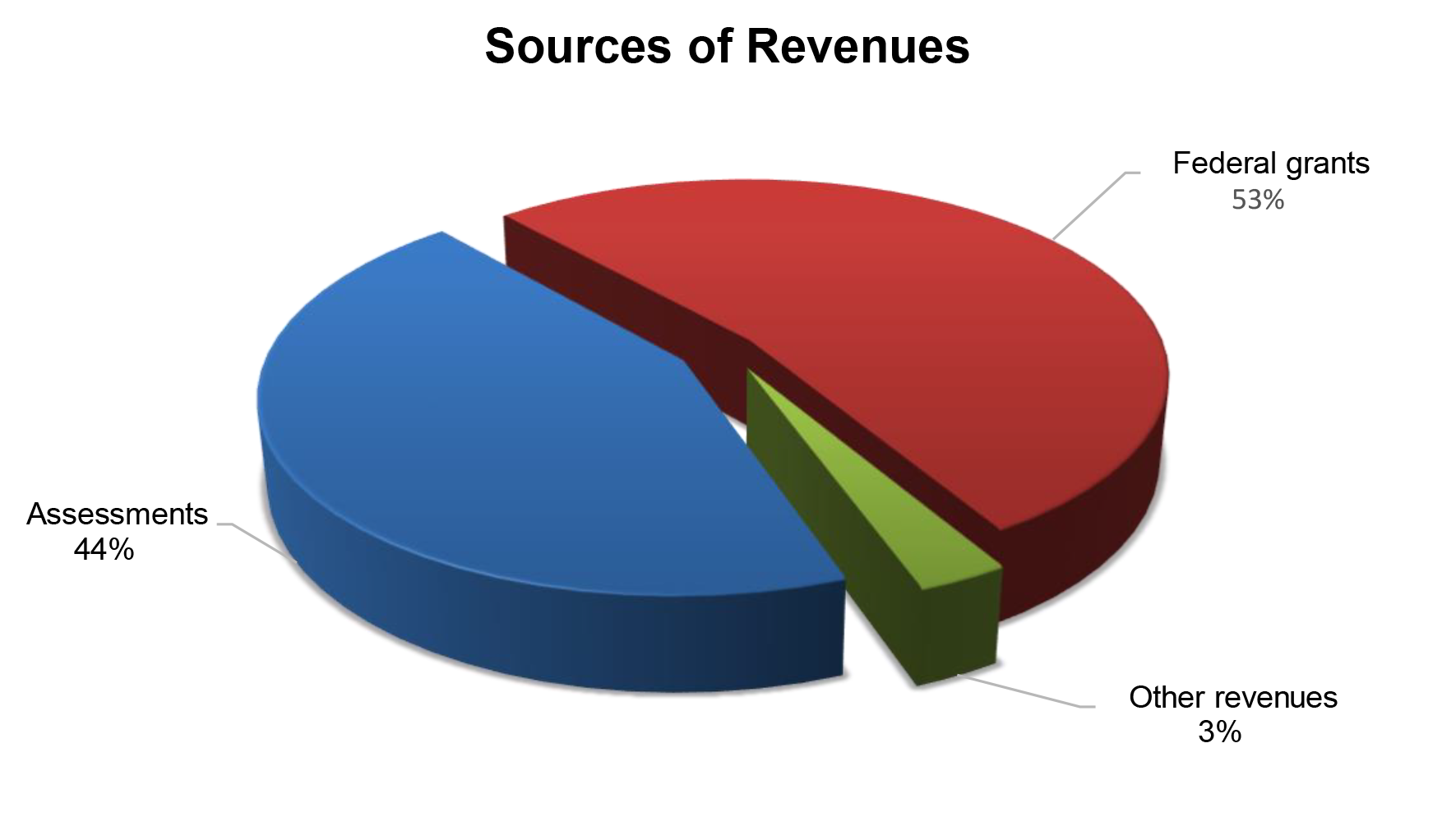

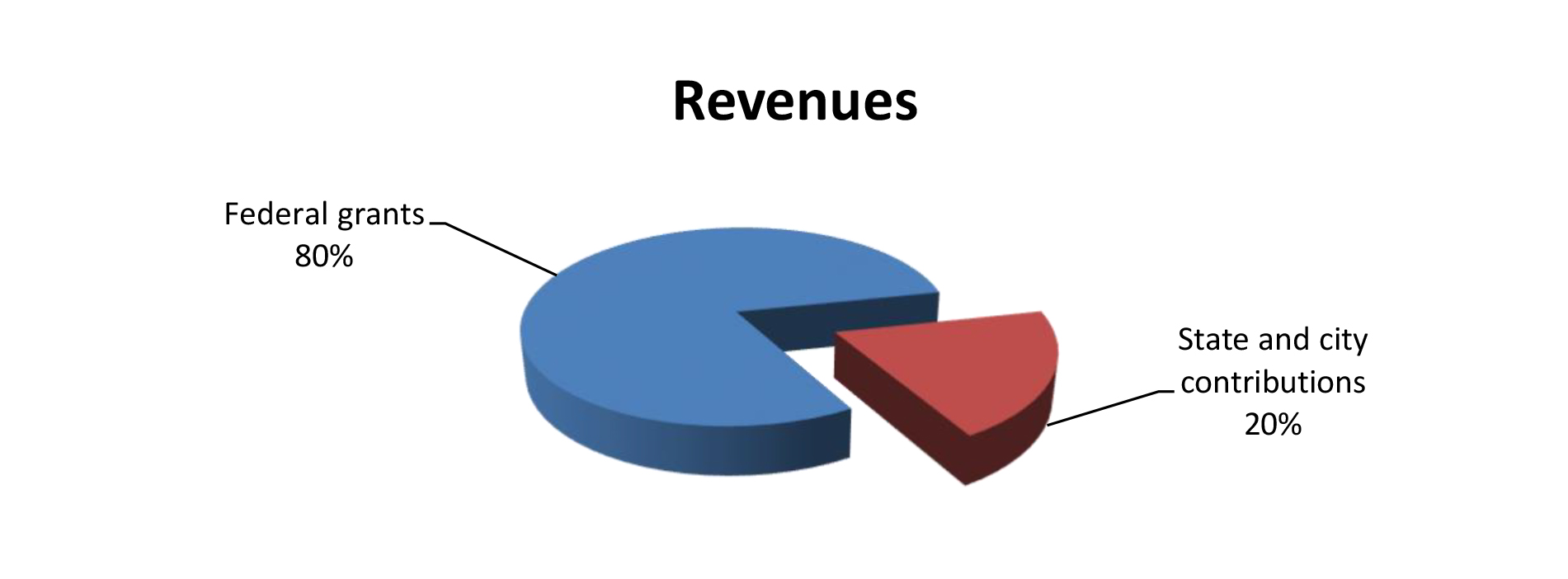

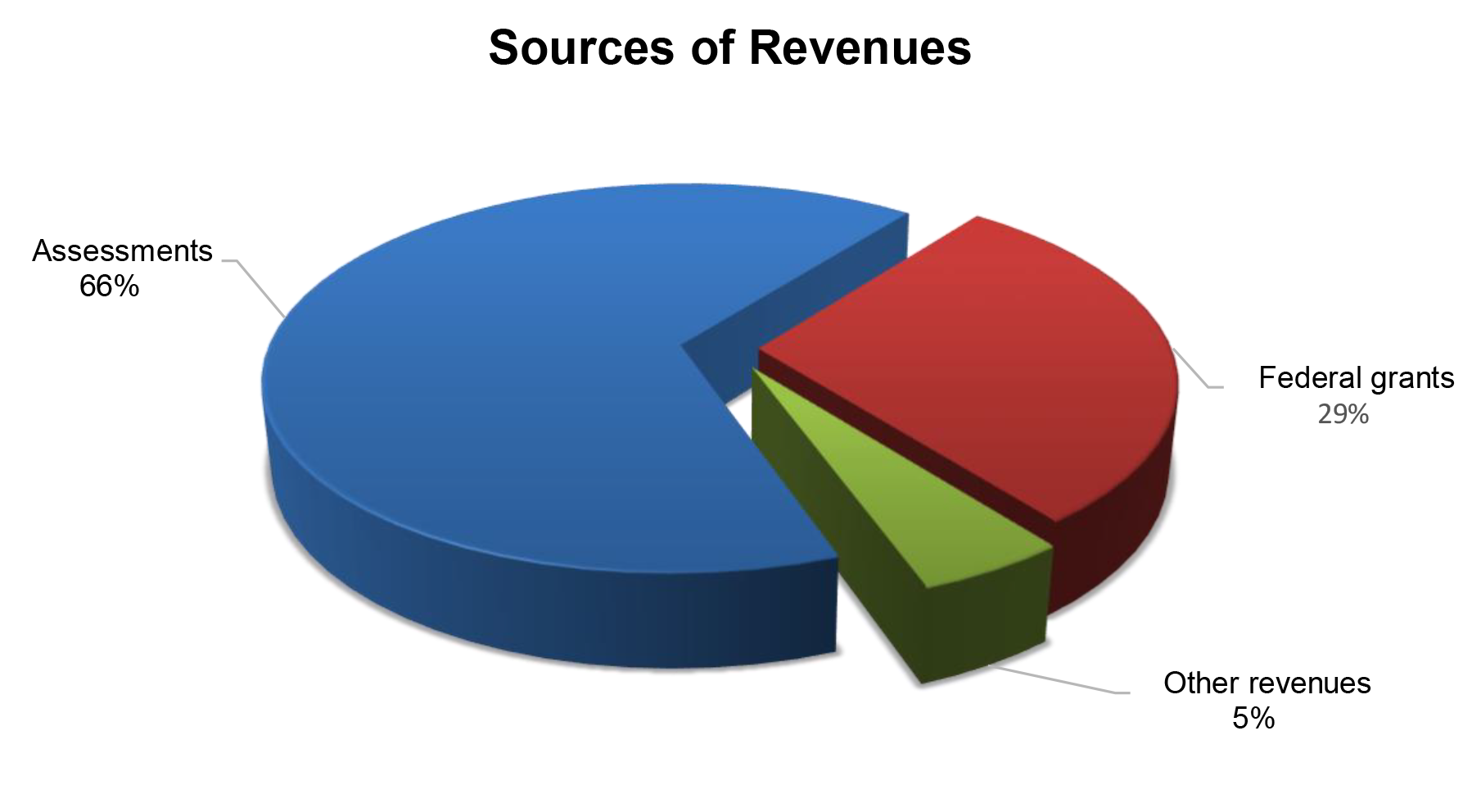

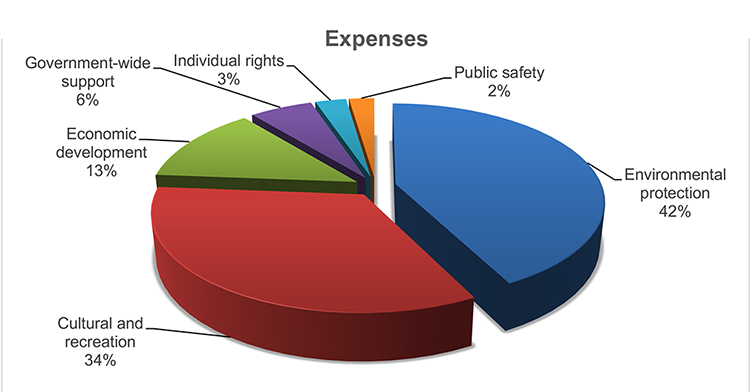

FOR THE FISCAL YEAR ended June 30, 2024, OahuMPO reported total revenues of approximately $4.4 million and total expenses of approximately $4.58 million, resulting in minimal change in net position. Revenues consisted of $3.55 million from federal grants, $842,000 in contributions from the State of Hawai‘i and City and County of Honolulu, and $10,000 from other sources.

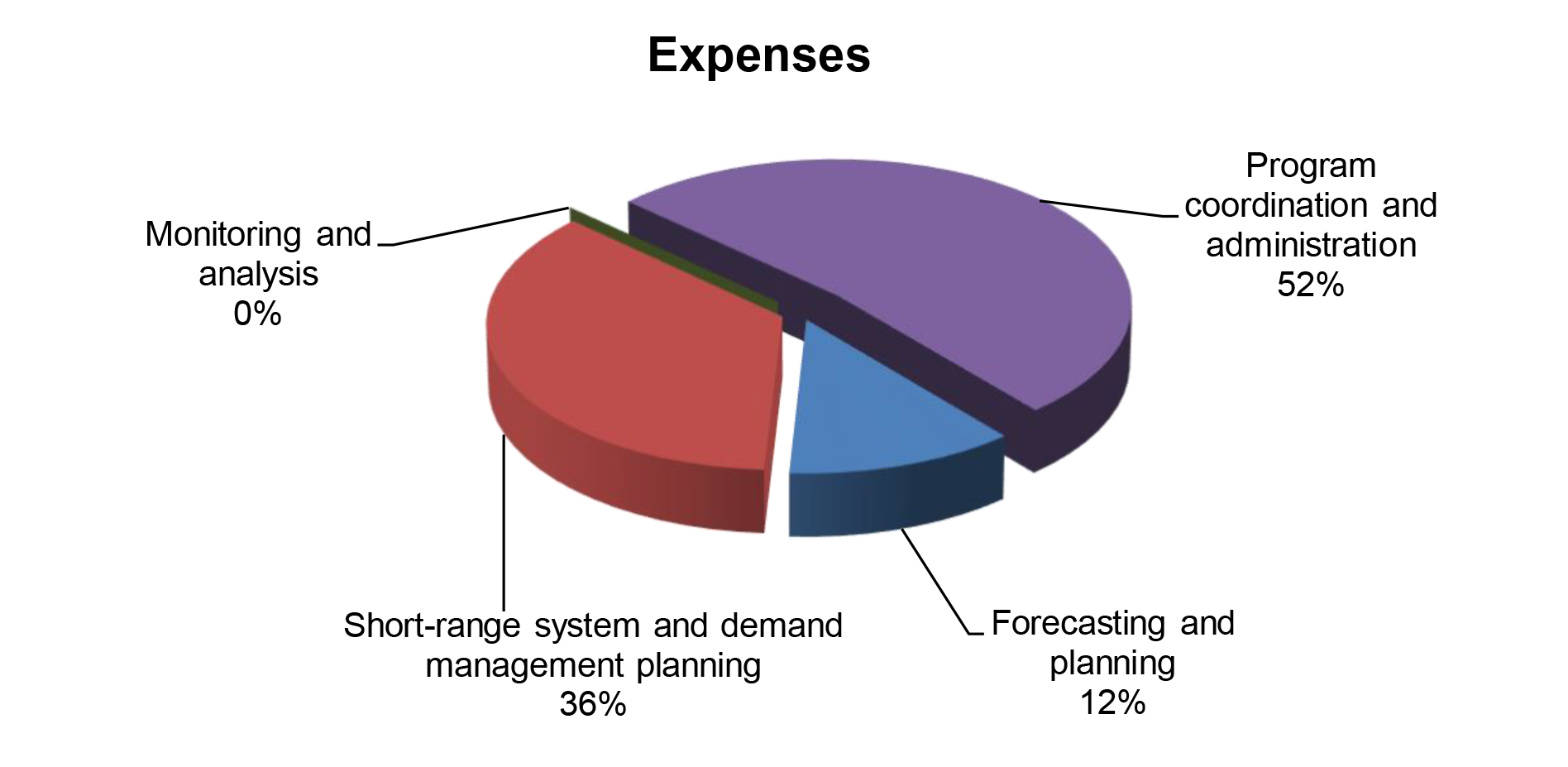

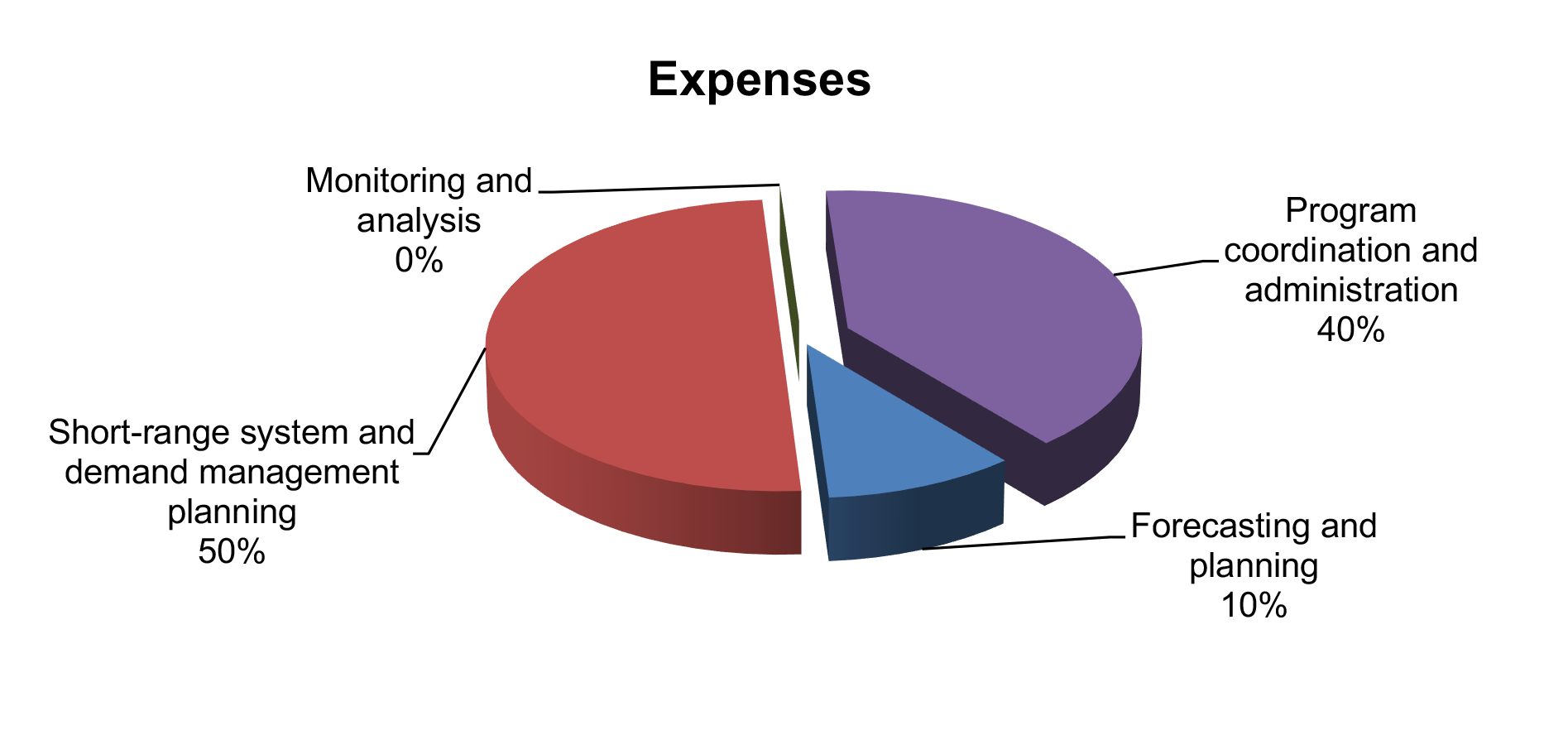

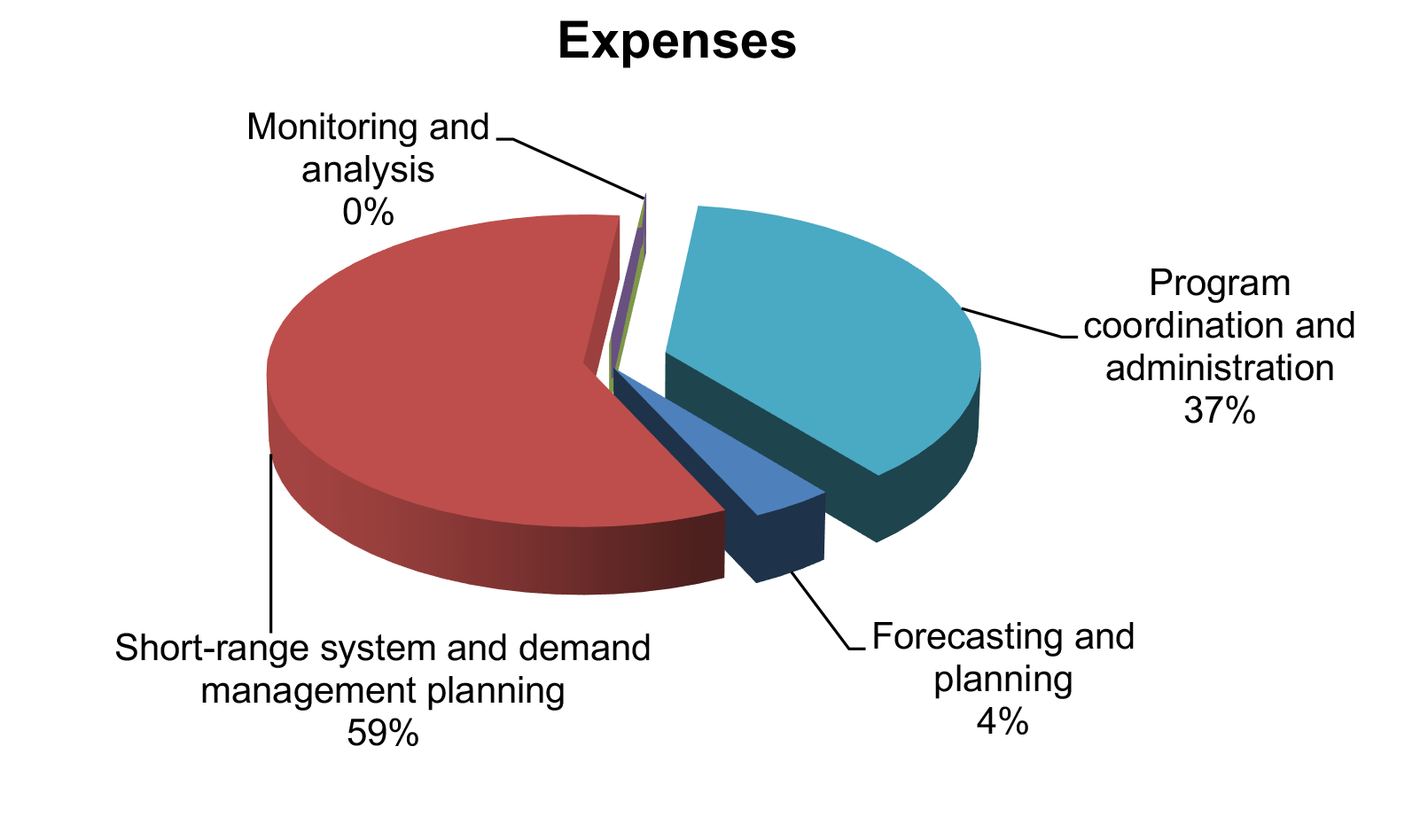

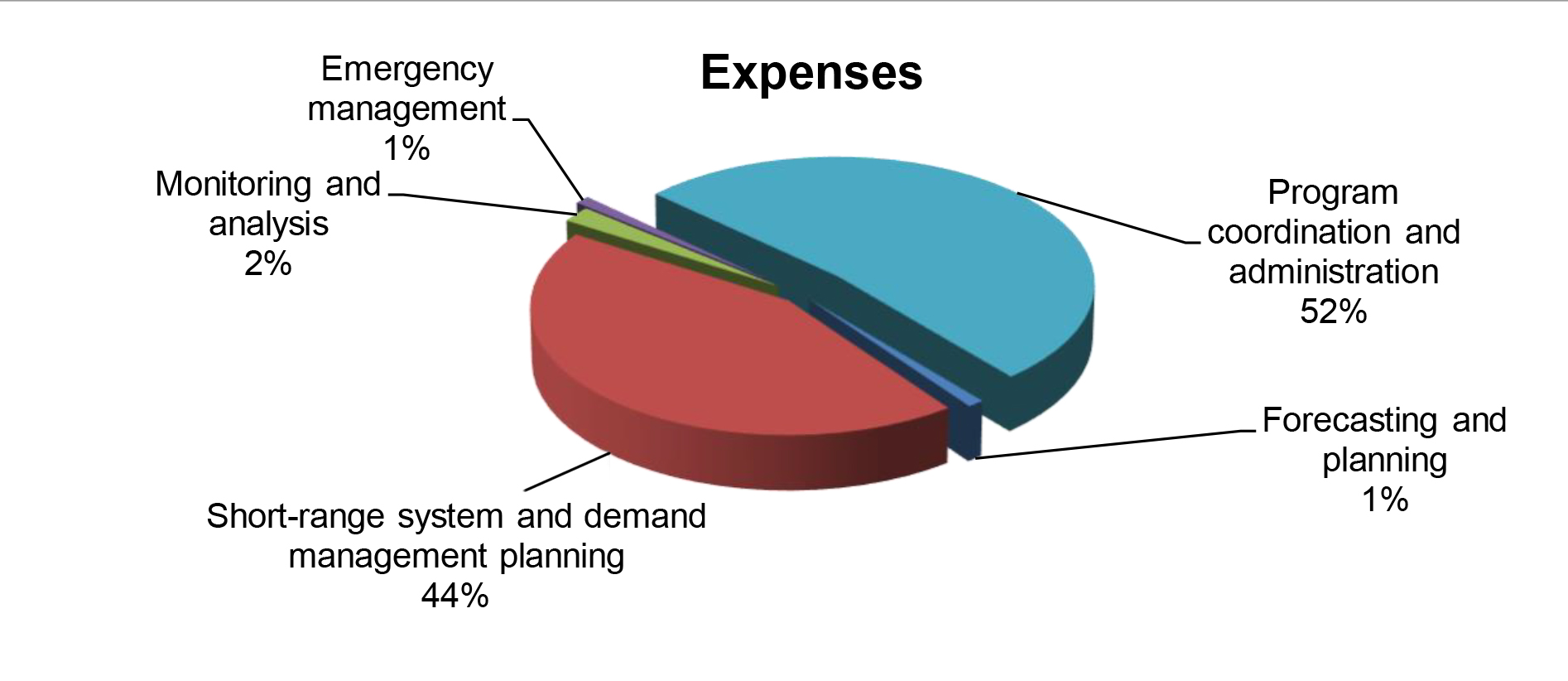

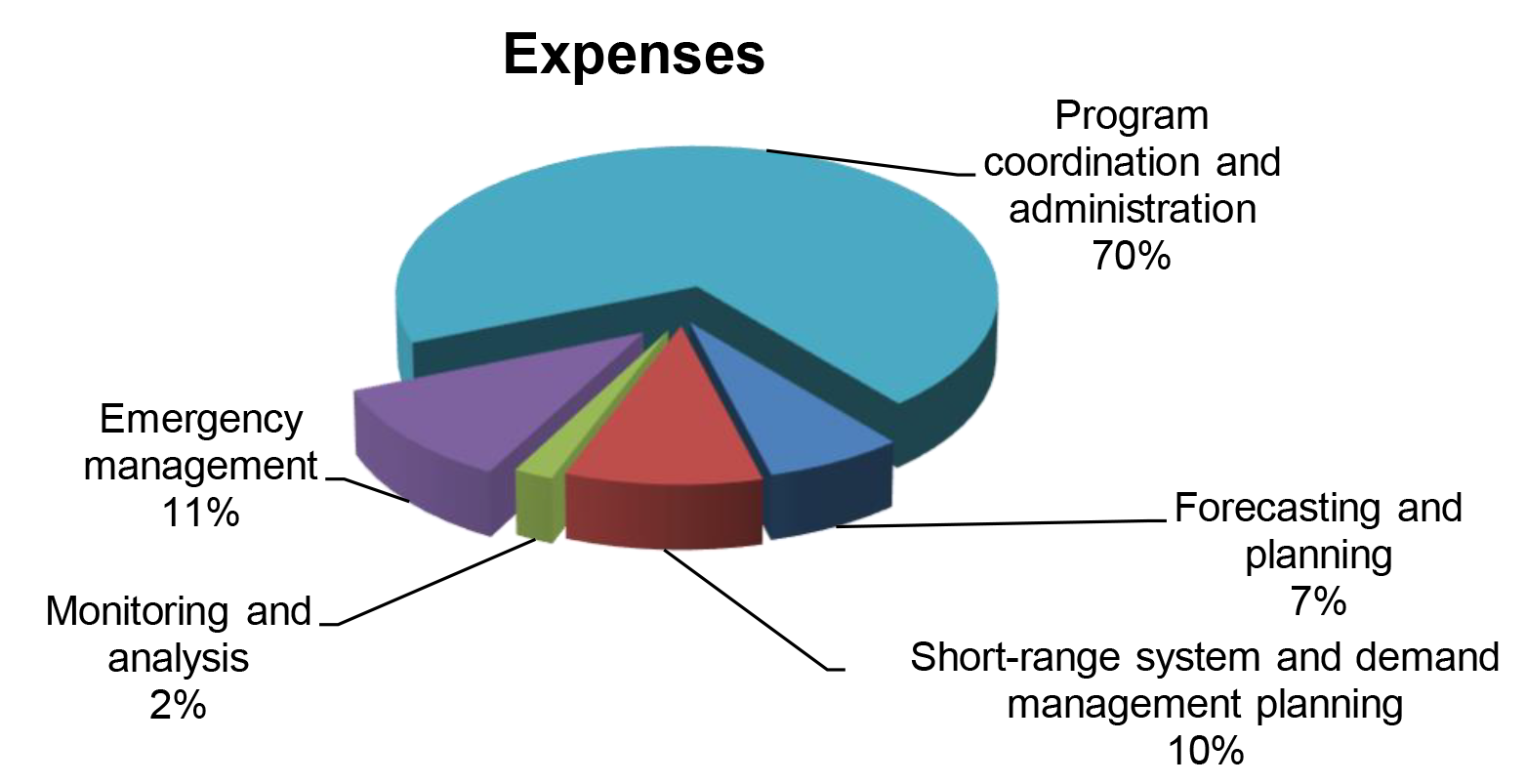

Total expenses consisted of (1) $540,000 for transportation forecasting and long-range planning; (2) $1.65 million for short-range transportation system and demand management planning; (3) $6,000 for transportation monitoring and analysis; and (4) $2.38 million for program coordination and administration.

As of June 30, 2024, total assets exceeded total liabilities by $317,000. Total assets of $1.99 million, included cash of $560,000, receivables and other assets of $1.39 million, and net capital assets of $39,000. Total liabilities were $1.68 million.

Auditors’ Opinion

OahuMPO RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles. OahuMPO also received an unmodified opinion on its compliance with major federal programs in accordance with the Uniform Guidance.

Findings

THERE WERE NO REPORTED DEFICIENCIES in internal control over financial reporting that were considered to be material weaknesses and no instances of noncompliance or other matters that were required to be reported under Government Auditing Standards. However, the auditors identified one significant deficiency that was required to be reported under Government Auditing Standards. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. The significant deficiency is described on page 45 of the report.

There were no findings that were considered material weaknesses in internal control over compliance in accordance with the Uniform Guidance.

About the Organization

Federal highway and transit statutes require urbanized areas greater than 50,000 in population to designate a metropolitan planning organization as a condition for spending federal highway or transit funds. O‘ahu Metropolitan Planning Organization (OahuMPO) is the designated metropolitan planning organization for the island of O‘ahu. OahuMPO was established by agreement between the Governor of the State of Hawai‘i and the Chairperson of the City Council of the City and County of Honolulu and serves as the decision-making body responsible for carrying out continuing, comprehensive, and cooperative transportation planning and programming for the island of O‘ahu.

Financial Statements, Fiscal Year Ended June 30, 2024

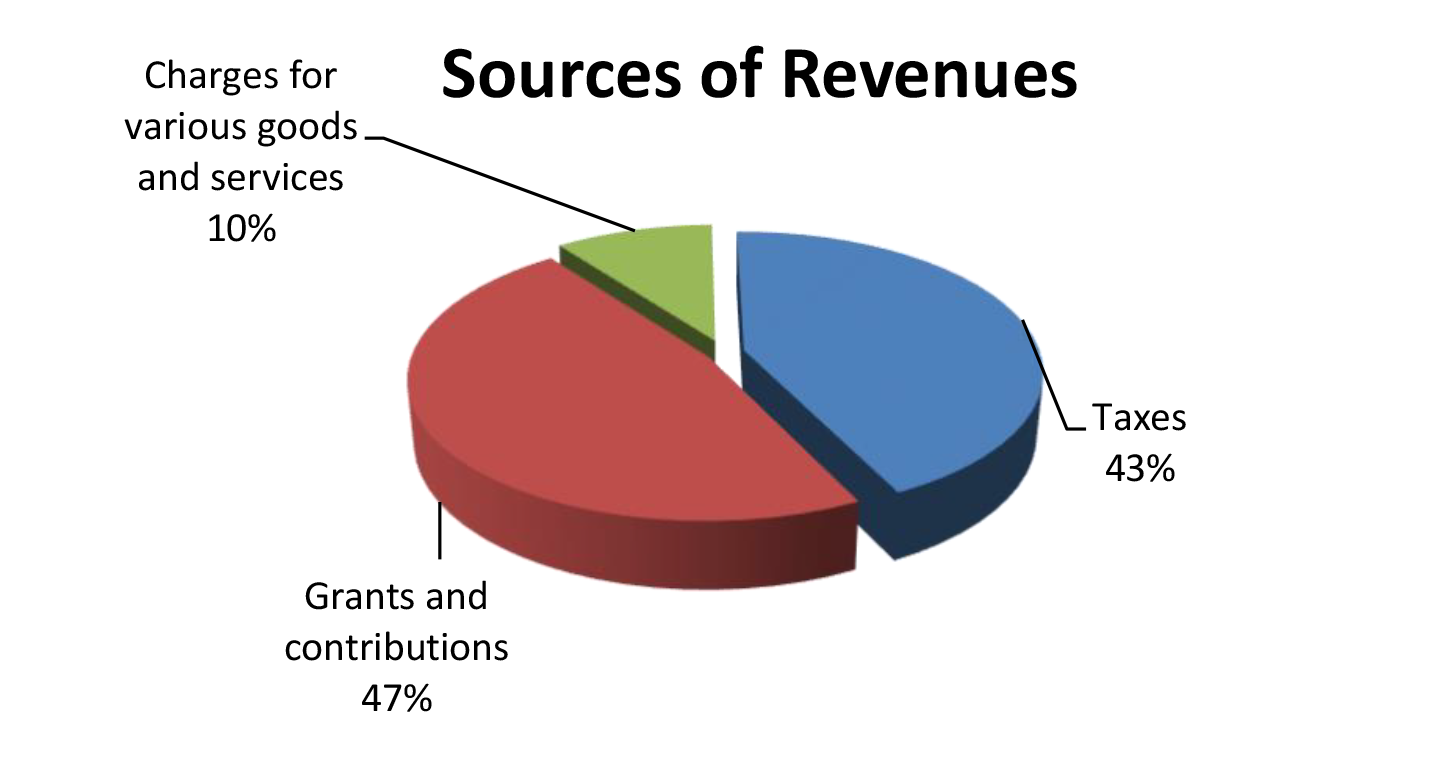

THE PRIMARY PURPOSE of the audit was to form an opinion on the fairness of the presentation of the State of Hawai‘i’s financial statements, as presented in the Annual Comprehensive Financial Report (ACFR) for the State of Hawai‘i, as of and for the fiscal year ended June 30, 2024. The audit was conducted by Accuity LLP. The ACFR was issued on March 30, 2025.

Financial Highlights

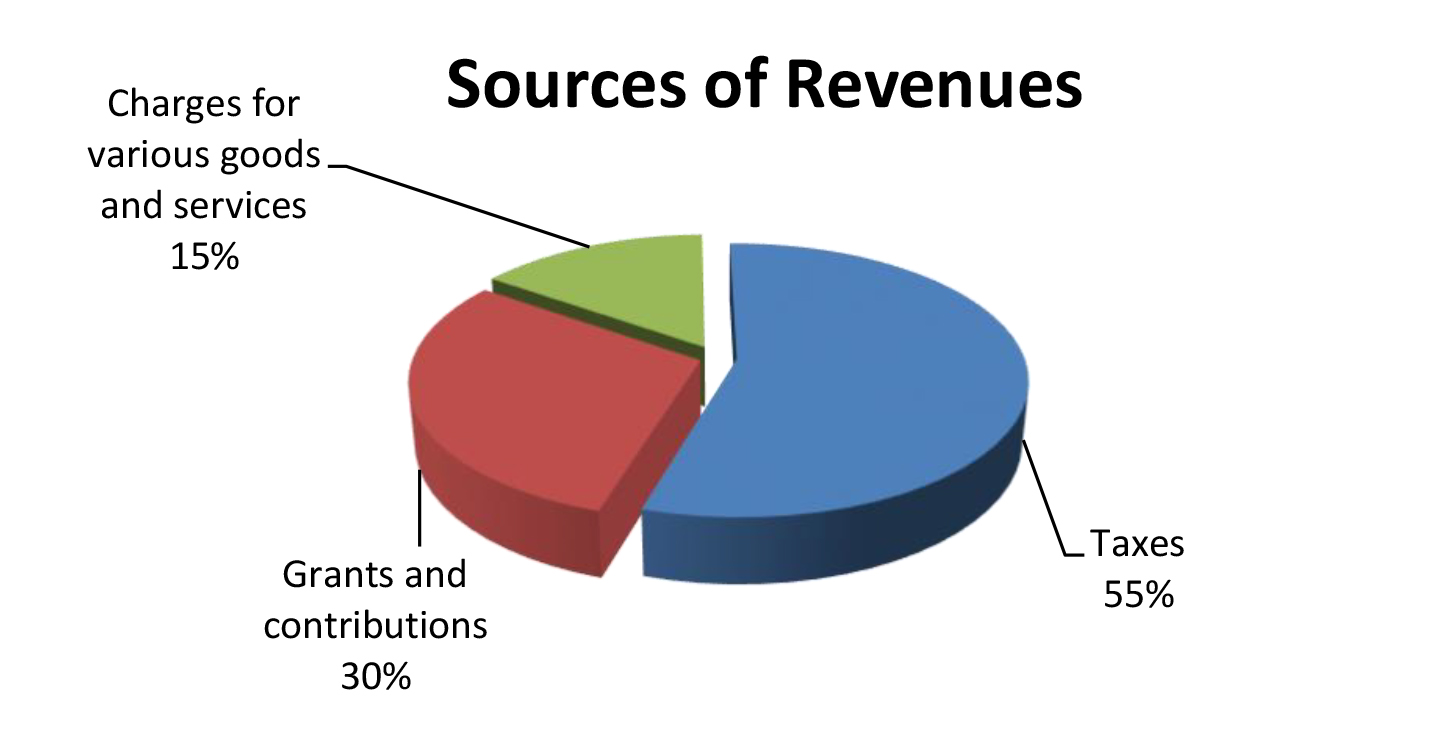

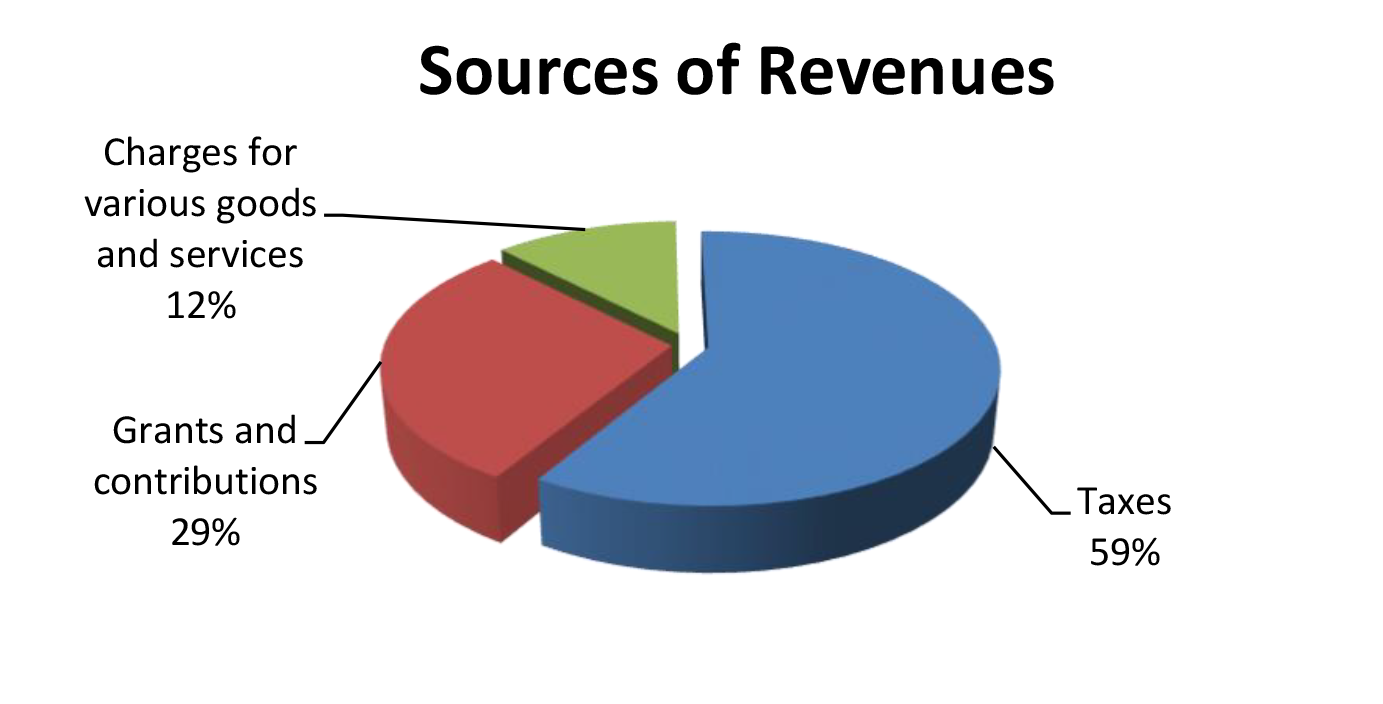

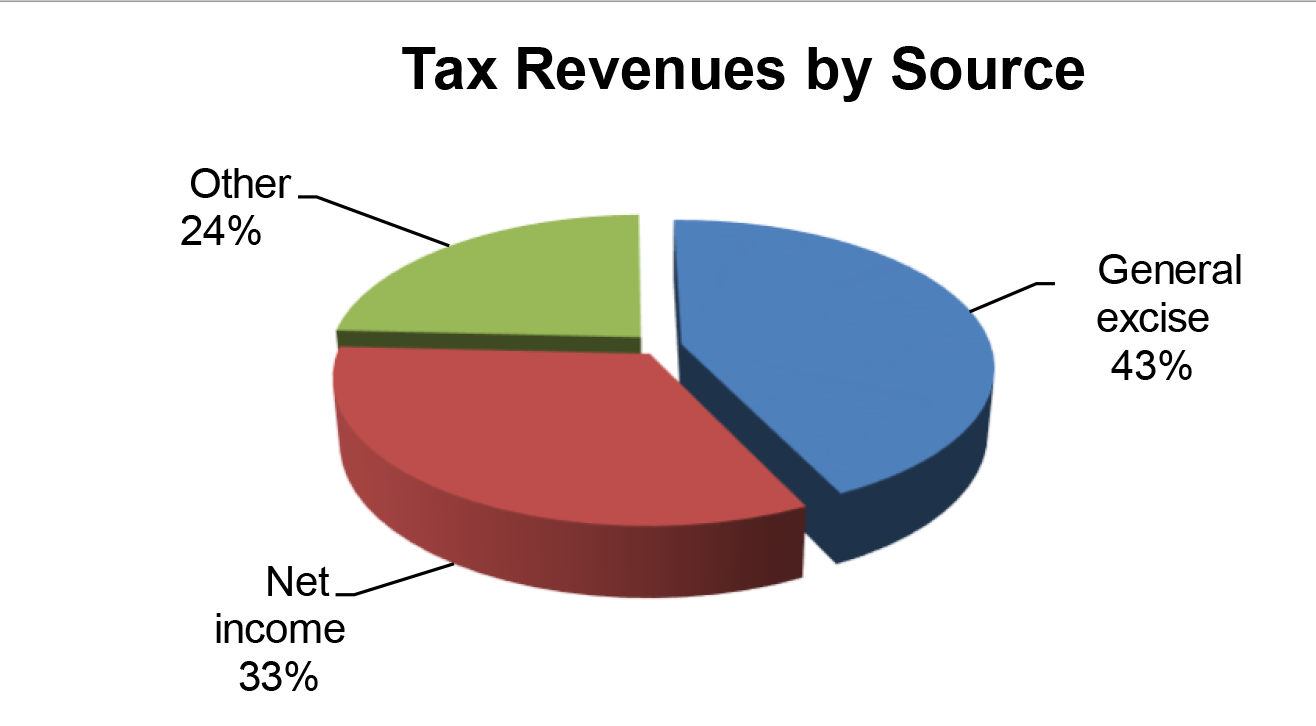

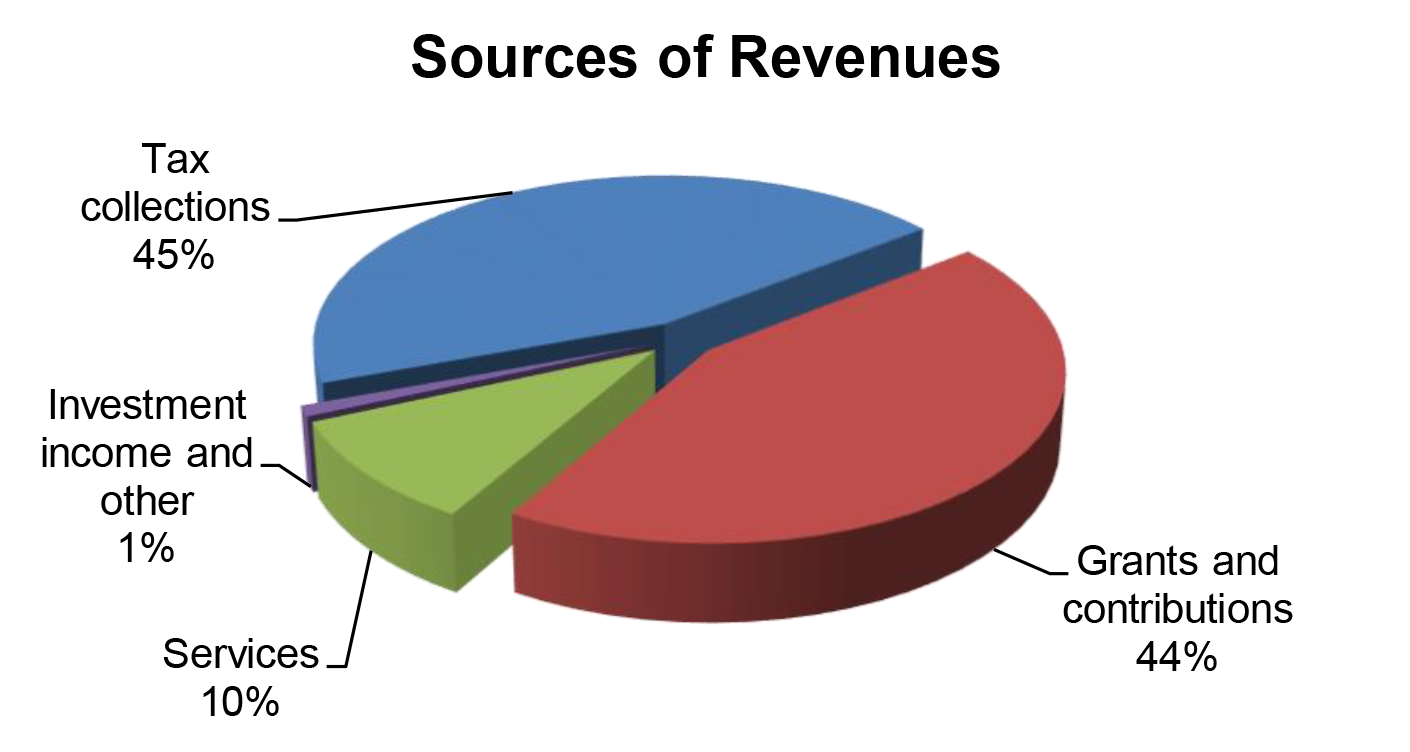

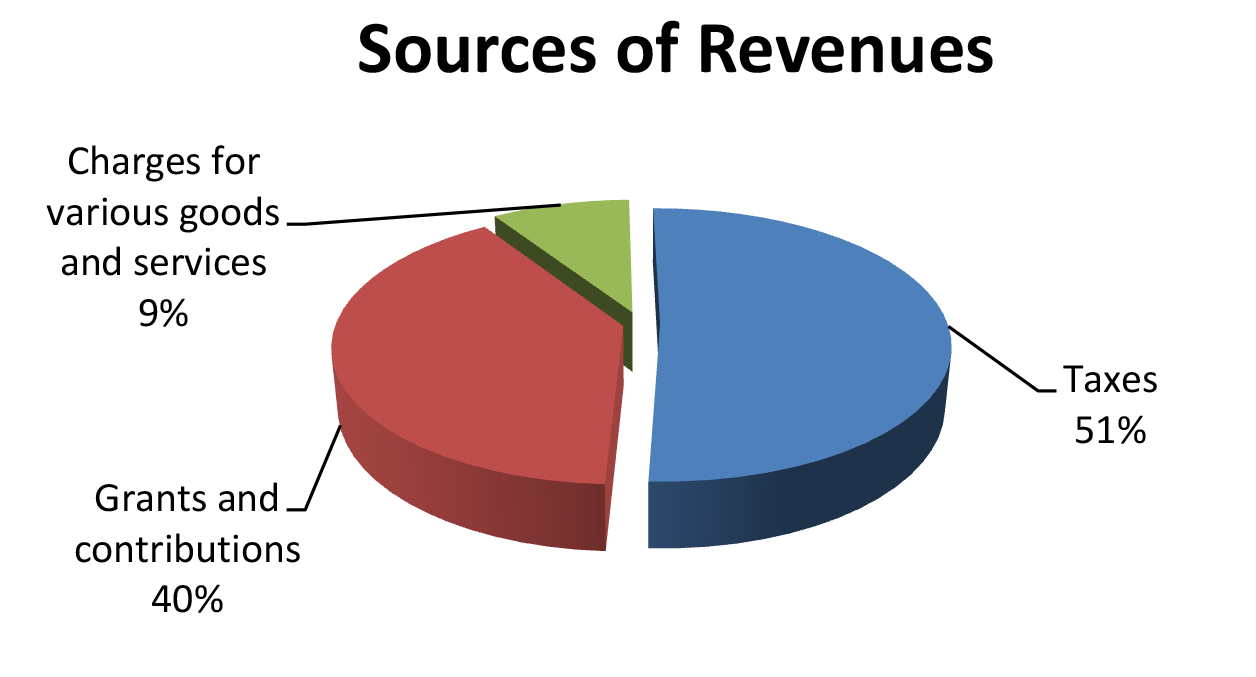

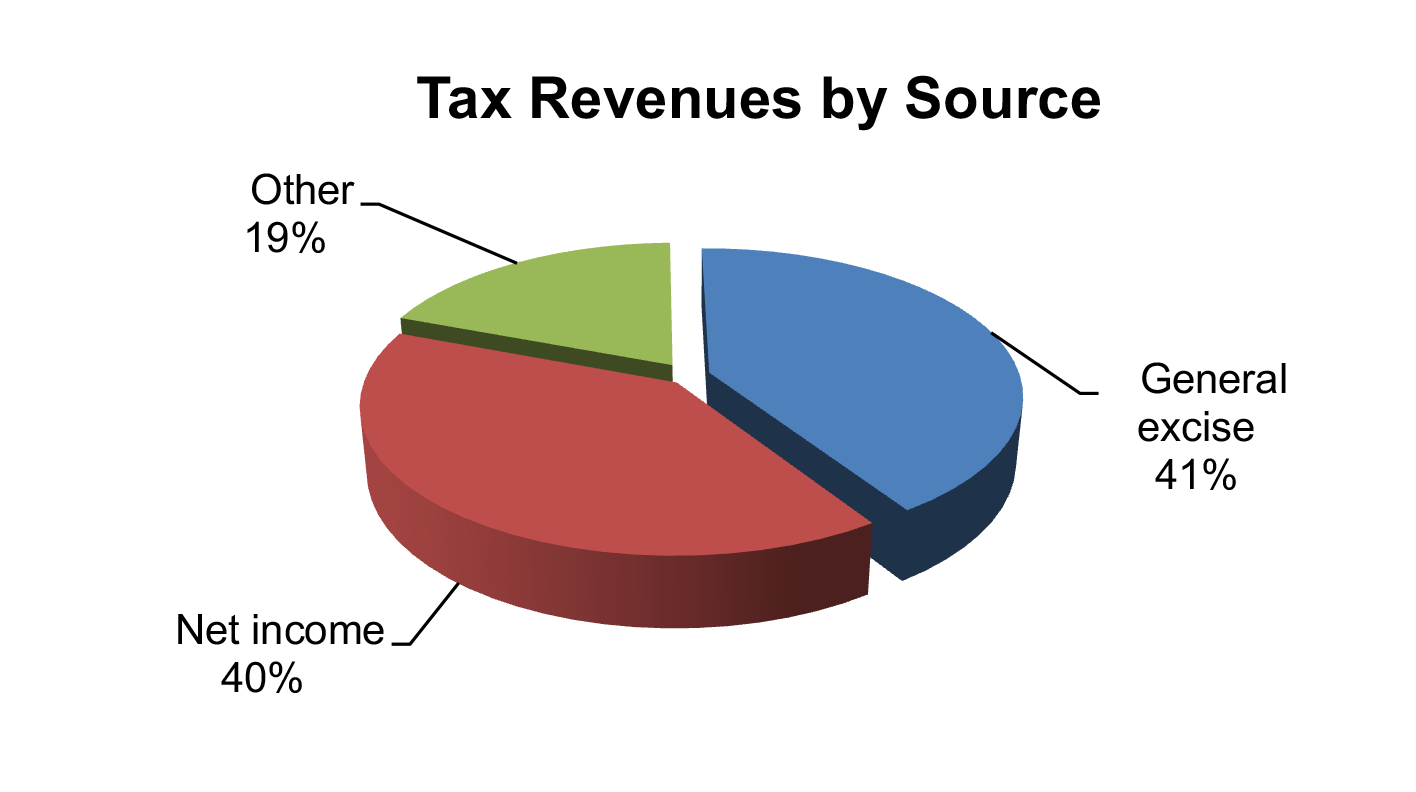

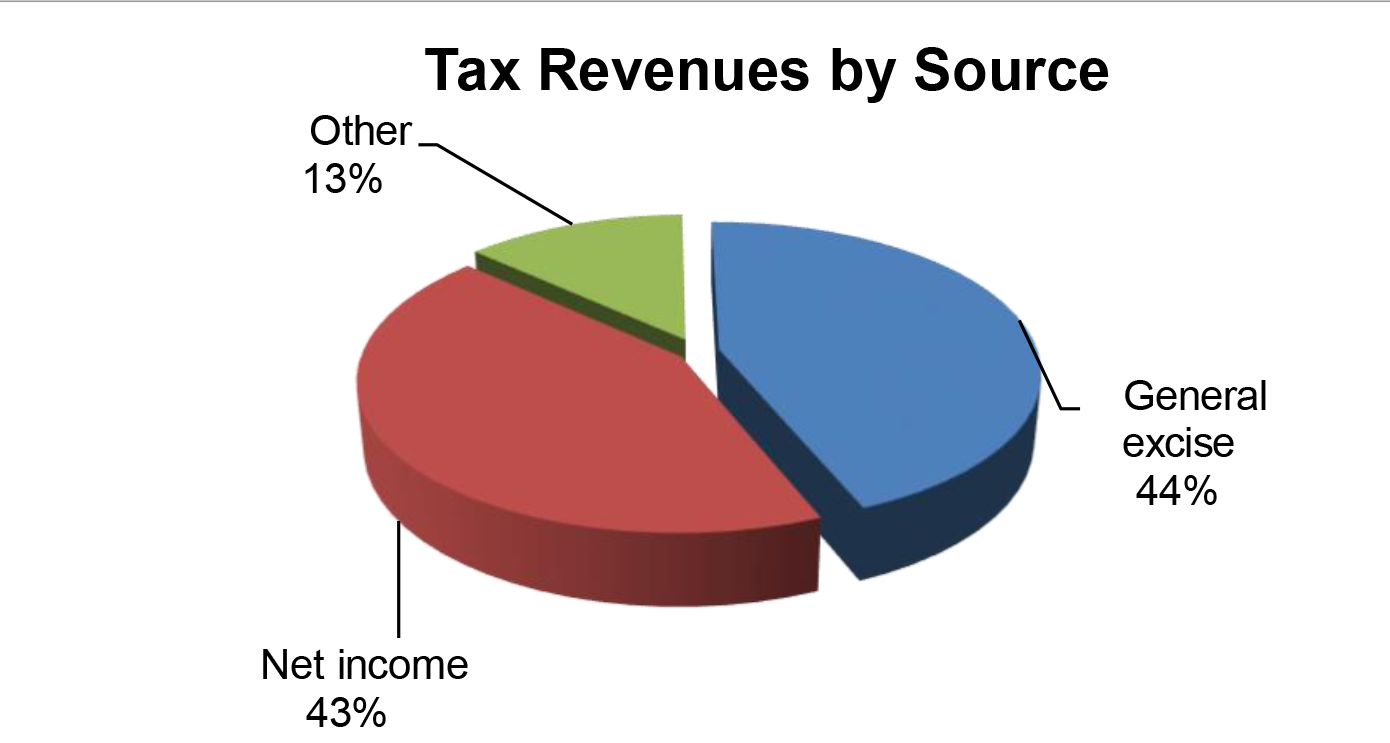

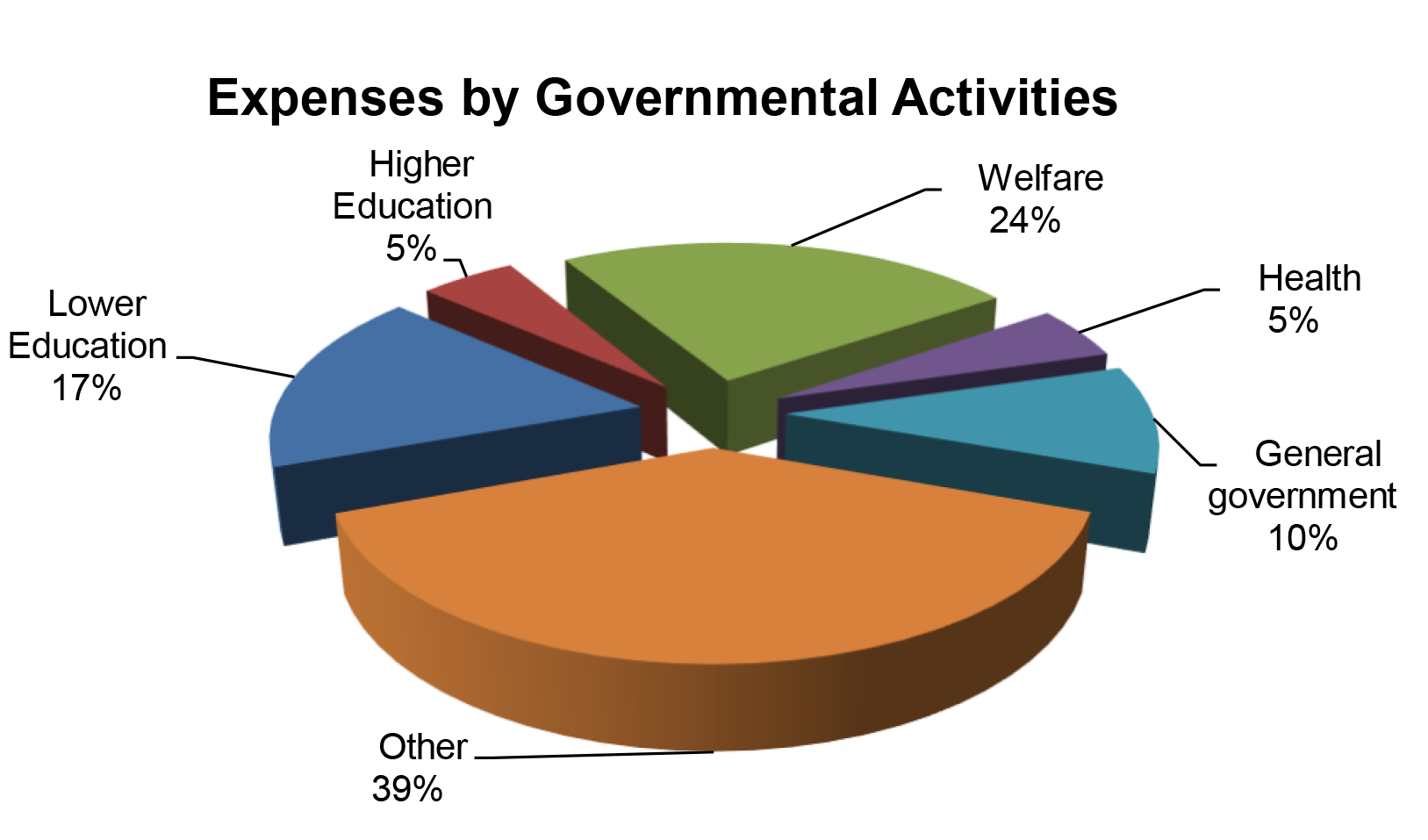

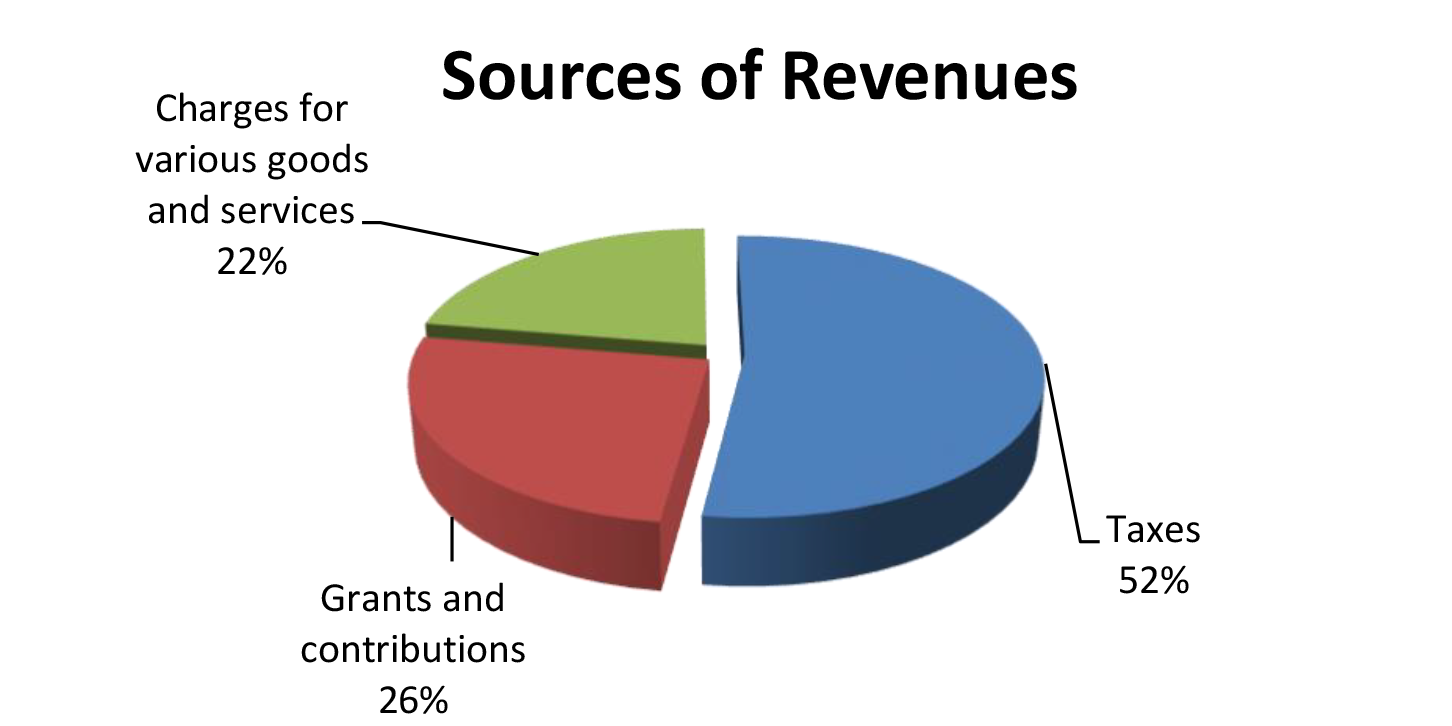

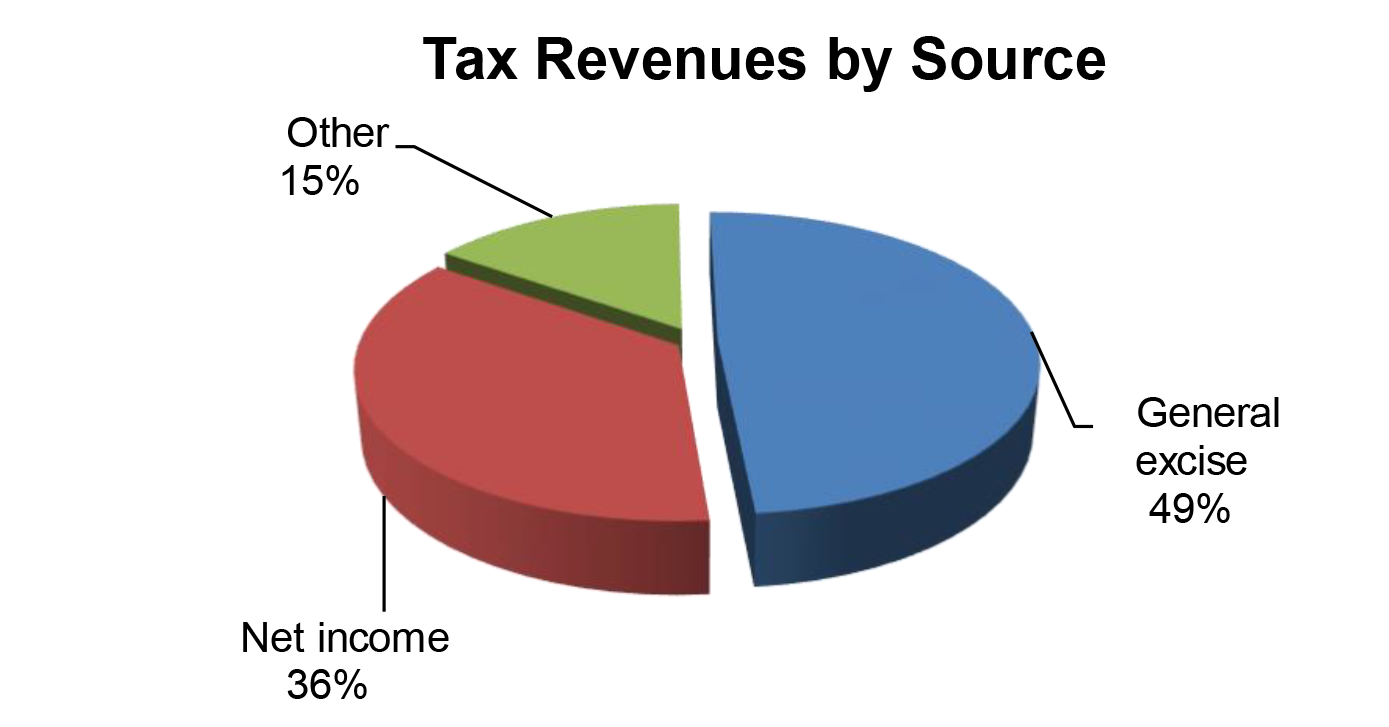

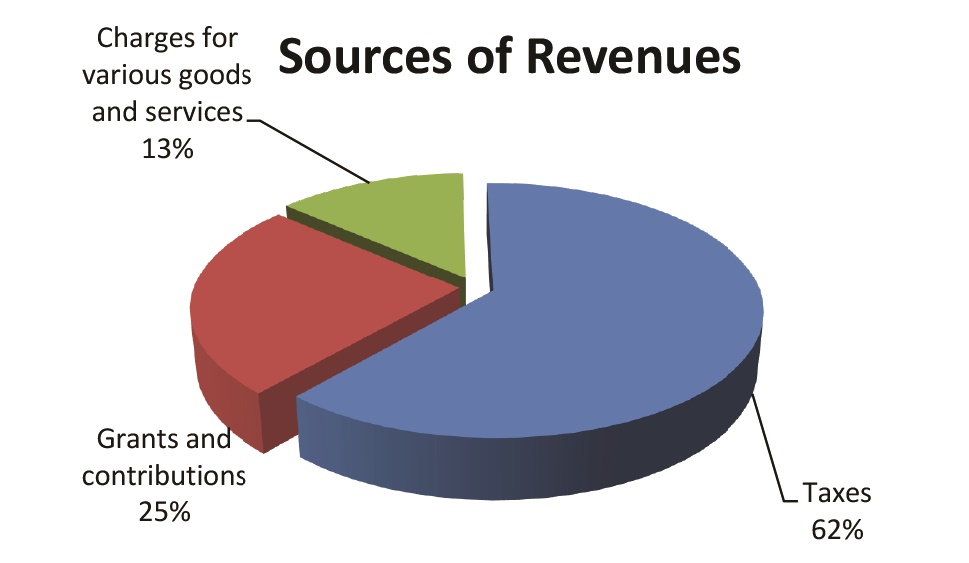

FOR THE FISCAL YEAR ended June 30, 2024, total revenues were $18.9 billion and total expenses were $17.6 billion, resulting in an increase in net position of $1.3 billion. Approximately 55 percent of the State of Hawai‘i’s total revenues came from taxes of $10.4 billion, 30 percent from grants and contributions of $5.7 billion, and 15 percent from charges for various goods and services of $2.8 billion.

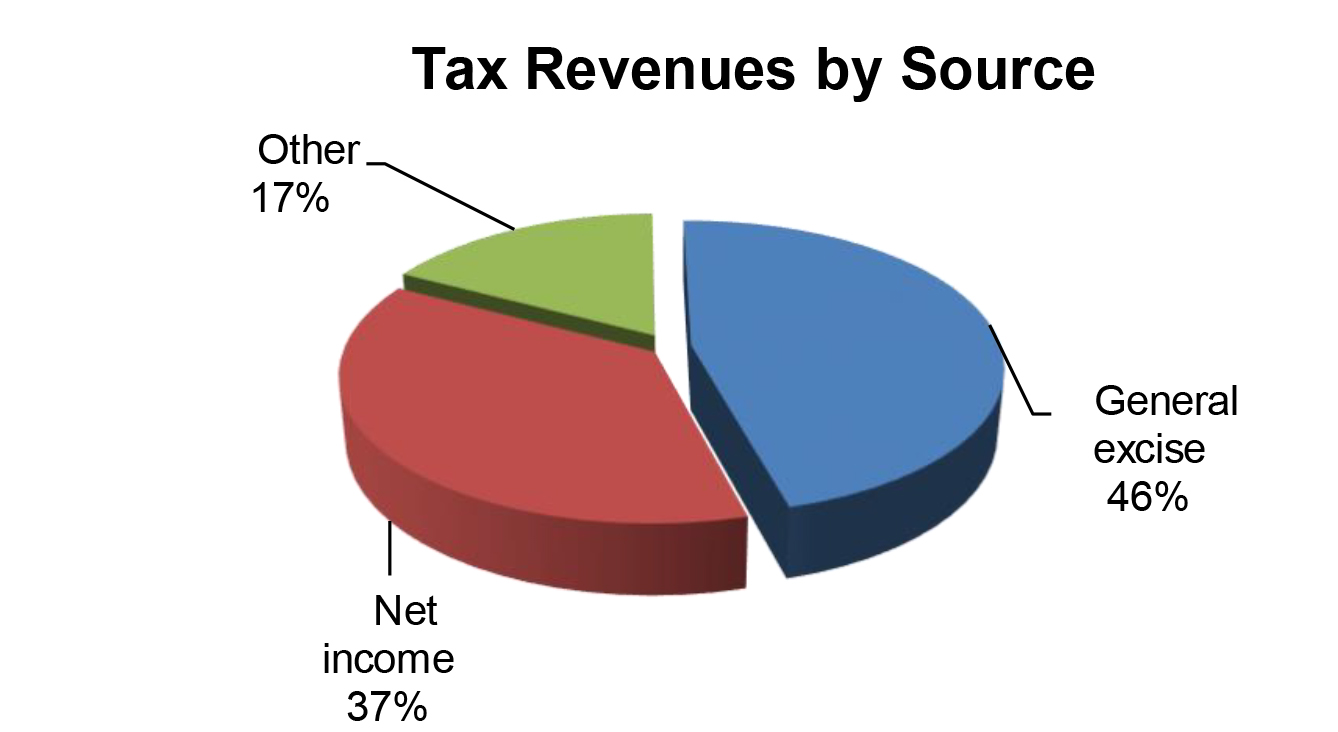

Total tax revenues of $10.4 billion consisted of general excise taxes of $4.8 billion, net income taxes of $3.8 billion, and other taxes of $1.8 billion.

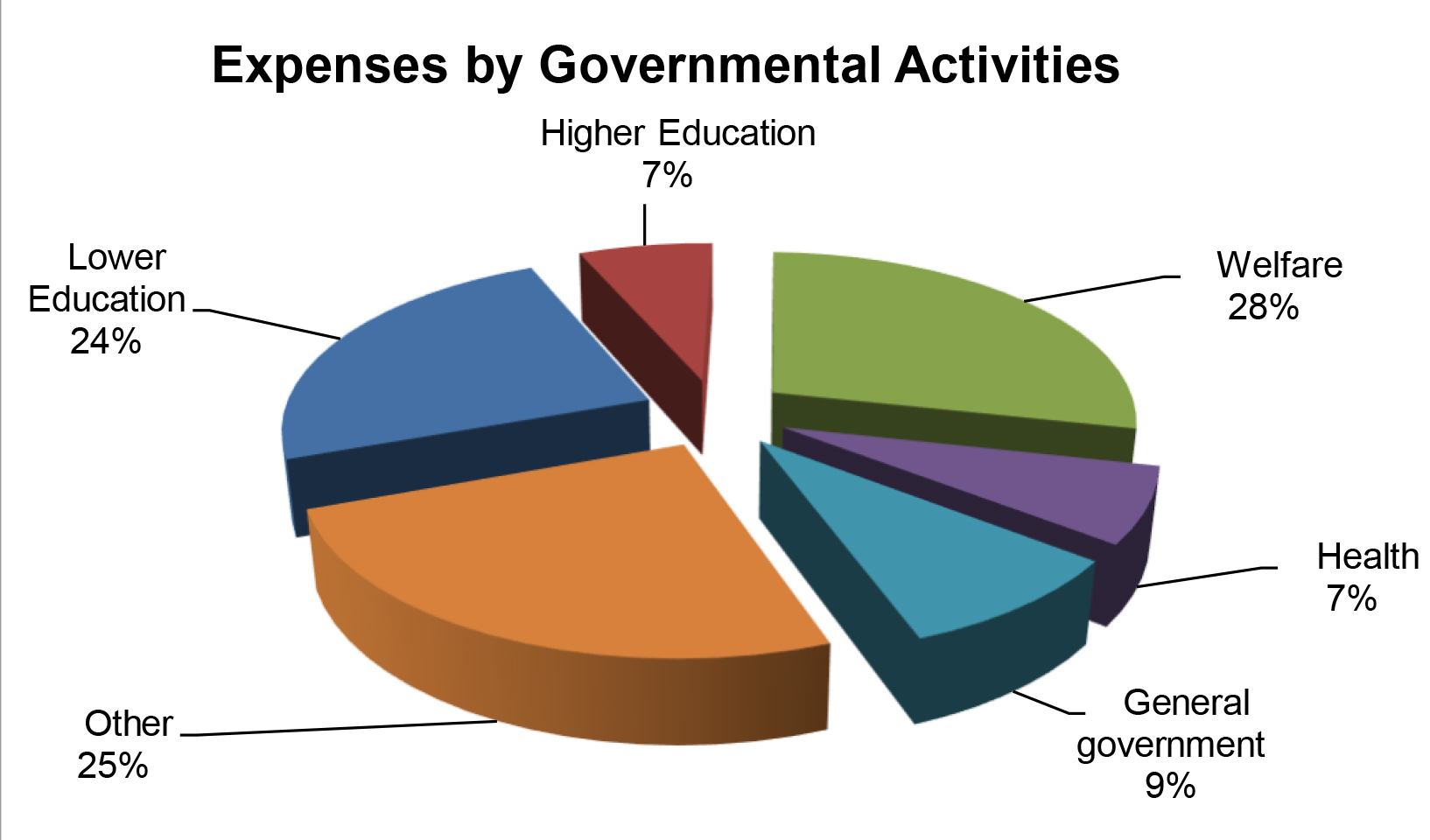

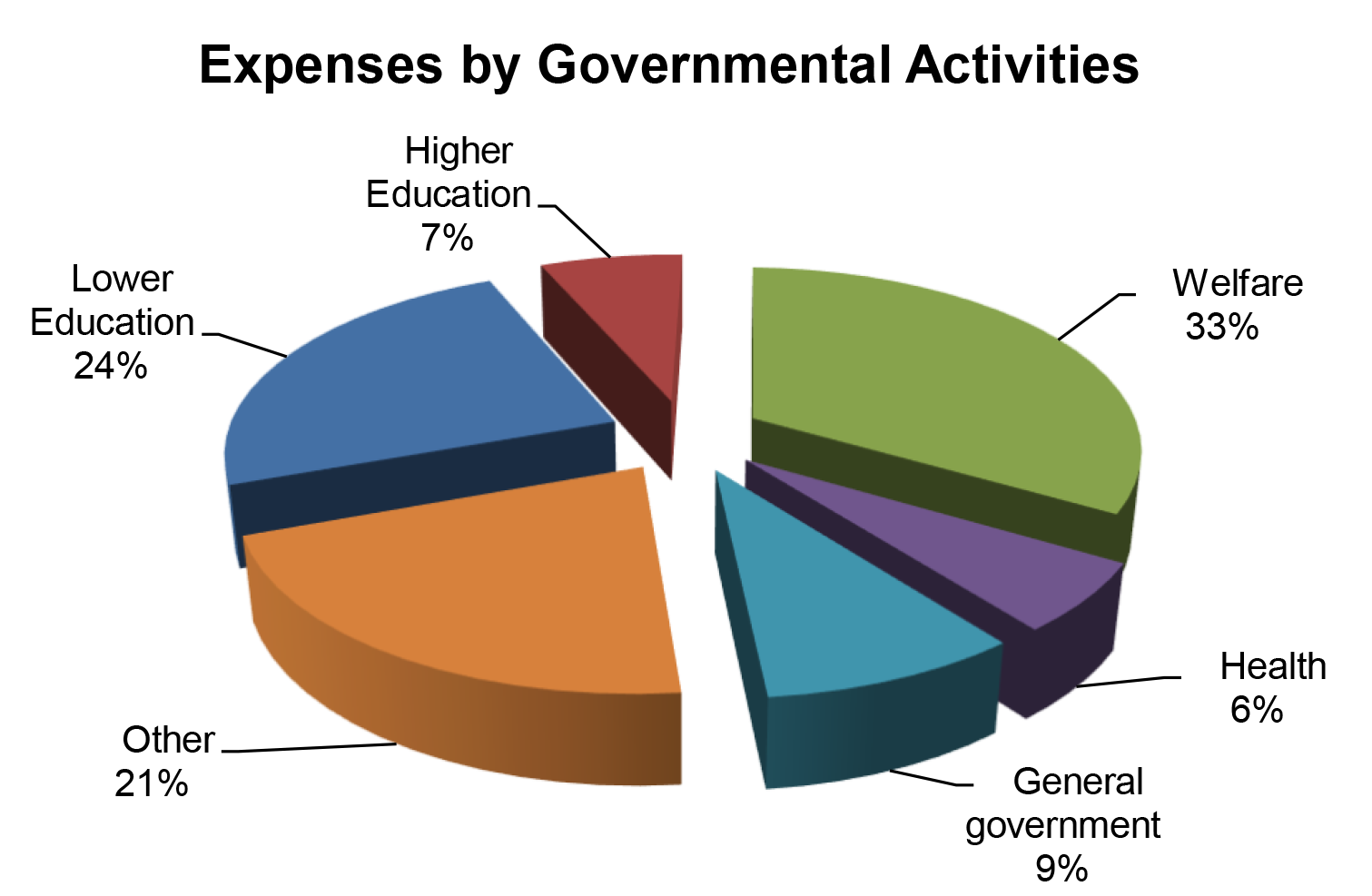

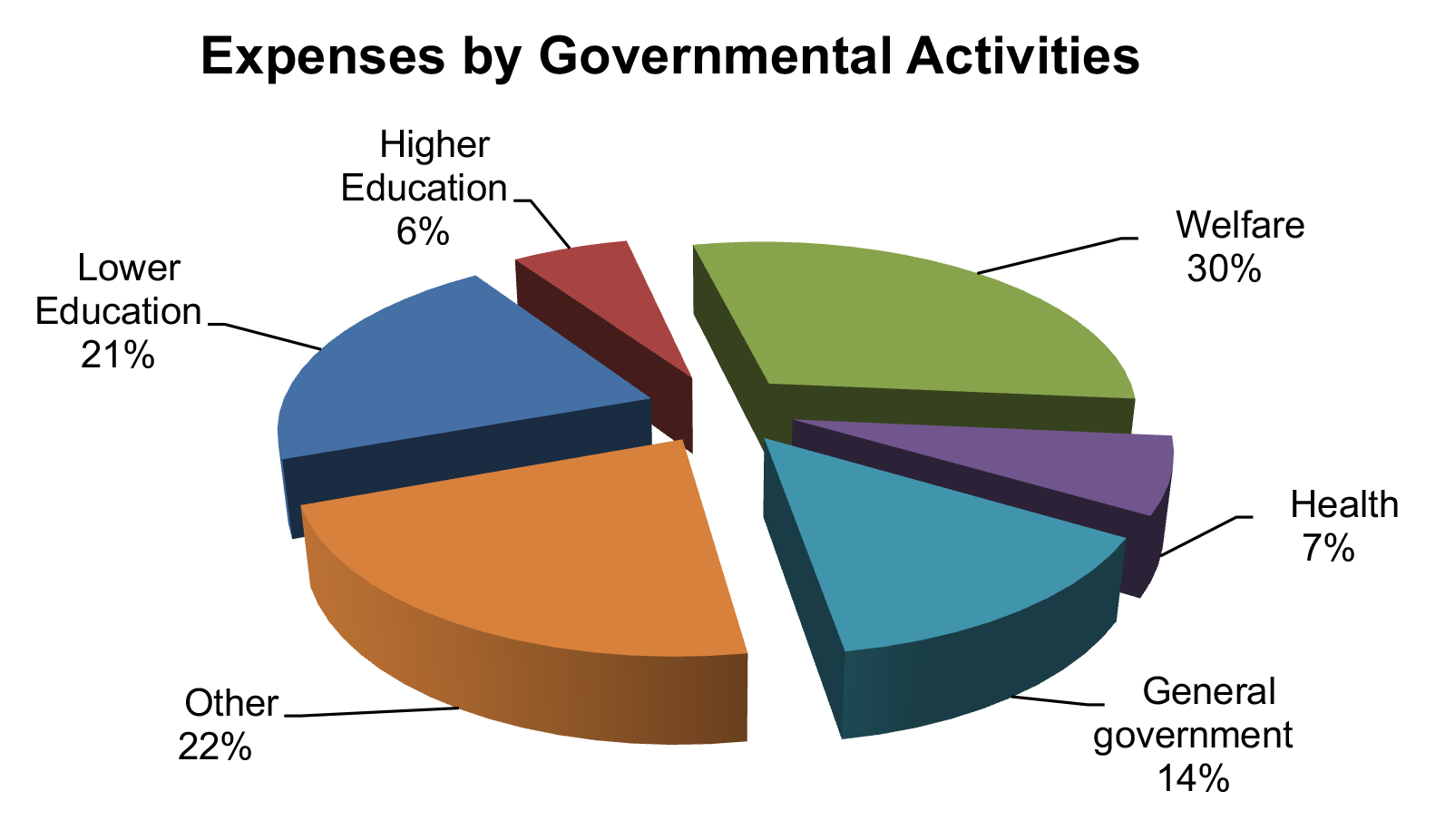

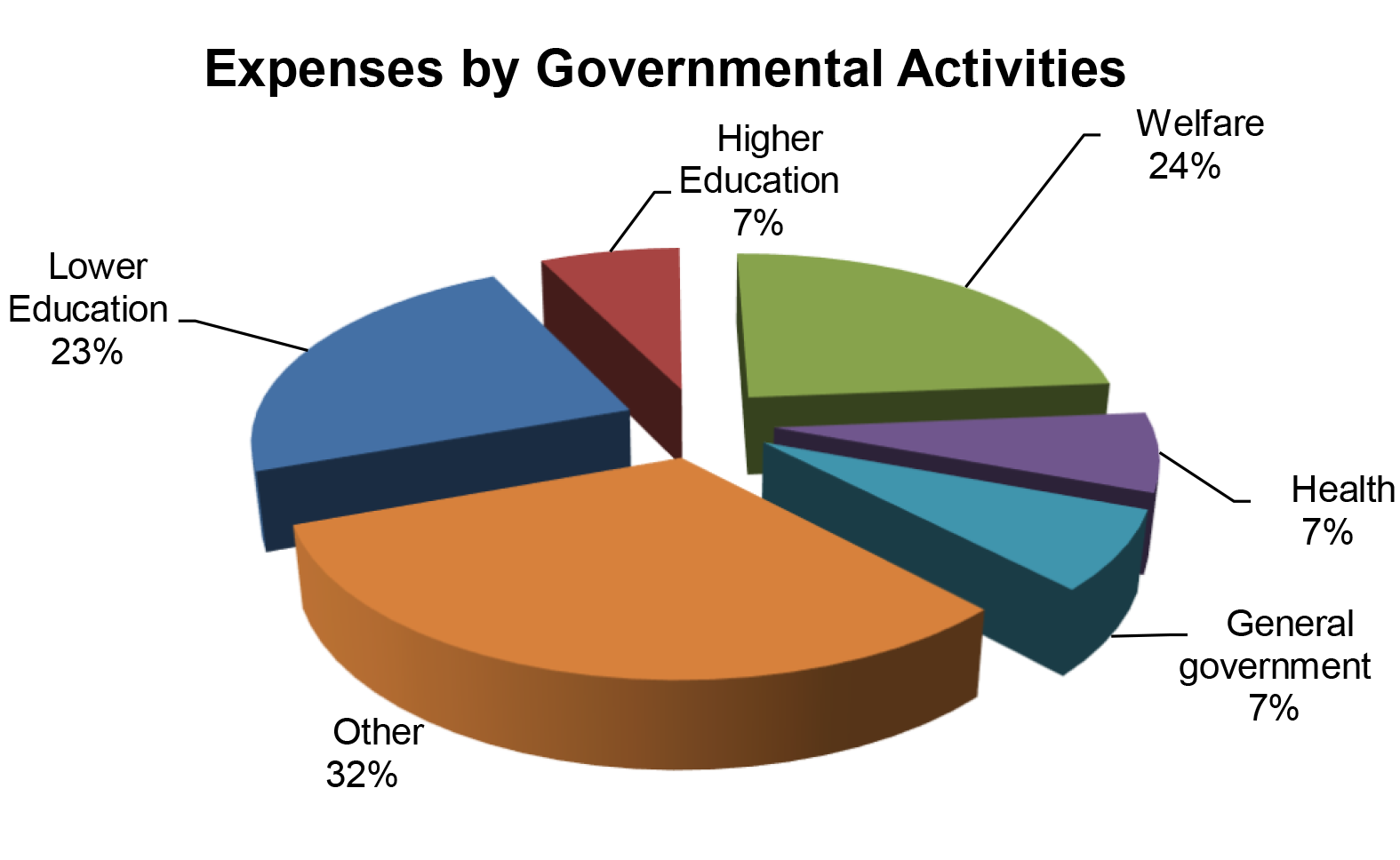

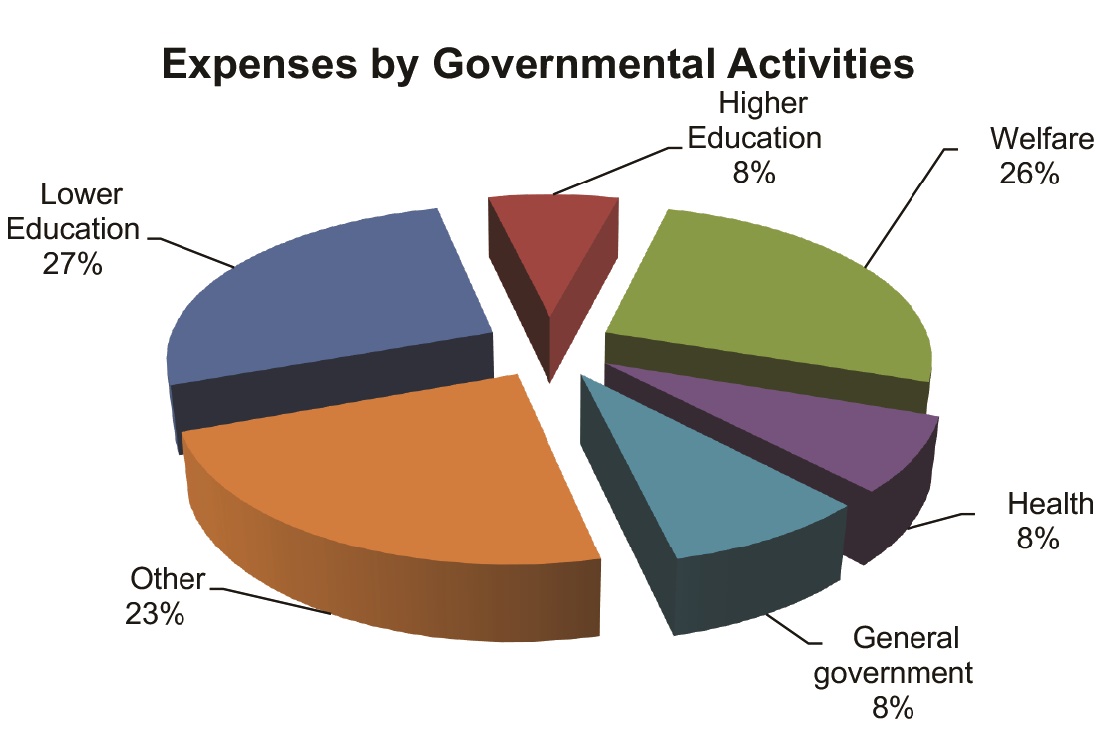

The largest expenses were for welfare at $4.9 billion, lower education at $4.2 billion, higher education at $1.1 billion, health at $1.3 billion, and general government at $1.5 billion. Other expenses totaled $4.6 billion.

As of June 30, 2024, total assets and deferred outflows of resources of $33.8 billion exceeded total liabilities and deferred inflows of resources of $31 billion, resulting in a net position of $2.8 billion. Of this amount, $4.1 billion was for the State’s net investment in capital assets, $2.1 billion was restricted for specific programs, and a negative $3.4 billion was unrestricted assets.

As of June 30, 2024, total assets and deferred outflows of resources of $33.8 billion were comprised of (1) net capital assets of $16.2 billion, (2) investments of $7.9 billion, (3) cash of $3 billion, (4) receivables of $2.2 billion, (5) restricted assets of $1.4 billion, and (6) other assets and deferred outflows of resources of $3.1 billion. Total liabilities and deferred inflows of resources of $31 billion were comprised of (1) general obligation and revenue bonds payable of $12.2 billion, (2) vacation and retirement benefits of $12.2 billion, and (3) other liabilities and deferred inflows of resources of $6.6 billion.

Auditors’ Opinion THE STATE OF HAWAI‘I RECEIVED AN UNMODIFIED OPINION that its financial statements were presented fairly, in all material respects, in accordance with generally accepted accounting principles.

About the State

THE STATE OF HAWAI‘I is mandated by statute to provide a range of services in the areas of education (both lower and higher), welfare, transportation (including highways, airports, and harbors), health, hospitals, public safety, housing, culture and recreation, economic development, and conservation of natural resources.

Financial Statements, Fiscal Year Ended June 30, 2024

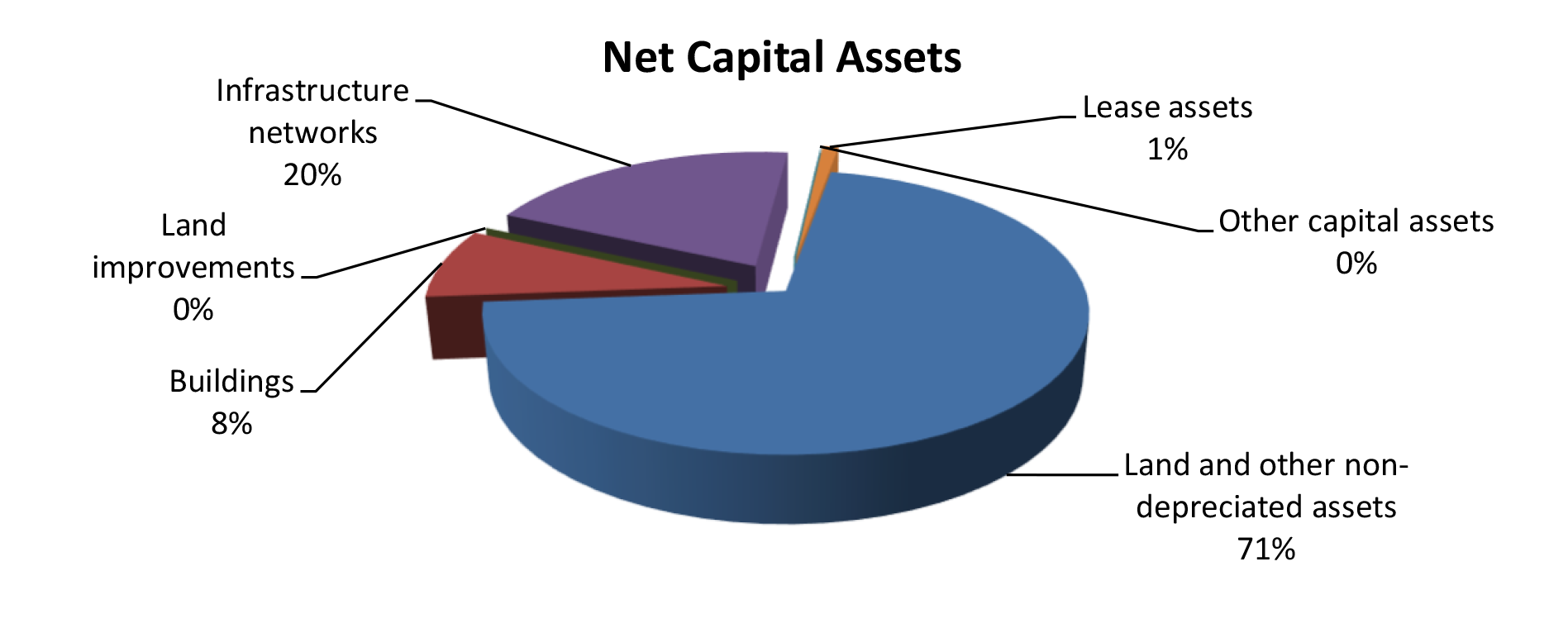

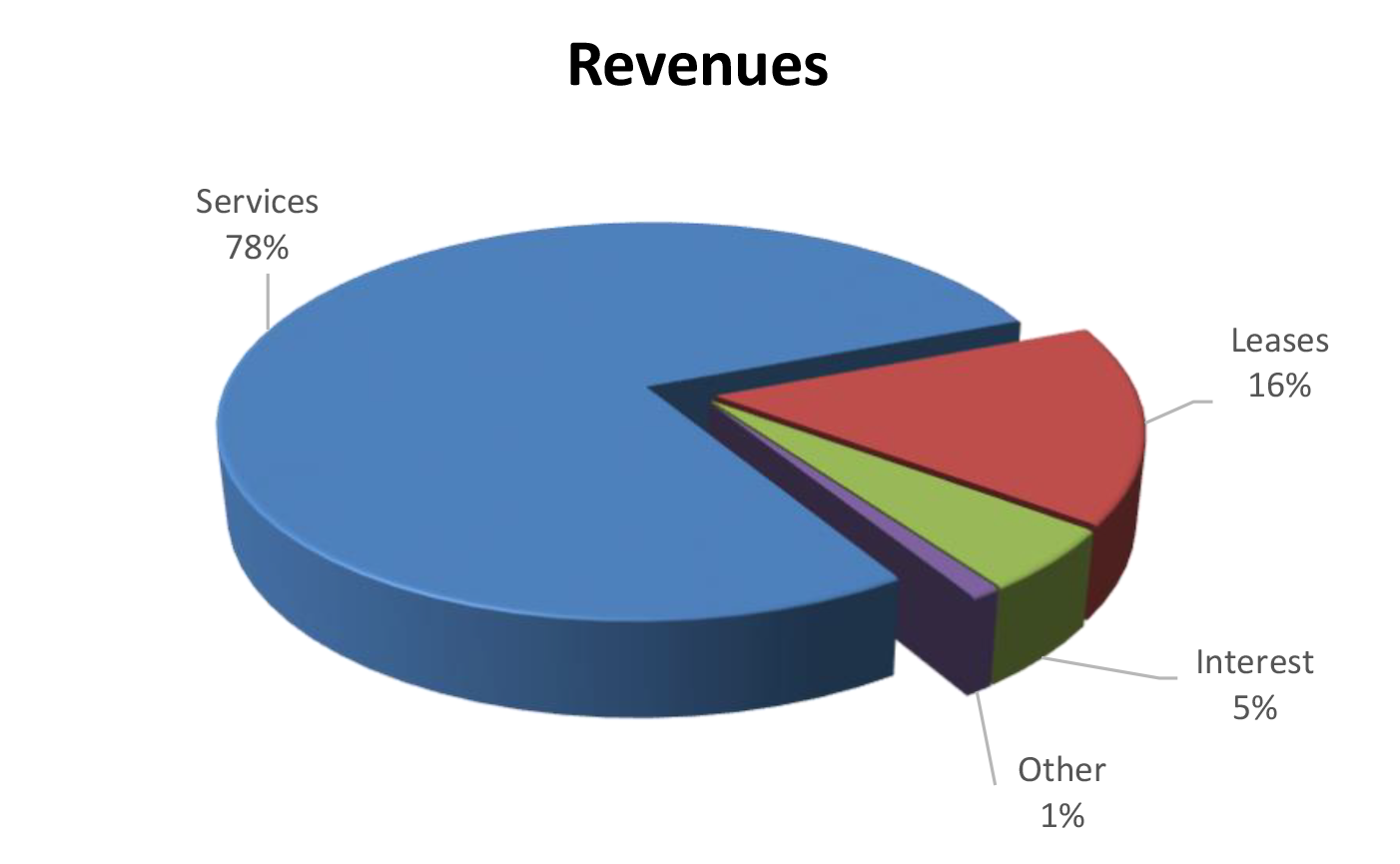

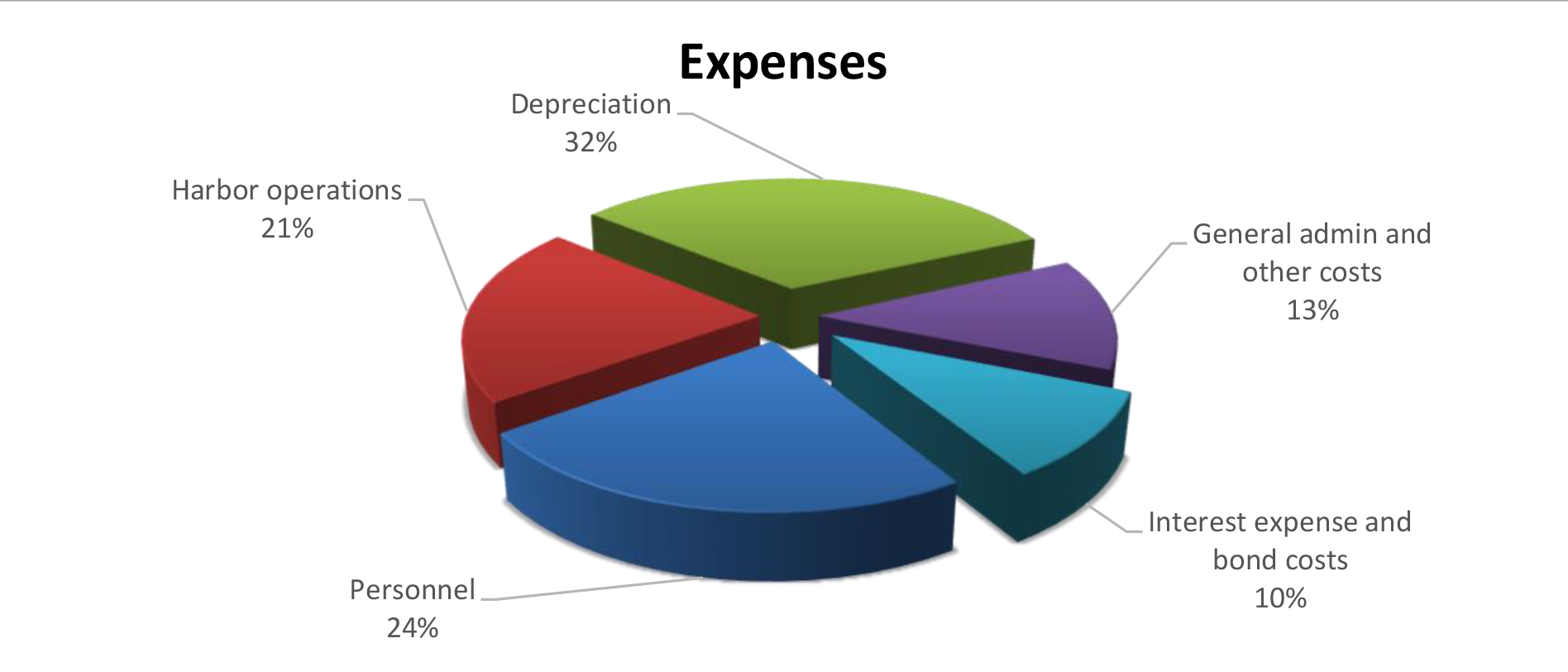

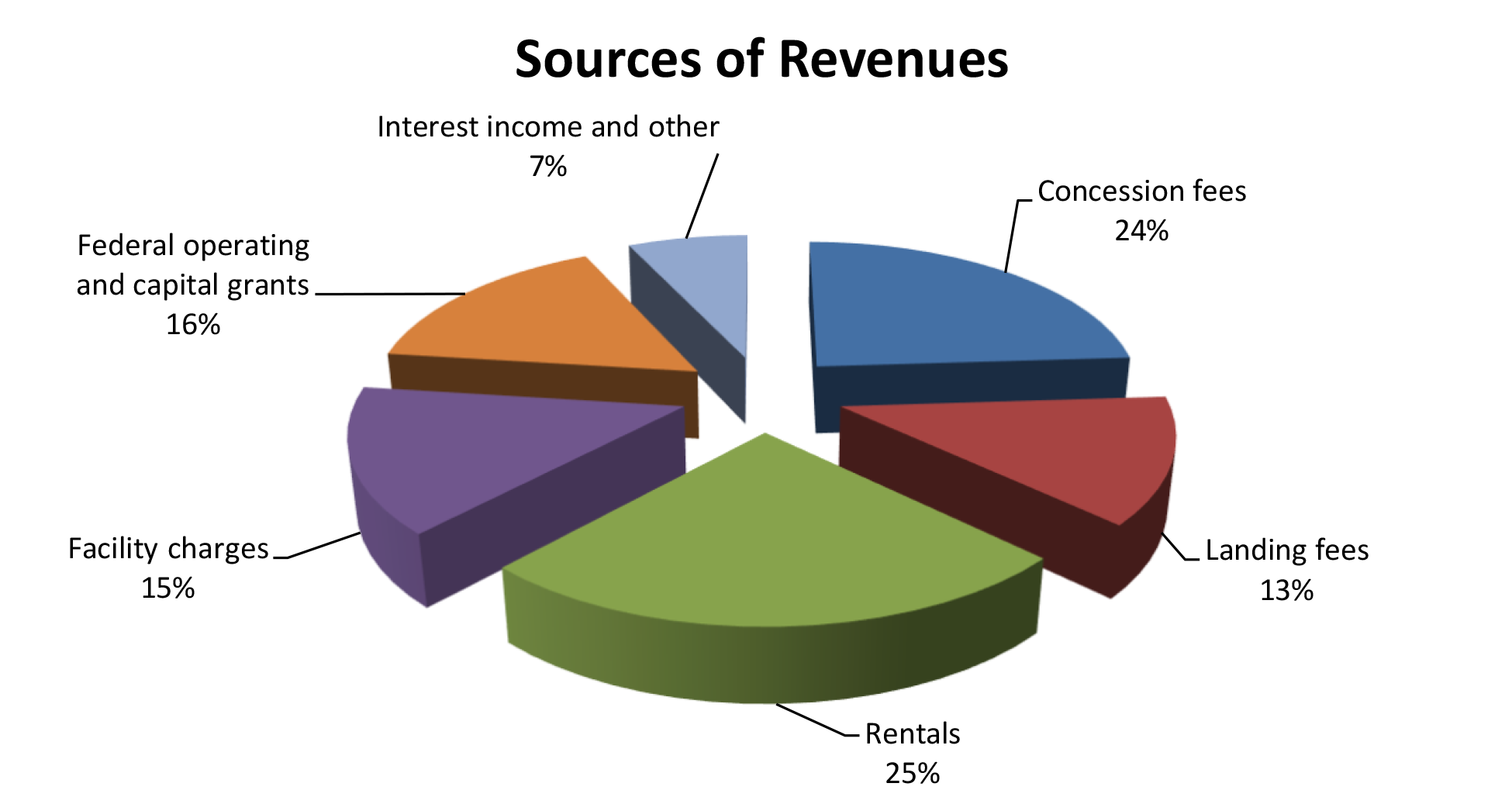

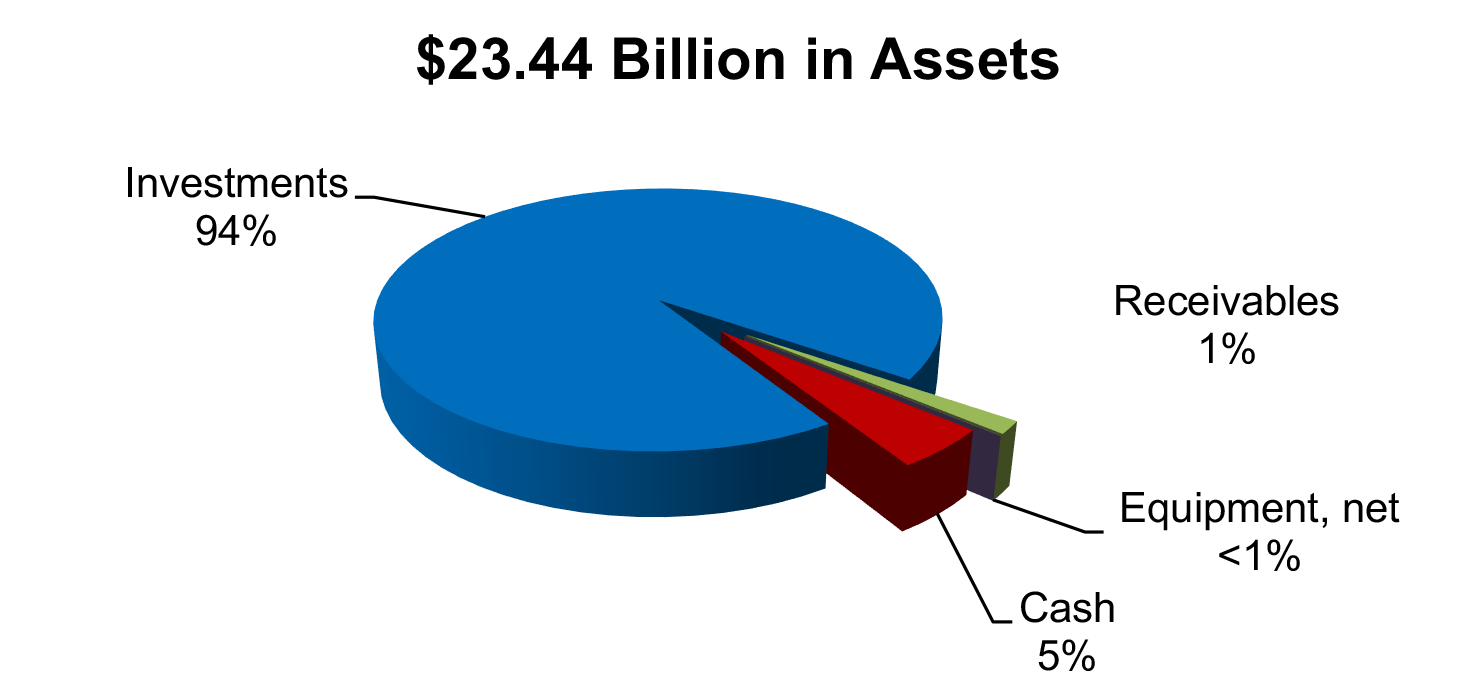

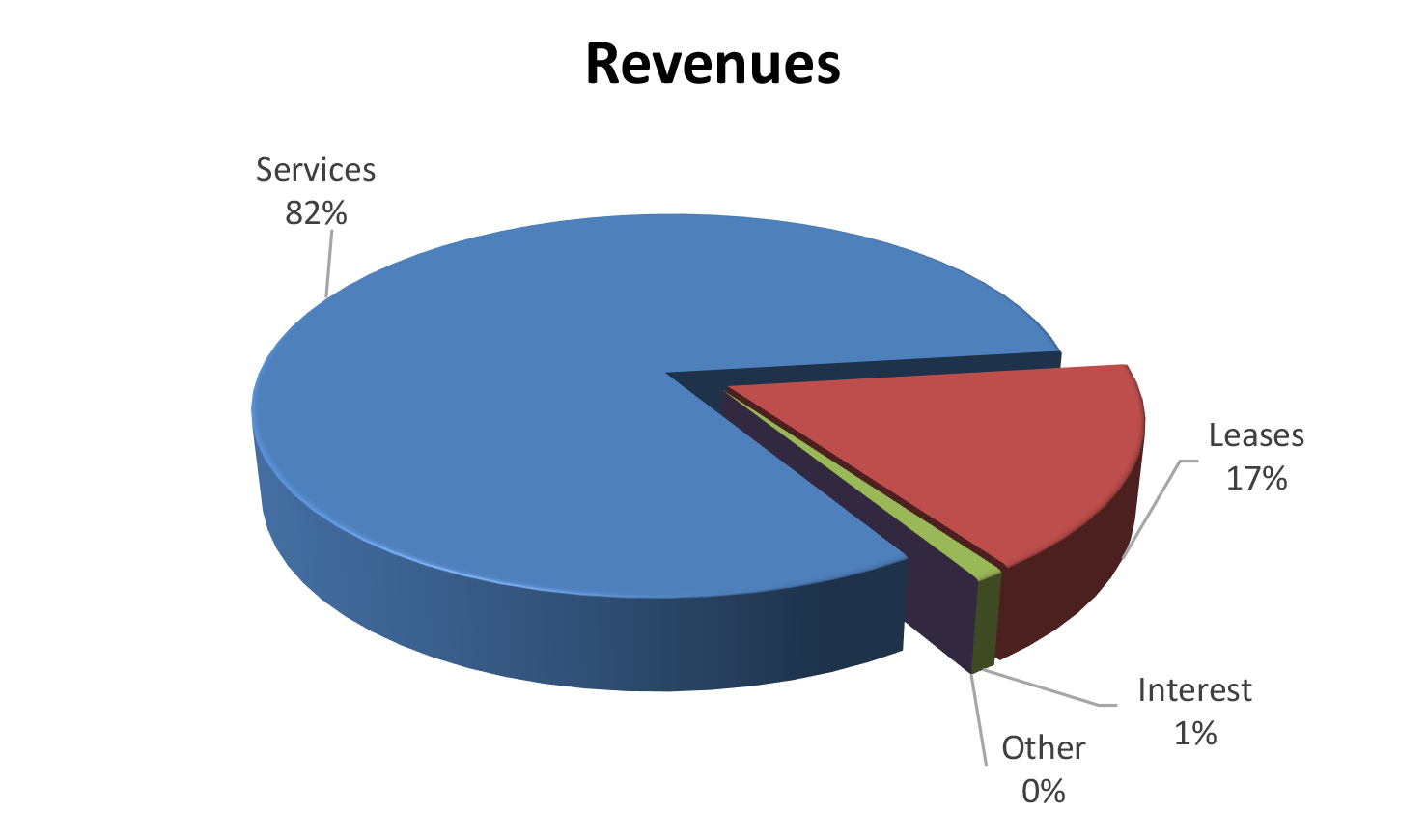

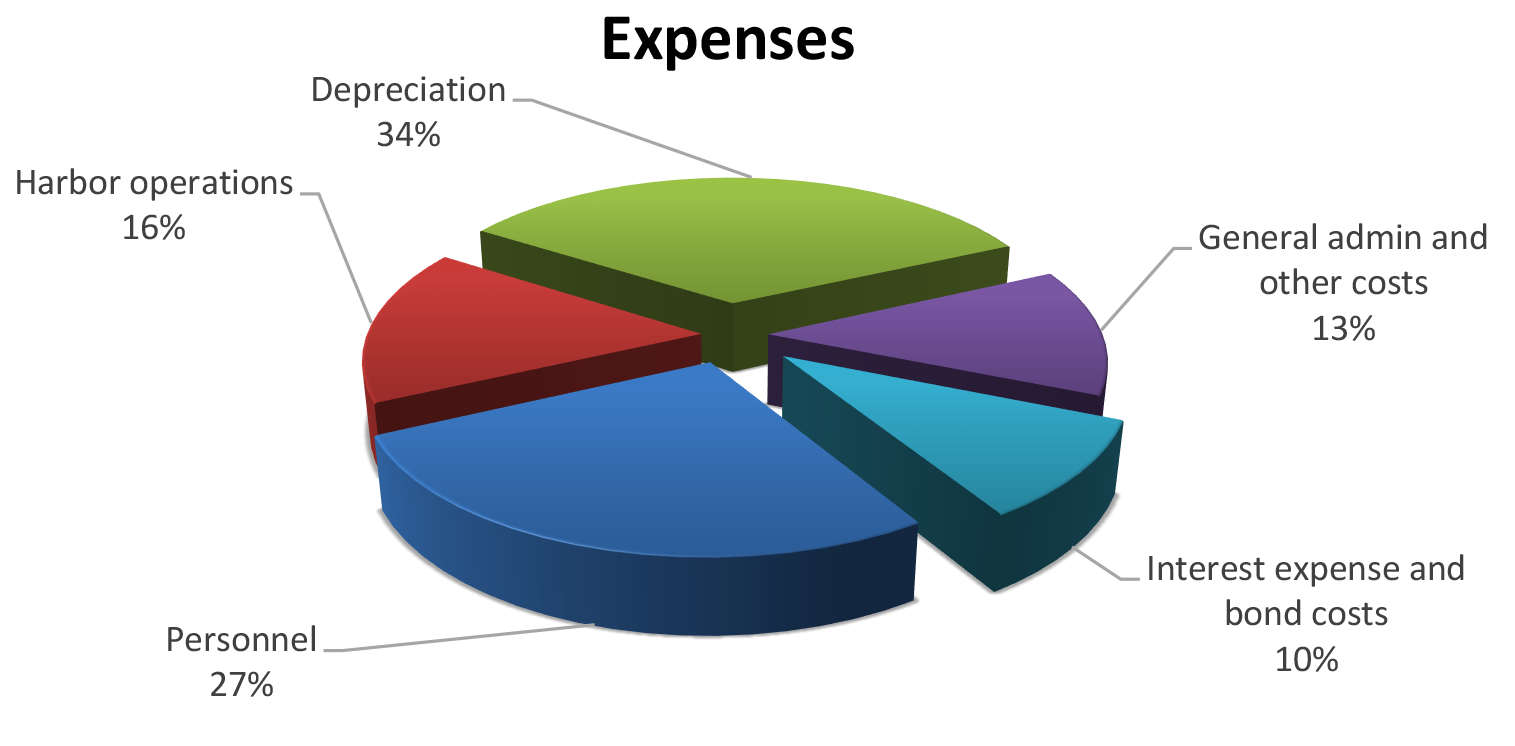

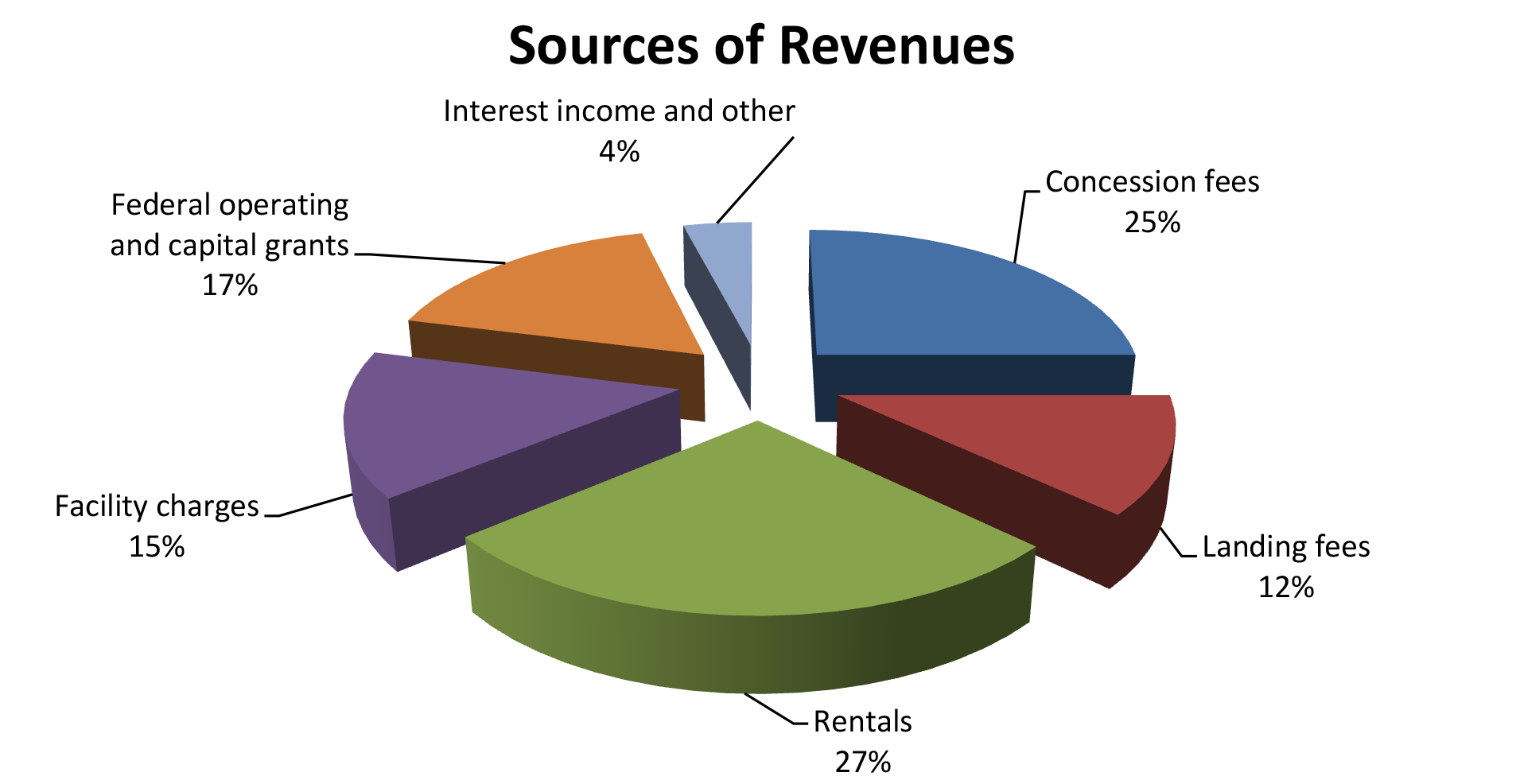

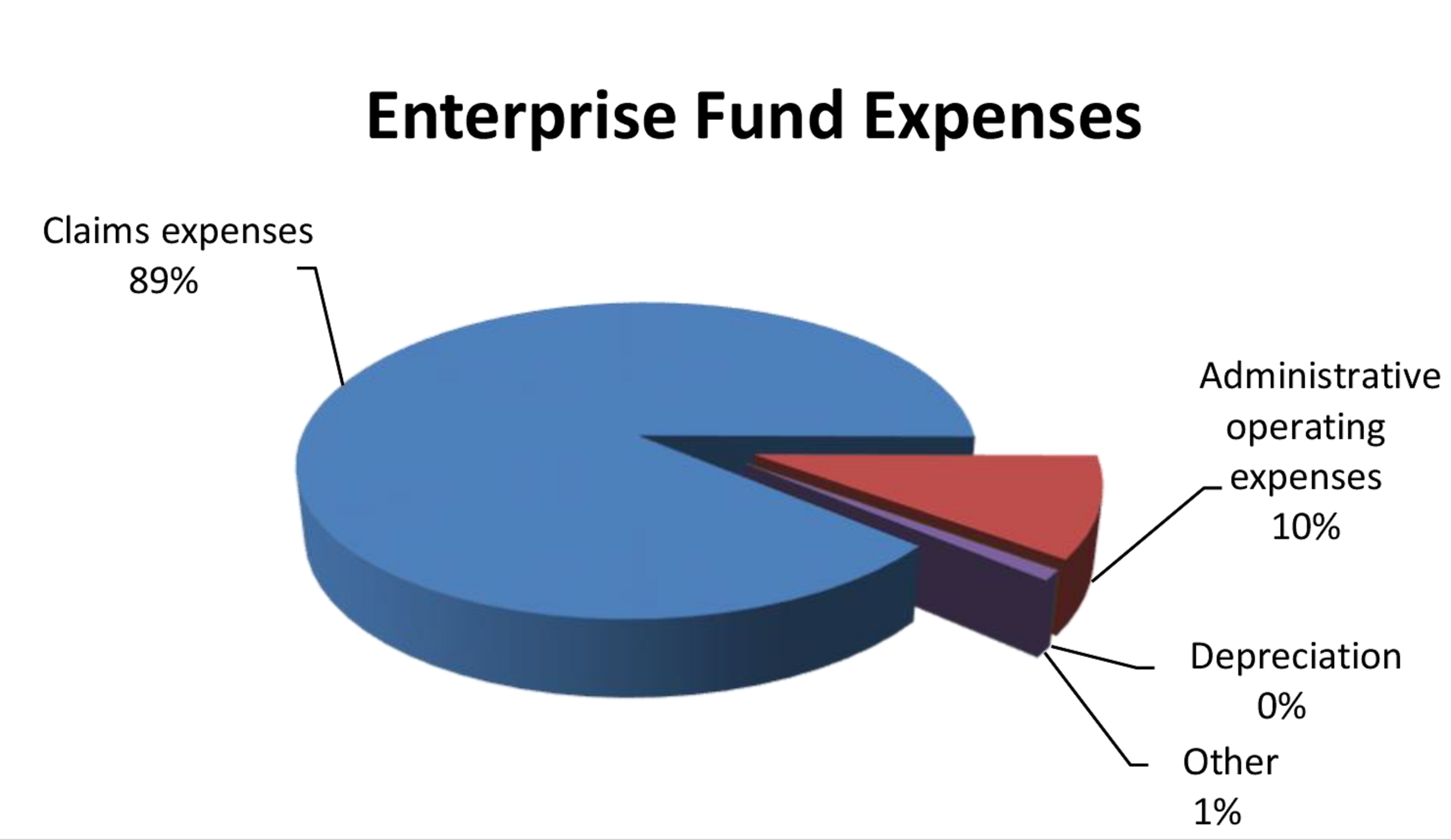

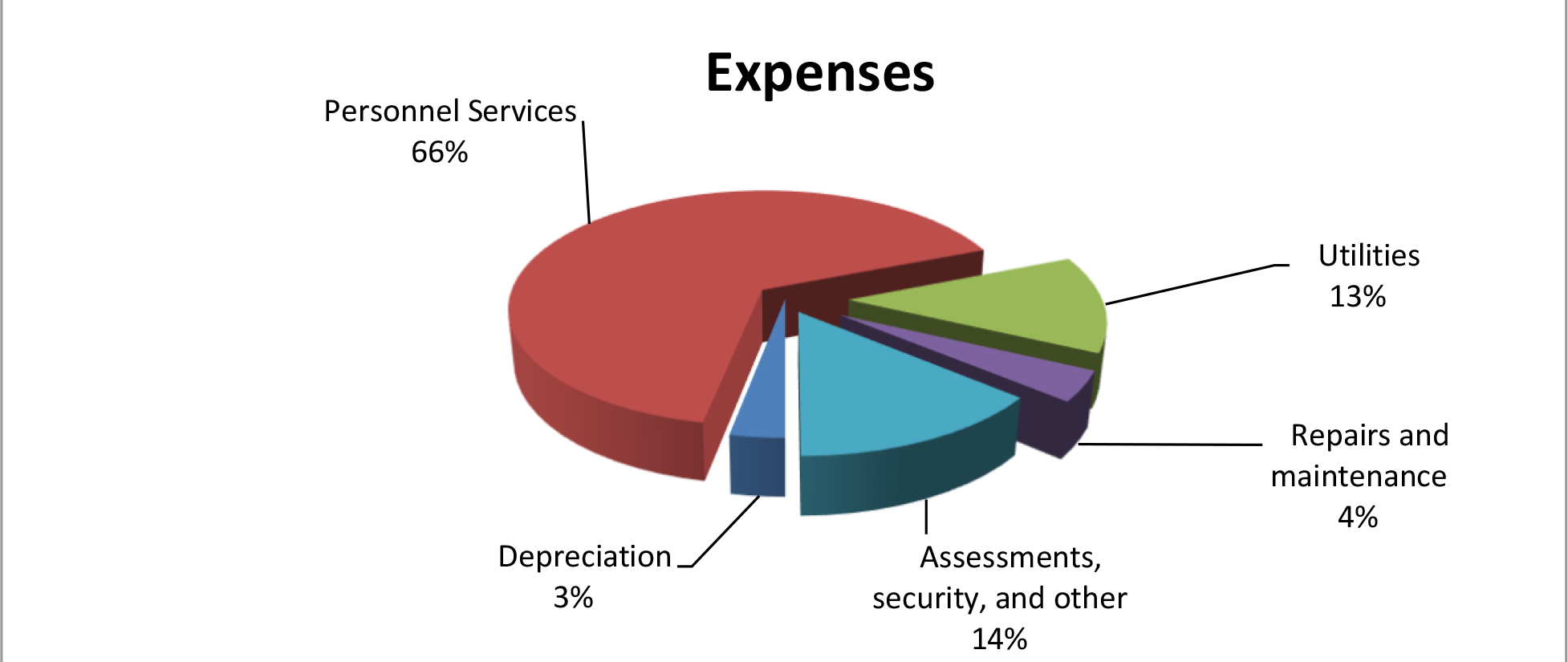

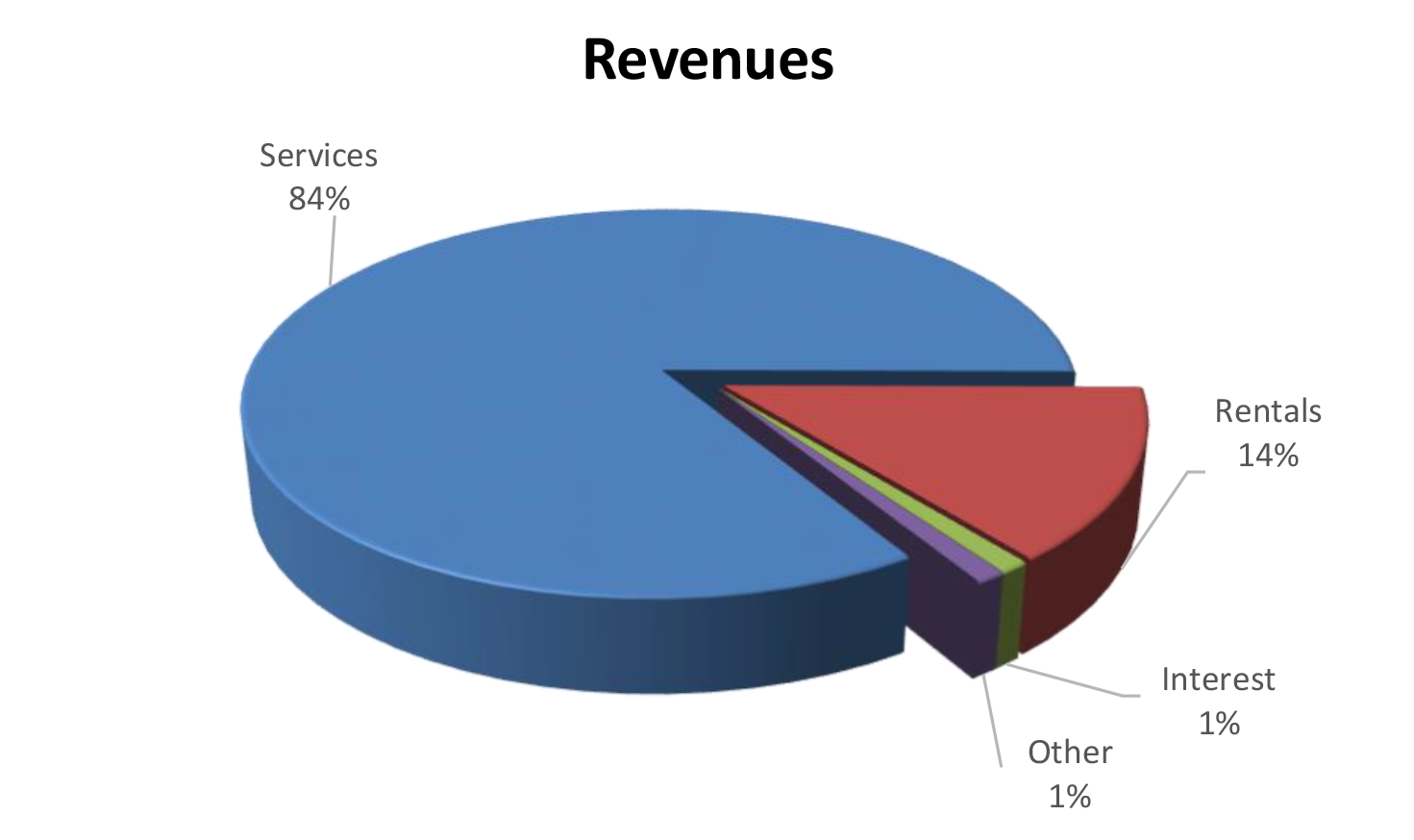

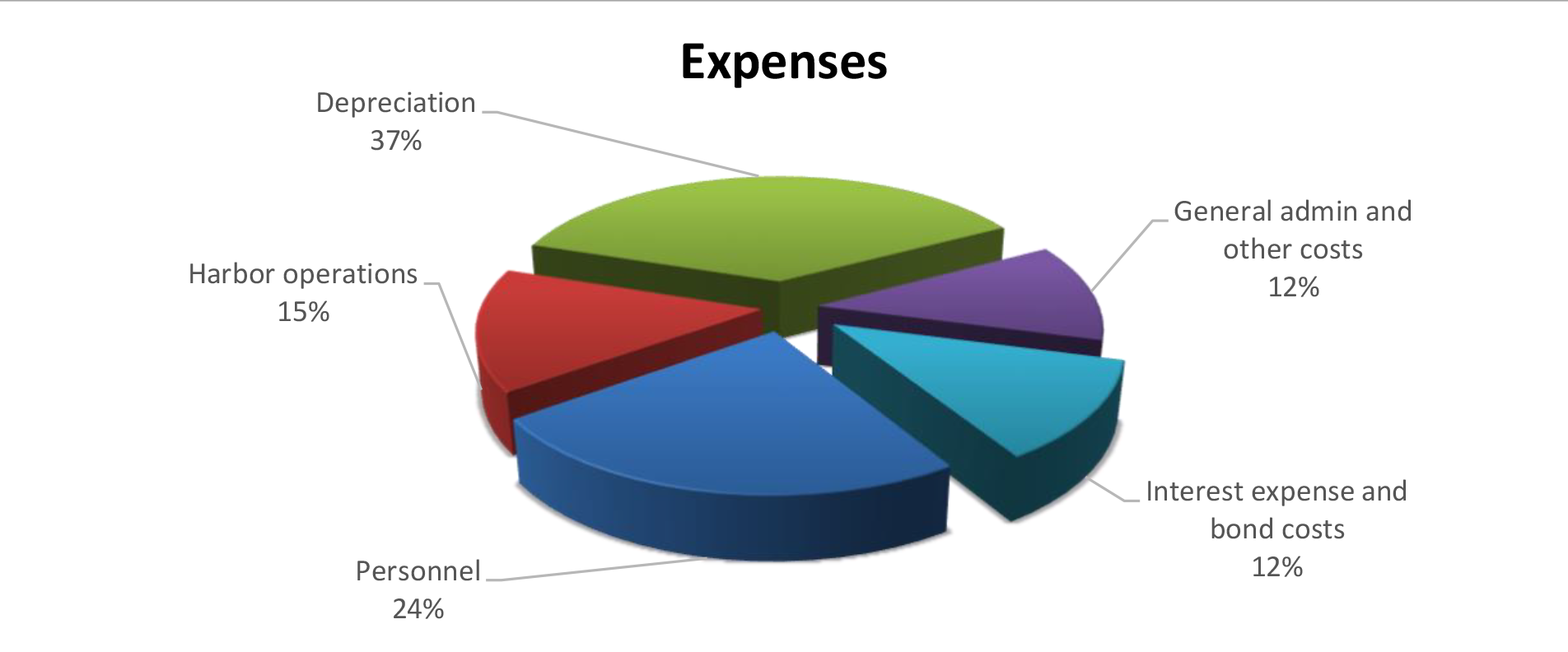

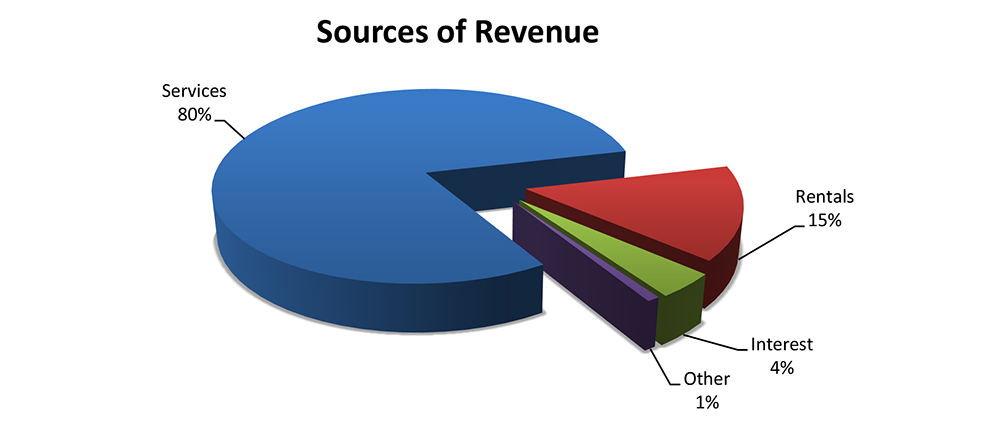

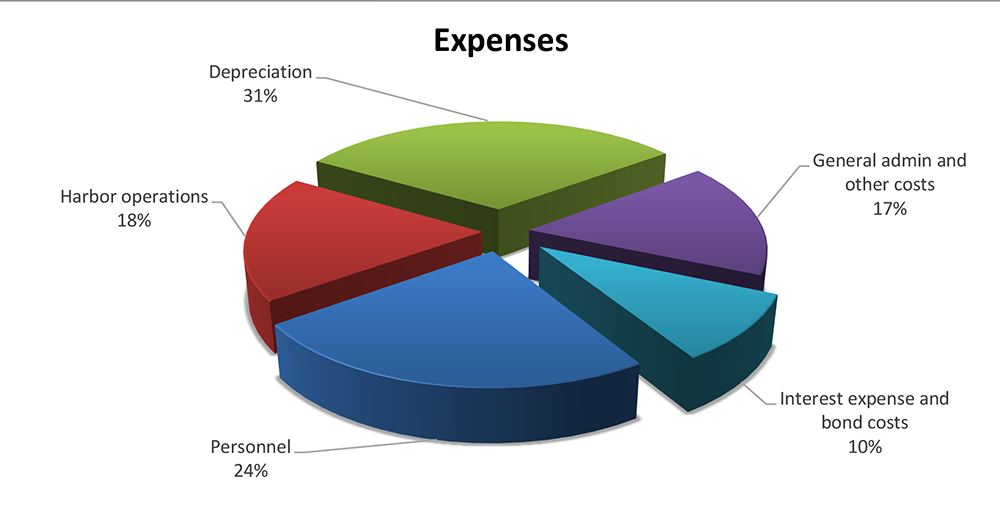

THE PRIMARY PURPOSE of the Department of Transportation, Harbors Division, Single Audit for the fiscal year ended June 30, 2024, was to comply with the Code of Federal Regulations, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, Title 2, Part 200 (Uniform Guidance), which established audit requirements for state and local governmental units that receive federal awards. The audit was conducted by Accuity LLP.

About the Report

SINGLE AUDITS provide assurance to the federal government that state agencies and programs receiving federal funds are expending those funds properly. This report includes the total federal expenditures and findings related to the DOT–Harbors’ Federal Financial Assistance Programs for the fiscal year ended June 30, 2024.

Auditors’ Opinion

DOT-HARBORS RECEIVED AN UNMODIFIED OPINION on its compliance with major federal programs in accordance with the Uniform Guidance.

Findings

THERE WERE NO REPORTED DEFICIENCIES in internal control over financial reporting that were considered to be material weaknesses and no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

There were no findings that were considered material weaknesses in internal control over compliance in accordance with the Uniform Guidance. However, the auditors identified two significant deficiencies in internal controls over compliance that were required to be reported under the Uniform Guidance. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. The significant deficiencies are described on pages 11-12 of the single audit report.

About the Division

The Department of Transportation, Harbors Division (DOT—Harbors) is responsible for Hawai‘i’s statewide system of commercial harbors consisting of ten harbors on six islands. Major activities include maintenance and operation, the construction of new harbor facilities, and the management of vessel traffic into, within, and out of Hawai‘i’s harbors. The Division is self-sustaining and receives no financial support from the State General Fund. Pursuant to Hawai‘i Revised Statutes, rates and charges imposed and collected pay for the costs of operations, maintenance, and repairs, as well as debt service on revenue bonds and other outstanding obligations. A capital improvements program is funded by the revenue and proceeds from harbors system revenue bonds.

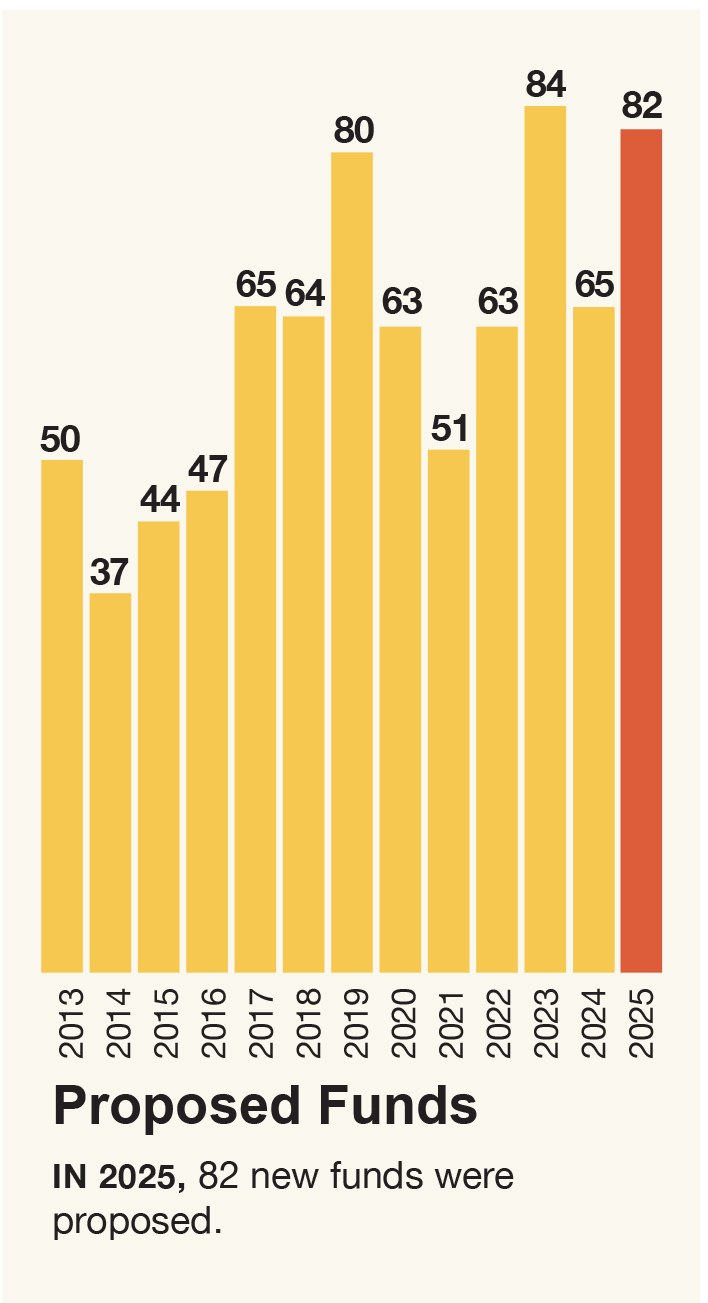

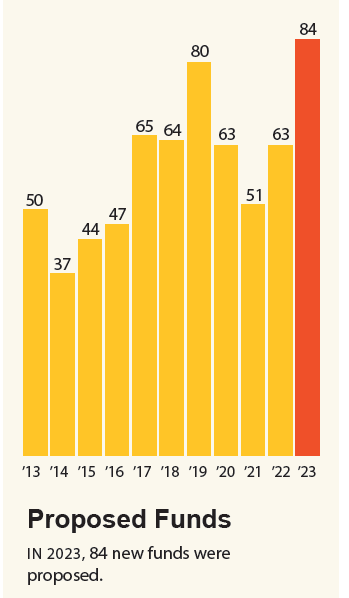

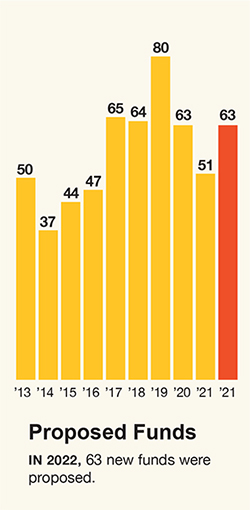

Eighty-two of the funds proposed in 2025 did not meet criteria.

We reviewed 127 House and Senate bills proposing 82 special and revolving funds during the 2025 legislative session of which none met criteria.

ONLY ABOUT HALF OF THE MONEY the State spends each year comes from its main financial account, the General Fund. The other half of expenditures are financed by special, revolving, federal, and trust funds. Between 2008 and 2012, the number of these non-general funds and the amount of money contained in them substantially increased. Much of that upward trend had been caused by an increase in special funds, which are funds set aside by law for a specified object or purpose.

In 2013, the Legislature amended Section 23-11, Hawai‘i Revised Statutes (HRS), after the Auditor recommended changes to stem a trend in the proliferation of special and revolving funds over the past 30 years. Such funds erode the Legislature’s ability to control the State budget through the general fund appropriation process. General funds, which made up about two-thirds of state operating budget outlays in the late 1980s, had dwindled to about half of outlays.

By 2011, special funds amounted to $2.48 billion, or 24.3 percent, of the State’s $10.2 billion operating budget. Also ballooning were revolving funds, which are used to pay for goods and services and are replenished through charges to users of the goods and services or transfers from other accounts or funds. By 2011, revolving funds made up $384.2 million, or 3.8 percent, of the State’s operating budget. Further hampering the Legislature’s control over the budget process was a 2008 court case. In Hawai‘i Insurers Council v. Linda Lingle, Governor of the State of Hawai‘i, the Hawai‘i Supreme Court determined that under only certain conditions could the Legislature “raid” special funds to balance the State budget. In 2013, in order to gain more control over the budget process, the Legislature built new safeguards into the criteria for establishing special and revolving funds.

This year, applying the criteria required by Section 23-11, HRS, we reviewed 127 Senate and House bills introduced during the 2025 legislative session that propose 82 new special and revolving funds. We determined that none of the proposed special and revolving funds satisfied the criteria established by the Legislature.

The Criteria

SECTION 23-11, HRS, requires the Auditor to analyze all bills proposing to establish new special or revolving funds according to the following criteria:

1. The need for the fund, as demonstrated by:

The purpose of the program to be supported by the fund;

The scope of the program, including financial information on fees to be charged, sources of projected revenue, and costs; and

An explanation of why the program cannot be implemented successfully under the general fund appropriation process; and